private health insurance uk cost: comprehensive guide 2026

Figuring out the true private health insurance uk cost usually feels like a frustrating guessing game. Even though we desperately want reliable medical protection, expensive monthly premiums quickly become a massive financial barrier. Straight answers are surprisingly scarce.

To clear up this confusion, our overview breaks down exactly what dictates these recurring expenses. We look closely at why prices spike and examine practical tricks to shrink our quoted rates. Before signing any contracts, checking how a standard private health insurance uk cost aligns with our long-term budget is an absolute necessity.

Whether we need individual coverage or an expansive family plan, getting the math right matters most. Let us strip away the typical sales jargon and examine the actual numbers providers often hide.

Note:

we update our guides regularly to reflect the latest market trends affecting

private health insurance uk cost. the prices mentioned

here are estimates based on 2026 data and can vary by provider.

key takeaways for private health insurance uk cost

- average monthly premiums range from £30 to over £100, varying your private health insurance uk

cost. - age is the single biggest factor influencing the private health insurance uk cost of your

policy. - adding a moratorium or increasing your excess can significantly lower your premiums.

- postcode lottery is real; where you live affects what you pay.

- comprehensive cancer cover is a major value addition but adds to the cost.

how much does private health insurance cost in the uk?

it is the question everyone asks first: what is the damage? honestly, there is no single figure that applies to

everyone because determining your specific private health insurance uk cost is personal. however,

to give you a ballpark figure, most people in the uk pay somewhere

between £30 and £100 per month for a standard policy. buying a basic plan in your 20s might cost as little as a gym

membership, while comprehensive cover in your 60s could rival your monthly car finance payment. ultimately, the

private health insurance uk cost varies significantly based on individual circumstances.

the wide range in private health insurance uk cost exists because insurers look at risk. if you are

young and healthy, the likelihood of you claiming is

statistically lower, so your price is lower. conversely, if you are older or have a history of medical issues, the

insurer anticipates higher costs and charges accordingly. it is also worth noting that “budget” policies exist which

cover only in-patient treatment, while “premium” options cover everything from gp appointments to mental health

support.

is it cheaper to pay for treatment yourself?

for one-off minor treatments, sometimes yes. however, for serious conditions or

surgeries like hip replacements (which can cost £12,000+), insurance is far more cost-effective in the long

run than paying the full private health insurance uk cost out of pocket.

private health insurance uk cost: average monthly premiums

age is the compass by which insurers navigate your premium. generally speaking, for every decade you add to your

life, you can expect your private health insurance uk cost to tick upward. here is a rough breakdown of what average

monthly

premiums look like across different age bands.

in your 20s and 30s, you are in the “sweet spot” for pricing, keeping your private health insurance uk

cost low. premiums often sit between £25 and £45 per month.

health issues are less common, benefiting your private health insurance uk cost, and insurers are

keen to get you on board early. by the time you reach your 40s, you

might see this creeping up to between £45 and £70. this is the age where lifestyle factors and early signs of wear

and tear on the body start to factor into the actuarial tables.

Tips:

locking in a policy while you are young can sometimes help you avoid exclusions later,

as you enter the policy with a clean bill of health.

once you hit your 50s and 60s, the private health insurance uk cost jump can be more significant.

premiums can range from £70 to well over £120.

sadly, this is often when people feel they need cover the most. for those over 70, costs can exceed £150 or £200 a

month, depending on the level of cover chosen. it seems unfair that costs rise just as income often becomes fixed in

retirement, but that is the reality of the risk-based model.

factors that influence private health insurance uk cost

while age is the headline act, there are plenty of supporting characters in the story of your premium. understanding

these can help you tweak your quote. location is a surprisingly big one. if you live in central london or near

expensive private hospitals, your premium will be higher than someone living in a rural area with lower hospital

facility costs. this geographic factor plays a huge role in your final private health insurance uk cost.

smoking status is another major lever on your private health insurance uk cost. smokers can pay

significantly more—sometimes up to 50% more—than non-smokers.

quitting not only helps your lungs but also your wallet. insurers usually require you to be nicotine-free for at

least 12 months (including vaping) to be classified as a non-smoker.

your current health and bmi also play a role in determining private health insurance uk cost, though

most standard policies are sold on a “moratorium” basis (more on

that later) which doesn’t require a full medical upfront. however, if you undergo full medical underwriting, a high

bmi or history of high blood pressure can load your premium.

Warning:

never lie about your smoking status or medical history. if you do, your insurer can

refuse to pay out when you make a claim, leaving you with nothing.

level of cover affecting private health insurance uk cost

not all policies are created equal, and this choice massively impacts private health insurance uk

cost. a basic policy might only cover you for “in-patient” treatment—meaning tests and

surgeries that require a hospital bed. this is the cheapest way to get private cover and protects you from the big,

expensive procedures. but it won’t help with the initial consultations or diagnosis.

adding “out-patient” cover allows you to see consultants and get diagnostic tests (like scans and blood tests)

privately without waiting for an nhs referral. this usually adds 20-30% to the cost but significantly speeds up the

entire potential treatment journey. many people find this upgrade worth the extra expense for the sheer speed of

diagnosis.

can i change my cover level later?

yes, most insurers allow you to adjust your cover at renewal. you can add out-patient

cover or reduce it if you need to save money.

cancer cover is another critical component of private health insurance uk cost. most comprehensive

policies include full cancer cover, including access

to drugs not available on the nhs. reducing or removing this cover can slash premiums, but it removes one of the

primary safety nets people buy insurance for. think carefully before stripping this out.

excess and its impact on private health insurance uk cost

just like car insurance, your health policy will usually have an “excess”—the amount you agree to pay towards the

cost of a claim. this is one of the most effective tools you have to control your monthly premium. a standard excess

might be £100 per year, but raising it can lower your overall private health insurance uk cost.

if you agree to a higher excess, say £500 or £1,000, your monthly premium will drop. this is because you are taking

on a small part of the financial risk yourself. for healthy individuals who don’t expect to claim often, a

high-excess policy can be a very smart financial move. you keep your monthly outgoings low but retain the

“catastrophe cover” for serious conditions.

Remember:

check if your excess is per year or per claim. a per-year excess is generally much

better value as it caps your contribution regardless of how many treatments you need.

it is important to check if the excess is “per claim” or “per year”. a “per year” excess is much friendlier, as you

only pay it once regardless of how many times you need treatment in that policy year. a “per claim” excess can add

up quickly if you have a complex condition needing multiple visits.

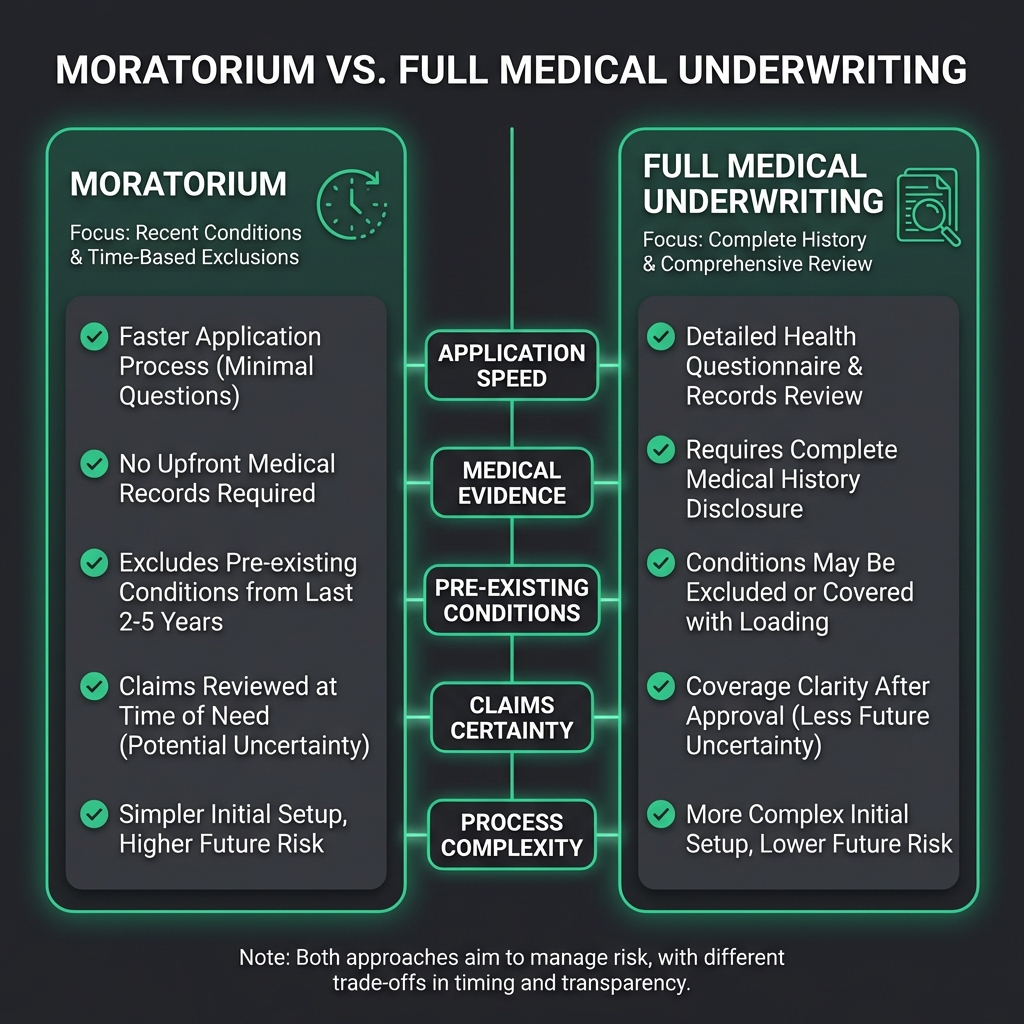

moratorium vs. full medical underwriting impact on private health insurance uk cost

when you buy a policy, you will be asked how you want to be underwritten. “moratorium” is the most common and usually

the default. under this, you don’t answer detailed medical questions. instead, the insurer says: “we won’t cover any

pre-existing conditions you have had in the last 5 years.” if you go 2 years on the policy without treatment for

that condition, it might then become covered. it is fast and often cheaper.

“full medical underwriting” (fmu) involves filling out a long questionnaire about your medical history. the insurer

then tells you exactly what is and isn’t covered from day one. while this gives you certainty, it can be more

expensive if you have a history of illness, and the application process is slower. however, for some with specific

histories they want clarity on, it is the better path.

what if i forget to mention a condition?

with moratorium underwriting, you don’t need to declare it upfront. but with full

medical underwriting, nondisclosure can void your policy. always take your time with the forms.

does private health insurance cover pre-existing conditions?

generally speaking, the answer is no. private health insurance is designed to cover “acute” conditions—illnesses that

start after your policy begins and can be cured. “chronic” conditions (like diabetes or asthma) that you already

have are almost always excluded.

this can be a shock to new buyers. you cannot buy insurance to fix a knee you injured three years ago. however, some

providers have “switch” policies where, if you are moving from one insurer to another, they might honour your

existing coverage terms, effectively covering those pre-existing conditions that were covered by your previous

insurer. this is known as “continued personal medical exclusions” (cpme).

Warning:

don’t cancel your old policy until the new one is fully set up and you have confirmed

that your pre-existing conditions are covered if you are switching.

family and joint policy discounts

buying as a couple or a family is often cheaper per person than buying individual policies. insurers love stability,

and families represent stable, long-term customers. discounts for couples can range from 5% to 10%, effectively

lowering your private health insurance uk cost.

many providers also offer “kids go free” deals or highly subsidised rates for adding children to a policy. if you

have a large family, looking for a provider that charges for the first child but covers subsequent siblings for free

can lead to massive savings. it is worth shopping around specifically for these family-friendly perks.

Tips:

compare the cost of separate policies vs. a family one. sometimes, if one parent has a

complex medical history, it’s cheaper to insure them separately to avoid loading the premium for everyone.

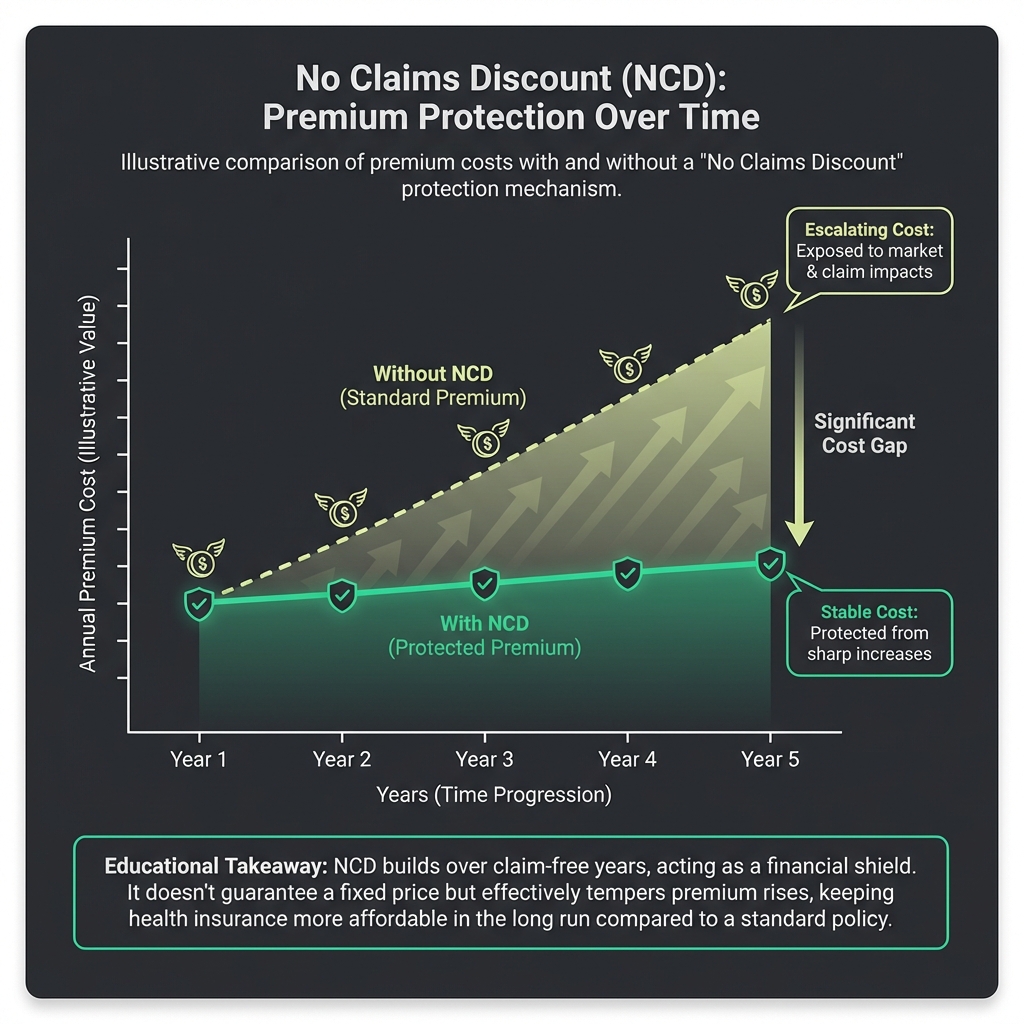

no claims discount (ncd) explained

the concept of a no claims discount is familiar to drivers, but it works slightly differently in health insurance and

is vital for managing private health insurance uk cost. if

you don’t make a claim, your renewal price should theoretically stay lower, or increase less than it otherwise

would. some insurers offer a structured ncd scale, giving you a percentage off for every claim-free year.

however, be aware that medical inflation (the rising cost of healthcare) happens every year regardless of your

claims. so, even with a no claims discount, your premium might still rise slightly simply because healthcare is

getting more expensive overall. protecting your ncd is an option with some insurers, allowing you to make a small

claim without losing your discount level.

will my premium go up if i claim?

usually, yes. claiming often reduces your no claims discount, leading to a higher

renewal price. it’s worth weighing up the cost of the treatment vs. the long-term premium increase.

comparing the top uk insurers for the best private health insurance uk cost

the uk market is dominated by a few big names: bupa, axa health, aviva, and vitality. each has a different “flavour”.

bupa is the household name with a massive network but can be pricier. axa health offers great flexibility. aviva

often provides solid comprehensive cover at competitive rates.

vitality is the disruptor, gamifying health insurance. they offer rewards (like free coffee, cinema tickets, and

apple watches) if you track your activity and stay healthy. for active people, vitality offers incredible value, but

for those who prefer a simpler, traditional insurance product, the complexity of points and rewards can be

overwhelming. comparing them isn’t just about price; it is about lifestyle fit.

Note:

some insurers like vitality require you to use specific wearables or apps to unlock the

best rewards and lowest private health insurance uk cost. make sure you are comfortable with this tech

aspect.

hidden costs to watch out for in your private health insurance uk cost calculation

the monthly premium isn’t the only private health insurance uk cost. watch out for “hospital lists”. insurers tier

hospitals. a standard policy

might cover most hospitals in the uk but exclude expensive central london facilities. if you want access to those

prestige london hospitals, you have to upgrade your hospital list, which increases your premium.

another hidden cost is the “shortfall”. sometimes an anaesthetist or surgeon charges more than the insurance

company’s limit for a procedure. you would be liable for the difference. always check with your insurer that the

specialist’s fees are fully covered before you go ahead with treatment to avoid a nasty bill later.

Warning:

always get pre-authorization from your insurer before any treatment. if you proceed

without it, you might be left footing the entire bill yourself.

is private medical insurance worth the private health insurance uk cost?

this is the ultimate question. if you are happy to rely on the nhs for emergencies (which you have to do anyway) and

don’t mind waiting for elective surgeries, you might decide to save your money. the nhs is fantastic for critical,

life-threatening care. private insurance shines for “quality of life” issues—bad knees, cataracts, hernias—where nhs

waiting lists can be months or years long, making the private health insurance uk cost justifiable.

for self-employed people, the value is clearer: time is money. waiting six months for surgery while unable to work is

a financial disaster. having insurance means getting back on your feet and back to work weeks sooner. it is buying

speed and convenience as much as healthcare. for many, the private health insurance uk cost is worth it for this

reliability.

can i use private insurance for emergencies?

no, private insurance is generally for planned, non-emergency treatments. for accidents

and emergencies, you should always go to an nhs a&e department.

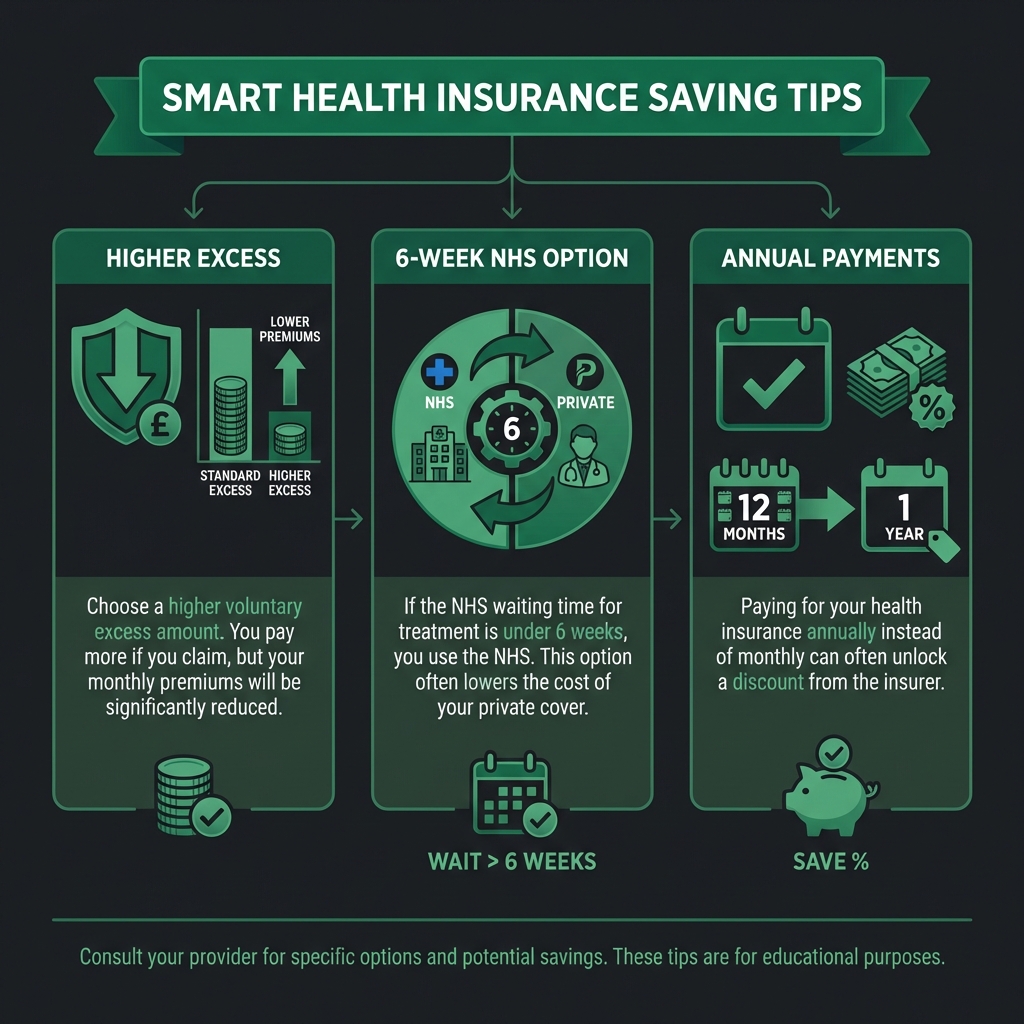

tips to reduce your private health insurance uk cost

if the quote comes back too high, don’t just walk away—negotiate by tweaking the policy. first, raise your excess.

moving from £0 to £250 excess can save you a chunk of cash. second, look at the “6-week nhs option”. this brings the

price down significantly by agreeing that if the nhs can treat you within 6 weeks, you go nhs. if the wait is

longer, you go private.

finally, consider paying annually. most insurers charge a small interest percentage for paying monthly. if you can

afford to pay the lump sum upfront, you instantly save that 5-10% interest charge. it is a simple win if your cash

flow allows it.

Tips:

use a broker. they often have access to broker-exclusive deals that you won’t find on

comparison sites, and they can help you understand the fine print.

conclusion

private health insurance in the uk is a significant financial commitment, but for many, the peace of mind is

priceless. costs vary wildly based on who you are and what you want covered, but understanding the levers—age,

excess, and cover levels—puts you in control.

we recommend getting quotes from multiple providers or using a specialist broker. they can navigate the fine print

better than a comparison site algorithm. remember, the cheapest policy isn’t always the best; the best policy is the

one that is there for you when you actually need it, balancing quality care with a manageable private health

insurance uk cost.

medical disclaimer:

the information provided in this article is for educational and informational purposes only and does not

constitute medical or financial advice. insurance policies vary by provider and individual circumstances. always

consult with a qualified insurance broker or financial advisor before making decisions about your health

coverage. we do not guarantee the accuracy of pricing as rates fluctuate constantly.