PRIVATE HEALTH COVER AU: 8 BEST WAYS TO SAVE ON YOUR AUSTRALIAN INSURANCE

did we know that over 14 million people in our nation—which is more than half of the total population—are currently protected by some form of private insurance? while we are immensely proud of our medicare system, many of us recognize that a personal policy delivers an additional layer of certainty, freedom of choice, and the financial defense that we truly value. as noted by “health.gov.au”, the intricate relationship between the public system and private sectors is built to ensure that every citizen has access to top-tier care while simultaneously easing the significant pressure on our public hospitals.

TIPS:

we recommend used official comparison tools like “privatehealth.gov.au” to see exactly how different funds stack up against each other.

we often find ourselves weighing up whether investing in private health cover au is a genuine necessity in a country that boasts such a dependable public safety net. the reality is that the australian medical landscape operates as a clever dual-track system where the public and private areas function in harmony to offer a complete blanket of coverage. by making the choice to hold a private policy, we aren’t just paying for medical services; we are securing our peace of mind, gaining quicker entry to elective treatments, and ensuring a level of personal comfort that the public sector cannot always promise during times of extreme demand.

in this extensive guide, we will dive deep into everything we need to understand about the world of private medical insurance down under. from decoding the different hospital tiers to navigating the maze of tax penalties like the medicare levy surcharge, we want to empower us with the clarity needed to make the smartest decisions for our family’s long-term health. we will simplify the tricky terminology, explain the firm regulations surrounding waiting periods, and help us calculate if the long-term rewards of private cover justify the monthly cost for our specific way of life and budget.

CAN I HAVE PRIVATE HEALTH INSURANCE IF I AM NOT AN AUSTRALIAN CITIZEN?

yes, but you might need “working visa health cover” or “overseas visitor health cover” (ovhc) instead of the standard policies linked to medicare.

KEY TAKEAWAYS

- australian private health insurance consists of two main categories: hospital cover for inpatient treatments and extras cover for services like dental and optical.

- the government uses incentives like the medicare levy surcharge (mls) and the lifetime health cover (lhc) loading to encourage younger citizens to join private funds.

- all hospital policies are now categorized into four standardized tiers—basic, bronze, silver, and gold—to help consumers compare plans more easily.

- standard waiting periods apply to almost all new policies, typically 12 months for pre-existing conditions and 2 months for most general treatments.

- portability rules allow us to switch between health funds without serving new waiting periods, provided we are moving to an equal or lower level of cover.

INTRODUCTION: UNDERSTANDING PRIVATE HEALTH COVER IN AUSTRALIA

when we discuss the concept of private health cover au, we are talking about a fundamental pillar of our healthcare system that grants us the ability to receive treatment as private patients in both public and private hospital settings. while medicare serves as a brilliant safety net for every citizen and permanent resident, private insurance is what truly hands us the power to customize our care. according to “privatehealth.gov.au”, our system relies on a “community rating” model, which guarantees that we all pay the same price for any given policy regardless of our age or medical background, ensuring that even those among us with complex needs are never pushed out of the market.

REMEMBER:

under the “community rating” rule, health funds cannot refuse to insure us or charge us more based on our pre-existing conditions or medical history.

the decision to go private is frequently driven by our desire for total control over our personal medical paths. as private patients, we have the legal right to select our own doctors or surgeons, which can be life-changing for those of us managing chronic health issues or for anyone who has formed a trust-based bond with a particular specialist. furthermore, the option to request a private room and benefit from enhanced hospital facilities can make our recovery journey much more relaxed and far less overwhelming during what are often the most stressful moments of our lives. we believe that these emotional benefits are every bit as significant as the clinical care we receive.

it is also vital for us to understand that our government actively encourages us to embrace private health insurance through a series of tactical financial measures. the “australian government rebate” works to lower our monthly premium costs, making private protection much more affordable than many of us initially expect. conversely, the “medicare levy surcharge” is applied to higher earners who skip private hospital cover, effectively turning insurance into a smart tax-saving strategy for many families across our country. gaining a solid grasp of these interactions is the key to optimizing our finances while we safeguard our collective health future.

IS DENTAL COVER ALWAYS INCLUDED IN PRIVATE HEALTH INSURANCE?

no, dental is typically part of “extras” cover, not hospital cover. you must choose a policy that specifically lists dental as an included service.

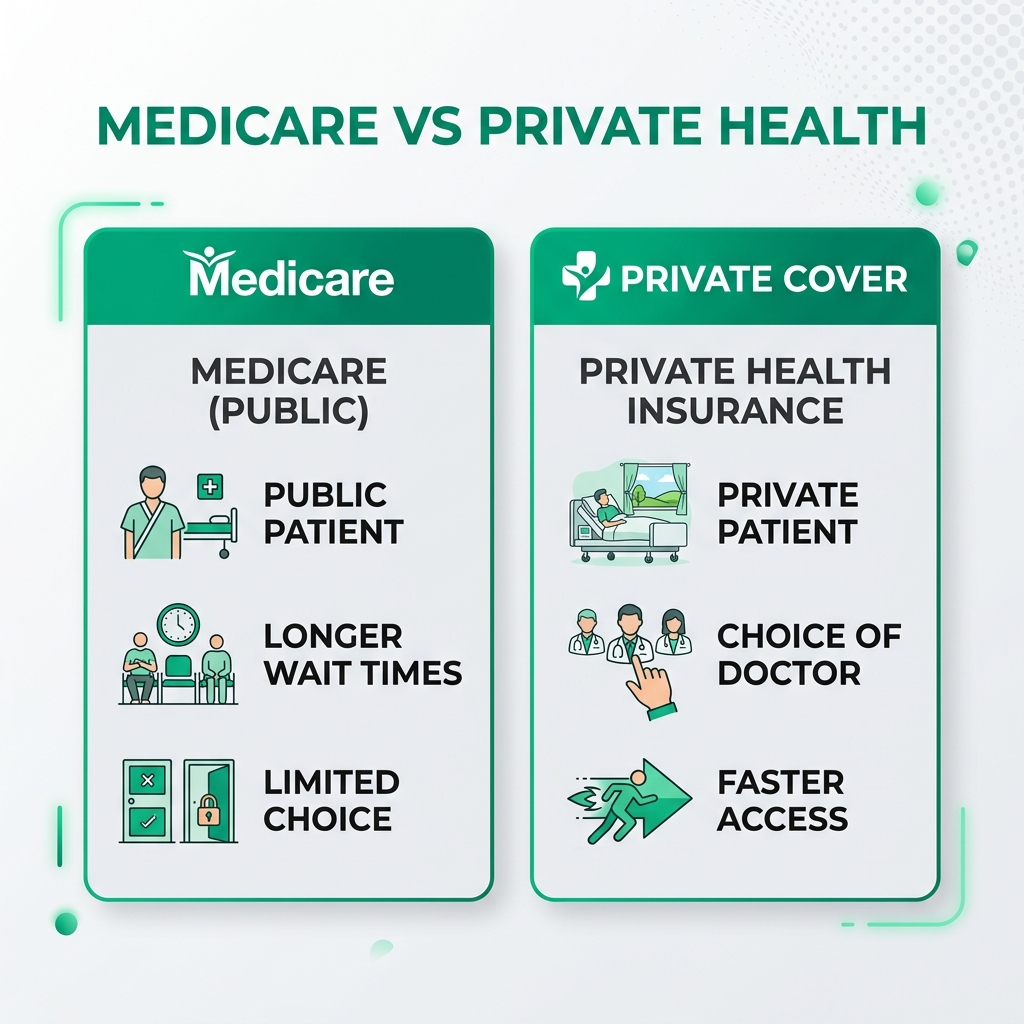

MEDICARE VS. PRIVATE HEALTH INSURANCE: WHAT’S THE DIFFERENCE?

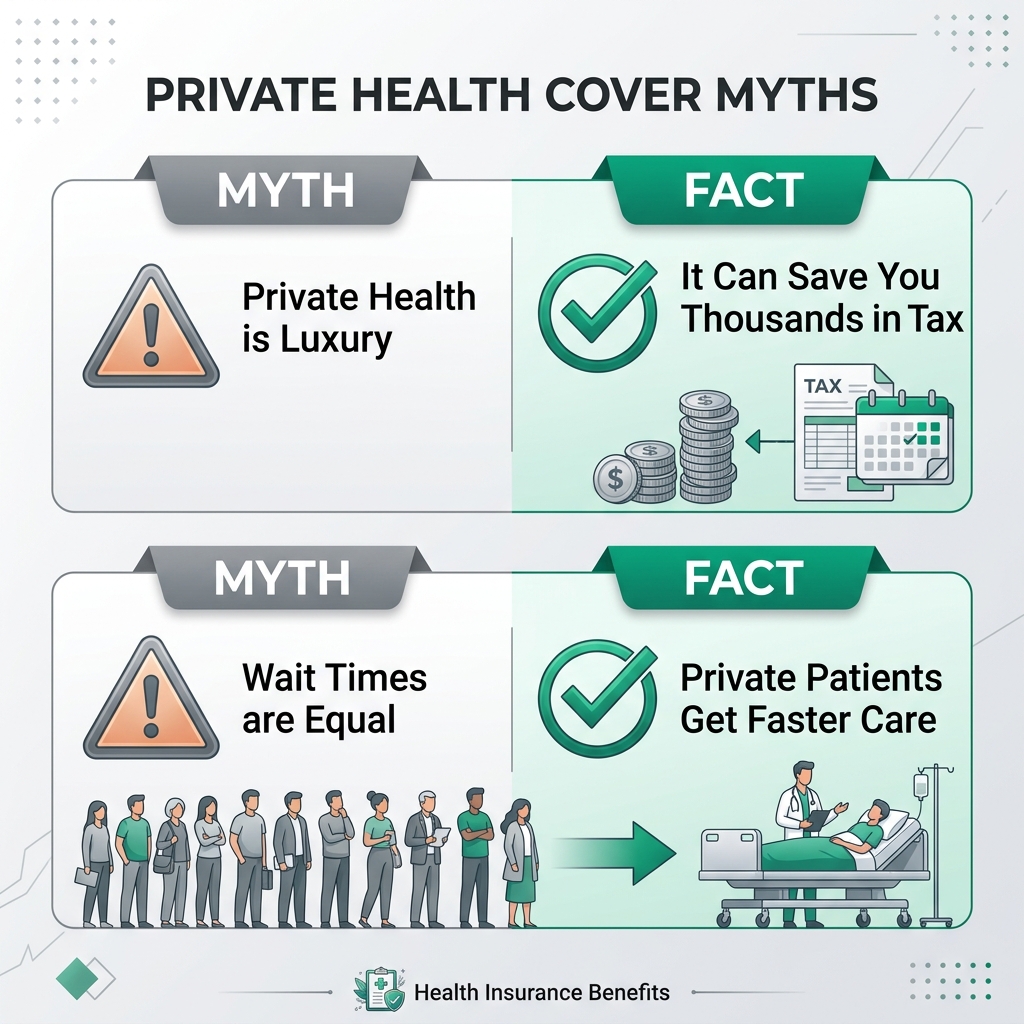

to truly comprehend why so many of us choose to invest in private health cover au, we must first examine exactly what medicare provides and where its limits lie. medicare is our universal plan that takes care of our hospital bills when we are treated as public patients in a public facility, and it also helps pay for our visits to the doctor and several specialist diagnostic services. nevertheless, our public system is often pushed to its capacity, which leads to the creation of lengthy waiting lists for elective procedures like joint replacements or vision-saving surgeries. as noted by “health.gov.au”, these waits can sometimes last for years, which is incredibly difficult for those of us living with pain or limited freedom.

You Might Also Like

private health insurance functions as a fast-track pass that lets us leap over these long public queues by giving us access to specialized private hospitals. when we are admitted as private patients, our chosen insurer helps us manage the costs of our room, the theatre charges, and a significant portion of the fees charged by our medical team. this freedom typically means we can pick a surgery date that works for our schedule, rather than waiting for an opening in the public queue. while medicare still pays for 75% of the official schedule fee for our treatment in a private setting, our insurance bridge the remaining 25% plus any “gap” costs if our doctor charges above the medicare rate.

one more vital distinction is found in our daily out-of-hospital care. medicare generally does not provide cover for the “extras” or ancillary services that many of us rely on for our regular well-being. for example, if we need a new set of prescription glasses, a routine dental cleaning, or a session with a physiotherapist to fix a back injury, medicare usually offers no help at all. this is where “extras cover” becomes an essential part of our lives, as it gives us money back for those critical healthcare services that keep us healthy and prevent small problems from becoming emergencies. by pairing medicare with a private policy, we ensure we are protected against both major health crises and the everyday costs of staying fit in the private health cover au landscape.

NOTE:

even with private insurance, you should still carry your medicare card as it remains the foundation of your healthcare access in australia.

THE TWO MAIN TYPES OF COVER: HOSPITAL VS. EXTRAS

starting our journey with private health cover au usually means picking between hospital cover, extras cover, or perhaps a combined plan. hospital cover is specifically engineered to handle the massive costs that come with a hospital stay as a private patient. this includes everything from the surgical fees and intensive care stay to the costs of the anaesthetist and the room itself. according to “privatehealth.gov.au”, this type of insurance is divided into very clear clinical categories, such as heart health or joint surgery, so we can see exactly what our specific policy protects without any confusion or fine-print surprises.

WHAT IS A “GAP” PAYMENT?

a “gap” is the difference between what your doctor charges and what medicare plus your private insurer will pay. always ask for “informed financial consent” before treatment.

extras cover, which we often call ancillary or general treatment cover, is focused on the medical services that take place outside of a hospital ward. these are the vital treatments that help us stay mobile and active in our everyday lives, including the dentist, the optometrist, podiatry, and even things like remedial massage. for many of us, this is the most frequently used part of our insurance, as it provides instant value through regular check-ups and preventative services. most of our health funds offer various levels of extras, where higher-tier plans offer us bigger annual limits and a higher percentage of cash back on every single claim we make.

for the majority of us, a “combined cover” policy is the most logical choice as it bundles both hospital and extras into one convenient package. this strategy often delivers the best overall value and ensures that we have no weak spots in our total healthcare plan. however, it is entirely possible for us to mix and match—for instance, keeping our hospital cover with one company and our extras with another—to maximize our benefits and tailor our defense to our specific needs. we always suggest looking at these two parts separately to make sure nuestro private health cover au hospital tier matches our medical risks while our extras limits fit our planned usage for the upcoming year.

BREAKING DOWN THE HOSPITAL PRODUCT TIERS (GOLD, SILVER, BRONZE, BASIC)

to make it much simpler for us to compare different private health cover au options, the australian government rolled out a compulsory tier system in 2019. now, every hospital policy we can buy must be labeled as either basic, bronze, silver, or gold. this move toward standardization was a massive victory for us as consumers, as it wiped away confusing brand names and replaced them with a system where a “bronze” plan from any fund must cover the exact same set of clinical categories. as explained by “health.gov.au”, this level of transparency finally allows us to make an honest “apples-to-apples” comparison and find the best deals on the market.

TIPS:

look for “plus” policies (e.g., bronze plus) which might offer silver-level benefits like heart cover while keeping the lower tier’s price tag.

these tiers are set up like a ladder, with each new step adding more essential services. “basic” cover is the starting point and is often picked by those of us who just want to avoid the medicare levy surcharge or need limited help with specific services like psychiatric care. “bronze” cover takes it a step further by adding 18 different clinical areas, including bone, joint, and muscle care. “silver” is the popular mid-range choice that covers everything in bronze plus 8 more categories such as heart surgery and dental surgery. it offers a solid shield for many of us who are reaching our middle years and want to be prepared for the common health issues that come with age.

standing at the very peak is “gold” cover, which is our most extensive and high-protection option. gold policies are required by law to cover all 38 clinical categories defined by the government, including high-cost services like pregnancy and birth, cataracts, and even joint replacements. if we are thinking about starting a family or are approaching an age where we might need a hip or knee replacement, gold cover is usually the only way to guarantee we are protected in a private setting. we always tell people to keep an eye out for “plus” policies, where an insurer might add a few higher-tier services into a lower-tier plan to give us better value without the high gold price.

CAN I CLAIM FOR GLASSES EVERY YEAR?

most extras policies have an annual optical limit that resets every calendar or financial year. check your fund’s specific reset date to maximize your benefits.

You Might Also Like

| TIER | KEY CLINICAL CATEGORIES INCLUDED | WHO IS IT FOR? |

|---|---|---|

| GOLD | PREGNANCY, CATARACTS, JOINT REPLACEMENTS, DIALYSIS | FAMILIES, SENIORS, HIGH-RISK INDIVIDUALS |

| SILVER | HEART, LUNG, BLOOD, DENTAL SURGERY, BACK/SPINE | ESTABLISHED ADULTS, ACTIVE INDIVIDUALS |

| BRONZE | BONE/JOINT, BRAIN, DIGESTIVE SYSTEM, ENT SURGERY | YOUNG ADULTS WITH LOWER HEALTH RISKS |

| BASIC | REHABILITATION, PSYCHIATRIC, PALLIATIVE CARE | THOSE SEEKING TAX BENEFITS ONLY |

WHAT IS EXTRAS COVER AND WHAT DOES IT INCLUDE?

when we explore the world of extras cover inside the private health cover au system, we discover a huge range of services that help us maintain our daily quality of life. while hospital cover is all about the big emergencies and surgeries, extras is about the steady, regular care that keeps our bodies running. the most popular services we use are “general dental,” which covers our check-ups and simple fillings, and “major dental,” which takes care of expensive things like crowns and wisdom teeth. for many of us, the cost of just one major dental surgery can be more than our whole annual premium, which makes these policies a very smart investment for our wallets.

WARNING:

never wait until you have an emergency dental problem to join a fund, as major dental surgery usually requires a 12-month waiting period.

optical cover is another bedrock of most extras plans, giving us annual rebates for things like our prescription glasses, contact lenses, and even prescription sunglasses. since millions of us in australia need help with our vision, this benefit is practically like cash in our pockets. in addition to the major areas like dental and optical, we often find that extras includes things like the physiotherapist, chiropractic care, and psychology. as “privatehealth.gov.au” explains, these services are the key to preventative health, helping us manage our small injuries or mental health struggles before they turn into bigger problems that might land us in a hospital bed.

it is also well worth looking at the more specialized extras that many of our modern insurers are now offering. some of the top-tier extras plans include money for hearing aids, speech therapy, and even health management programs like gym memberships or weight loss coaching if a doctor prescribes them. however, we must look very closely at the “annual limits”—the maximum amount we can claim each year—and see if those limits are for each person or shared across our whole family group. some funds also use “loyalty bonuses” to increase our limits the longer we stay with them, rewarding us for our loyalty and helping us get even more from our private health cover au over time.

UNDERSTANDING WAITING PERIODS: WHAT YOU NEED TO KNOW

one of the most important concepts of private health cover au that we absolutely must understand is the idea of “waiting periods.” a waiting period is simply the amount of time we have to hold our insurance policy before we are allowed to make a claim for a certain service. these timeframes are strictly controlled by our government to stop people from only joining a fund when they know they need an expensive surgery and then leaving the fund immediately after. according to “health.gov.au”, these rules are necessary to keep our insurance premiums affordable for everyone by making sure we all contribute to the collective pool for a while before we take out large benefits.

DO I NEED TO STAY WITH MY FUND FOR 10 YEARS TO REMOVE LHC LOADING?

yes, once applied, the lhc loading is only removed after you have held hospital cover for 10 continuous years.

You Might Also Like

the standard max wait times that our health funds can apply are actually quite similar across the whole industry. for most general hospital care and rehab services, the wait is usually just 2 months. however, for more major medical categories, the wait is often much longer. for instance, “pregnancy and birth” always comes with a 12-month waiting period, which means we have to plan ahead if we want to use private maternity care for our future children. similarly, any condition that we already had in the 6 months before we joined a fund is labeled as a “pre-existing condition” and always has a 12-month wait before we can claim hospital benefits for it.

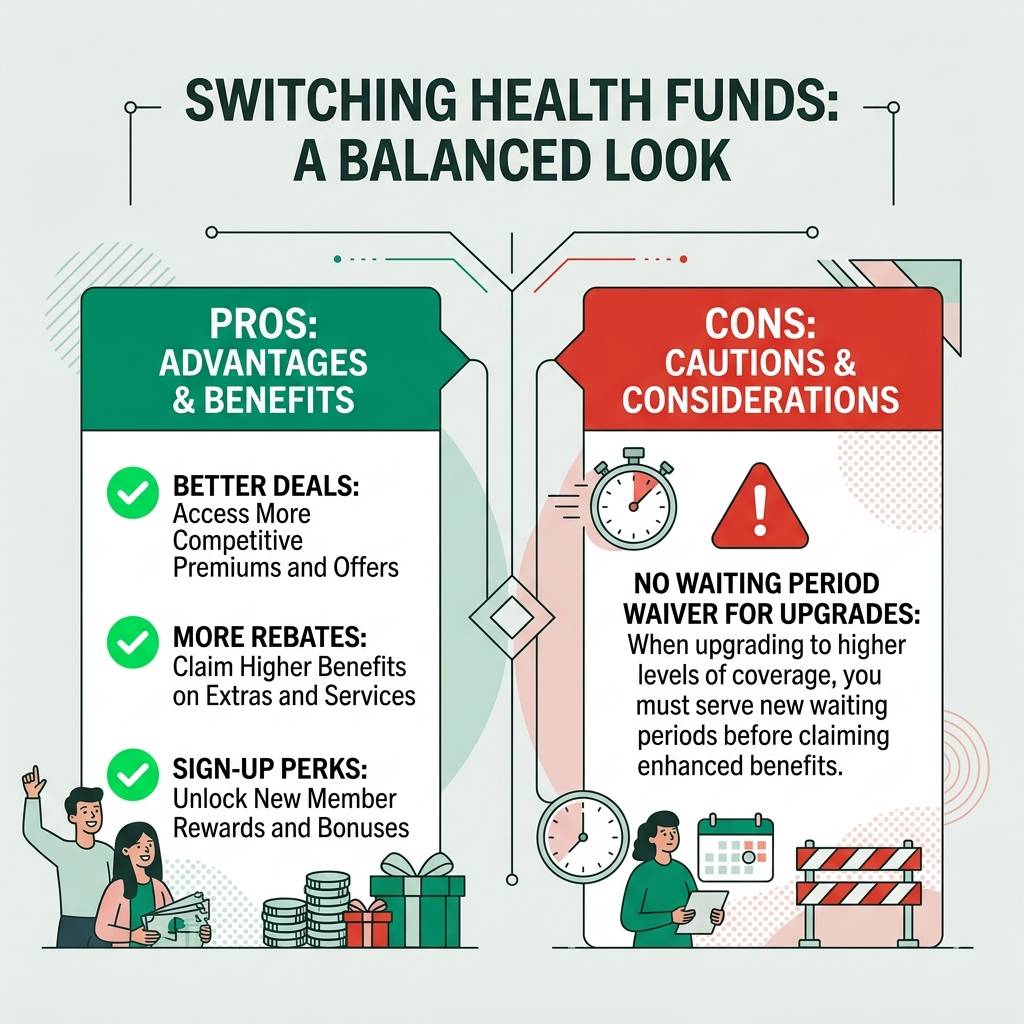

when it comes to extras cover, these waiting periods can vary quite a bit between insurers because the government doesn’t control them as strictly. we often see 2 to 6-month waits for simple things like dental or physio, while the big stuff like major dental or orthodontics almost always makes us wait for a full year. the good news is that if we are moving from a similar policy at another fund, we do not have to serve these waits again. this “portability” rule is one of our fundamental rights in the australian system, allowing us to shop around for better prices without losing our chance to get care when we need it most in the private health cover au market.

“waiting periods are an essential part of the private health insurance system, designed to protect all members by ensuring that everyone contributes fairly to the fund before claiming significant benefits.” — PRIVATEHEALTH.GOV.AU

AVOIDING THE MEDICARE LEVY SURCHARGE (MLS)

our financial planning and our choice of private health cover au are very closely linked, especially when it comes to the “medicare levy surcharge” (mls). most of us are already paying a 2% “medicare levy” in our tax to help fund the public system we all use. however, if we earn more than a certain amount and we don’t have the right level of private hospital insurance for ourselves and our dependents, the government will charge us an extra fee. per “health.gov.au”, the mls is specifically designed to nudge those of us with higher incomes into the private system, which then frees up beds and resources in our public hospitals for those who truly need them.

REMEMBER:

to avoid the medicare levy surcharge, you must have hospital cover. extras-only cover does not prevent this tax penalty from being applied.

the income levels for this surcharge are set in tiers based on whether we are single or have a family. for a single person earning more than $97,000, or a family group making over $194,000, the surcharge starts at 1% of our taxable income. as our earnings go up, the surcharge rate climbs too, hitting a max of 1.5% for high earners. for many of us in those income bands, the cost of the extra tax can actually be more expensive than the cost of a basic private hospital policy. in those cases, taking out private health cover au is a smart financial move that takes our tax dollars and puts them into a service that directly takes care of us.

we must always remember that to escape the mls, we have to hold a private hospital policy specifically. having only an extras policy will not stop this tax penalty from being applied to us. furthermore, our policy has to have an excess of no more than $750 for singles or $1,500 for families to count toward the private health cover au requirements. once we have the right plan in place, we just tell our accountant or put the details on our tax return to stop the surcharge. we’ve found that this is one of the strongest reasons why young aussie professionals join the private market, as they can effectively get “free” insurance by saving on the tax they would have otherwise lost.

THE IMPACT OF LIFETIME HEALTH COVER (LHC) LOADING

another policy that we really need to keep on our radar is the “lifetime health cover” (lhc) loading. this is an initiative from the government that penalizes us if we join the private hospital market later in our lives. the rule is very simple: if we haven’t taken out private hospital cover by the 1st of july after our 31st birthday, we will pay a 2% loading on our premium for every single year we were over 30 when we eventually join. for example, if we wait until we are 40 to get a policy, we could be paying 20% extra on our premiums for the next decade. as “privatehealth.gov.au” mentions, the max loading is a huge 70%, which can make insurance very expensive if we wait too long.

TIPS:

if you are moving to australia from overseas and are over 31, you have 12 months from being eligible for medicare to join a fund without an lhc loading.

You Might Also Like

this lhc loading was created to encourage us to join the system while we are young and healthy, which helps create a stable and balanced pool of money for everyone. if we are already paying this loading, it isn’t something that stays forever—we only have to pay it for 10 straight years of being a member, and after that, the loading is removed and we go back to the standard price. for people who have just moved to australia and are over 31, there are special rules that let them join without any loading if they get a policy within a year of getting medicare. we always highlight how important it is to beat that 31st birthday deadline to lock in the lowest rates for our future in the private health cover au system.

managing our “lhc status” is a big part of our long-term plan for healthy living. if we ever decide to take a break from our cover—maybe while we are traveling outside the country—we are allowed to have some “permitted days without cover” that don’t trigger the penalty. currently, we are allowed to be without cover for up to 1,094 days (nearly three years) across our entire lifetime without losing our loading status. this bit of flexibility is great, but we have to track those days very carefully so we don’t get a bad financial shock when we decide to restart our private health cover au. staying informed about these tiny rules is the best way to protect both our health and our bank balance.

THE AUSTRALIAN GOVERNMENT REBATE: LOWERING YOUR PREMIUMS

to help make the cost of private health cover au much more manageable for everyone, the australian government provides a “private health insurance rebate.” this is basically a contribution from the government toward the overall price of our daily premiums. the amount of money we get back depends on our income, so the more we make, the less support we receive. according to “health.gov.au”, this rebate is open to most of us whose total taxable income is below a certain level, and the percentages also change as we get older, with those of us over 65 and 70 getting slightly more help to keep our cover during our retirement years.

NOTE:

most people choose to receive their rebate as a premium reduction, which makes the regular payments significantly cheaper upfront.

we have two different ways to get our hands on this rebate. the most popular choice is to have it applied directly to our bill by our insurance company, which immediately cuts down the amount we have to pay every month. on the other hand, we can choose to pay the full price ourselves and then claim the money back as a one-off payment when we do our taxes with the australian taxation office (ato). for many of us, getting that instant discount is the much easier way to go, as it helps our weekly cash flow and makes it feel a lot easier to stay protected without breaking our budget for private health cover au.

it is very important for us to check our income brackets every year because if we guess wrong and claim more rebate than we should have, the ato will ask us to give the difference back when we do our tax. conversely, if we earn less than we thought, we will get the extra rebate money back as a tax refund. while the government adjusts the rebate amount a bit every year to keep up with the rising costs of medical care, it remains a pillar of our system that makes private health cover au a realistic choice for millions of aussie families. staying ahead of these tax brackets ensures we are always getting the right level of help from the government every year.

SWITCHING HEALTH FUNDS: RULES AND BENEFITS

REMEMBER:

when switching funds, your old fund must provide a “transfer certificate” to your new fund to prove you have already served your waiting periods.

You Might Also Like

we should never feel like we are stuck with the same health fund forever, as the rules around “portability” make the process of switching very easy and often quite profitable. in our country, health funds are legally obligated to respect any waiting periods that we have already finished with a previous fund, provided we are moving to a plan that has the same or lower level of protection. this means if we have been with a company like “bupa.com.au” for several years and want to move to “medibank.com.au” to get a better deal or more dental limits, we won’t have to wait another year for those same categories of care.

the actual act of switching is surprisingly simple and doesn’t require us to do much work at all. once we have picked our new fund, they will take care of canceling our old policy and moving all of our records over through a standard process. as suggested by “privatehealth.gov.au”, we should try to review our protection every year or two to make sure it is still serving us well. for example, as we grow from being single to having kids, or as we move closer to our retirement, what is important for our health changes. a plan that was great for us in our 20s might not be the best value or give us the specific care we need once we hit our 40s in the private health cover au landscape.

when we are comparing different funds for a potential move, we always look at more than just the lowest price tag. we think about things like the company’s reputation for helping customers, how easy it is to use their phone app for claims, and what kind of agreements they have with dentists or eye doctors to keep our out-of-pocket costs low. many of these funds also offer great deals to get us to join, like “six weeks free” or promising to waive some of the shorter waiting periods. while those deals look great, we always make sure the core policy is solid so we aren’t trading long-term security for a quick discount. switching remains our best weapon for keeping prices low and ensuring we always get the best private health cover au for our families.

WHAT’S NOT COVERED? COMMON EXCLUSIONS

while having private health cover au gives us a lot of protection, we also have to be very clear about what it simply cannot do. perhaps the biggest misunderstanding is the idea that private cover pays for our visits to the local gp. in australia, our doctor visits and any specialist appointments that happen in their private rooms are only covered by medicare and cannot be insured by law. this is part of our government’s plan to make sure basic healthcare is open to everyone through the public system, though it does mean we might still have to pay “gap” fees for those visits if our doctor doesn’t offer bulk billing.

WARNING:

private health insurance cannot cover out-of-hospital medical services like gp visits; these are the exclusive domain of medicare.

another big exclusion we often see in the lower-tier hospital plans is certain clinical areas. if we have a “bronze” plan, for instance, we are usually excluded from claiming for big operations like having a hip replaced or having cataract surgery. if we find ourselves needing one of those, our private fund won’t pay any of the costs in a private setting. as “health.gov.au” notes, we would have to upgrade our plan to a higher tier—usually gold—and then wait another 12 months before we could use those benefits. this is why we must be very honest with ourselves about our likely future risks when we are picking our plan level each year for private health cover au.

furthermore, it is very important for us to know that most hospital plans do not automatically give us ambulance cover. emergency transport is a service managed by our individual states, and the costs can be incredibly high if we don’t have protection. while some of our health funds add ambulance cover for free as a bonus, others make us pay for it as an extra or join a state scheme like “ambulance victoria”. we always double-check this tiny detail, because having to worry about a massive ambulance bill should be the very last thing on our minds during an actual medical crisis.

IS PRIVATE HEALTH INSURANCE WORTH IT? A FINAL VERDICT

after we have looked at all the different parts of private health cover au, we have to ask the big question: is it actually worth the money? for many of us, the answer is a firm “yes,” though the reasons are different for everyone. for a young couple thinking about a baby, the chance to pick their own doctor and stay in a private hospital is easily worth the monthly price. for our older citizens, the knowledge that they can have a knee surgury in a few weeks rather than waiting for years can completely change their life. choice and speed are the two main things we are buying with our insurance dollars.

TIPS:

always review your policy before your life circumstances change (e.g., turning 31, getting married, or planning a baby) to ensure you are covered.

You Might Also Like

from a purely money-focused view, the “worth” of our insurance often depends on how much we earn and our specific tax situation. for those of us who make enough to hit the medicare levy surcharge levels, the “actual cost” of our policy is often very small or even zero once we count the tax we would have otherwise lost to the ato. in those cases, it is almost always smart for us to get at least a basic hospital plan to protect our savings. similarly, for those who use a lot of “extras” like major dental work, the money we get back through the year can often cover a big chunk of our total annual insurance bill for private health cover au.

at the end of the day, the real value of our private insurance is the security it brings—the comfort in knowing that if something goes wrong, we have lots of options outside of the crowded public hospitals. while medicare is a brilliant asset that we are lucky to have in our nation, private cover is that extra layer that makes our medical journey as smooth, fast, and comfortable as it can be. we truly believe that by staying informed, picking the right level of cover for our needs, and checking our plan often, private health cover au remains one of the most important investments we can make in our future peace of mind and health.

YOUR TOP PRIVATE HEALTH COVER QUESTIONS ANSWERED

we often hear from lots of aussies who are a bit confused about how their private health cover au works in the real world. one of the most common questions we get is: “do i still need my medicare card if i have a private plan?” the answer is a big yes. medicare is the base of our whole system; it still pays for 75% of the official fees for our private hospital care and still covers our visits to the local doctor. our private plan is just a “top-up” that takes care of the gaps and lets us use private facilities, but it never takes away our basic right to public care under medicare at any time.

another thing people often ask us is if they are covered for accidents right after they join. most of our reputable health funds in australia have “accident cover,” which means they waive that standard 2-month wait for hospital care if the injury comes from a real, unexpected accident that happens after we became members. as “medibank.com.au” and “bupa.com.au” often point out, this gives a lot of peace of mind to active families who might be worried about sports injuries or sudden mishaps. however, we always suggest checking how your specific fund defines an “accident,” as those rules can be slightly different from one company to the next in the private health cover au market.

finally, many of us ask: “is health insurance the same price all over australia?” while the rules for the gold, silver, bronze, and basic levels are the same in every state, the actual price we pay for our premiums can change depending on where we live. this is because the cost of medical care and hospital space is different in places like perth compared to sydney or regional towns. as well, the rules for ambulance cover are different in every state, with people in queensland and tasmania getting government-funded cover while the rest of us have to manage it privately. we should always make sure our insurance fund knows exactly where we live so they can give us the right price and coverage info for private health cover au.

CONCLUSION

navigating through the world of private health cover au might seem like a lot to handle at first, but it is a path that is well worth taking to protect our most valuable asset: our health. by understanding the difference between hospital and extras cover, getting a handle on the tier system, and being aware of the waiting periods and tax perks, we can build a health plan that is both powerful and affordable for us. our australian system is built to reward those of us who think ahead, and by making shared decisions today, we are securing a faster and more comfortable future for ourselves and the people we love.

we must always remember that our health needs are constantly changing, and our insurance should change with us. as we move through the different chapters of our lives—from our first job to starting our own families and eventually into our retirement—taking the time to check and maybe even switch our health fund is the sign of a smart consumer. the government rebates and portability rules are there for our benefit, and we should use them to their full potential. private cover is much more than just another monthly bill; it is a deep commitment to a standard of care that lets us live our lives with total confidence, knowing we are ready for whatever might happen in the private health cover au landscape.

in closing, we invite you to use the resources from “health.gov.au” and “privatehealth.gov.au” to weigh up different plans and find the one that fits our unique way of life. whether we are just looking for a basic plan to save on our yearly tax or a high-end gold policy for complete peace of mind, there is a private health cover au option out there that is perfect for us. by taking this initiative, we aren’t just looking after our own well-being—we are also helping to keep our entire australian healthcare system strong and sustainable for everyone. here is to our collective health, our power of choice, and a very secure future for every one of us in this great nation.