AUSTRALIAN HEALTH PLANS: Your Guide to Success 2026

have we ever considered how australia manages to consistently rank among the most effective and efficient healthcare systems on the planet? according to rigorous analysis by “the commonwealth fund”, the unique infrastructure we utilize provides a comprehensive safety net through medicare while simultaneously fostering a dynamic private sector. this sophisticated hybrid model ensures that we can access essential care regardless of our financial standing, while offering clear incentives for those of us who choose to contribute more to our own specialized treatments. as we begin to explore the deep complexities of australian health plans, we encounter a landscape that is both rewarding and challenging, prioritizing the collective well-being of our population through a strategic balance of public funding and private initiative.

navigating the wide array of australian health plans can often feel like a massive undertaking for both lifelong residents and those new to our shores. we frequently find ourselves overwhelmed by the sheer volume of choices, ranging from entry-level hospital cover to premium private health insurance australia extras that include everything from major dental work to complex physiotherapy. our mission with this comprehensive guide is to demystify the complex terminology, clarify the tax implications, and help us all understand how to maximize the benefits of the australian healthcare system. we strongly believe that making informed choices leads to superior health outcomes and long-term financial stability, which is why we have developed this detailed investigation into the mechanisms that keep australians healthy. whether we are aiming to avoid the medicare levy surcharge or simply want to ensure our families have access to the highest quality specialists, mastering these australian health plans is the essential first step on our wellness journey.

IS HEALTH INSURANCE COMPULSORY IN AUSTRALIA?

while medicare is a universal system for all australian citizens and permanent residents, private health insurance is not mandatory. however, the government uses tax incentives and surcharges to encourage us to take out private hospital cover, especially if our income is above a certain level.

we must also acknowledge the pivotal role that government policy plays in determining the availability and actual cost of various australian health plans. through a structured system of rebates, levies, and loadings, the australian government actively promotes participation in the private market to alleviate pressure on our public hospital infrastructure. this strategy creates a highly competitive environment where insurers are pushed to innovate and provide genuine value for our memberships. as we dive deeper into the specifics of hospital tiers, waiting periods, and the often-misunderstood “gap,” we will observe how these components merge into a robust framework for our national health management. our shared health remains australia’s most significant asset, and by selecting the most appropriate australian health plans, we help build a sustainable and high-quality healthcare legacy for future generations.

NOTE:

the australian health plans system is designed to provide universal access through medicare while allowing individuals to upgrade their experience through private insurance. this dual-track model is highly praised by “the commonwealth fund” for its ability to balance equity and choice.

KEY TAKEAWAYS

- australia operates a dual healthcare system consisting of public (medicare) and private health insurance.

- private health insurance is divided into hospital cover, extras cover, and combined plans.

- hospital cover is categorized into four tiers: gold, silver, bronze, and basic to simplify comparisons.

- tax incentives like the medicare levy surcharge and the private health insurance rebate encourage private cover.

- lifetime health cover (lhc) loading adds a 2% surcharge for every year you delay private hospital cover after age 31.

- the “gap” refers to the difference between what a doctor charges and what medicare and your insurer pay.

- waiting periods apply to most new policies for pre-existing conditions and certain elective services.

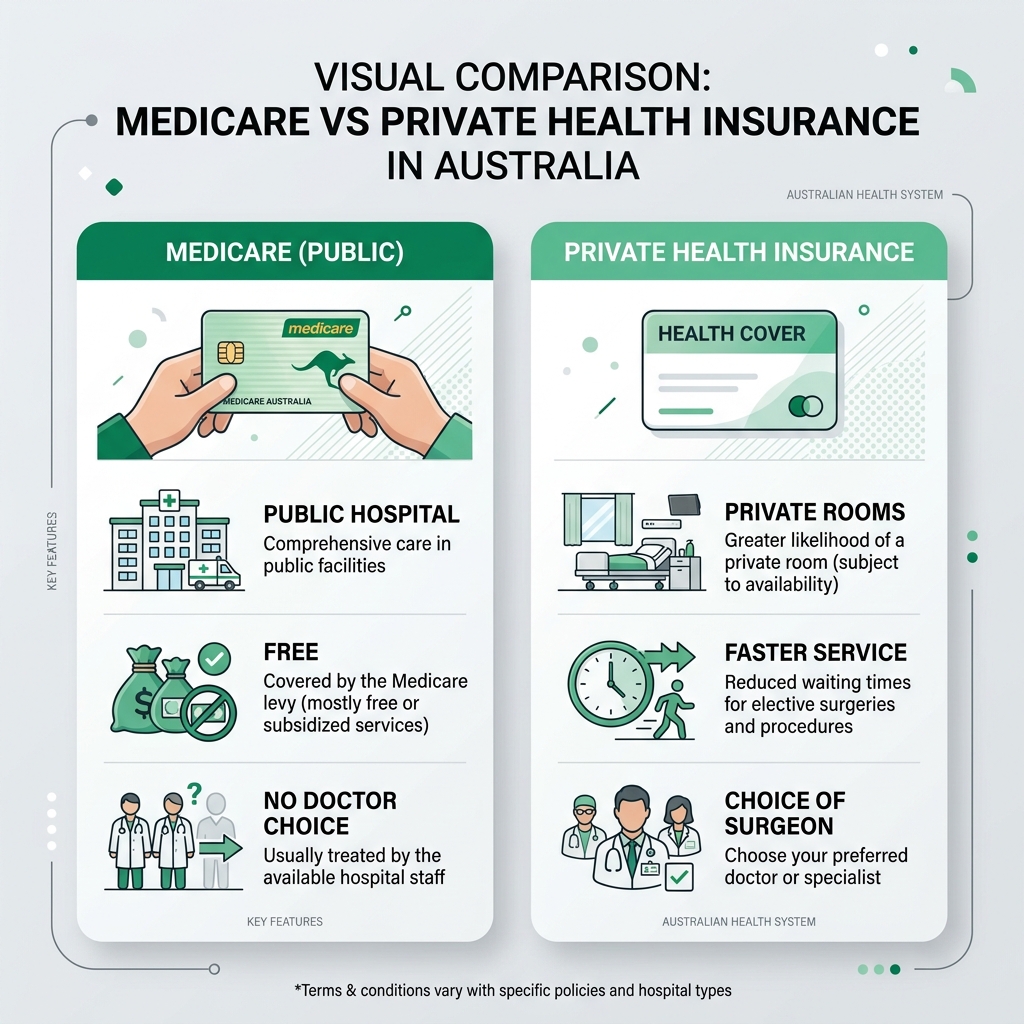

UNDERSTANDING THE AUSTRALIAN HEALTHCARE LANDSCAPE: PUBLIC VS. PRIVATE

whenever we discuss the diversity of australian health plans, we are essentially looking at a unique partnership between the state and the individual. the public system, famously known as medicare, offers us universal access to critical medical services, including completely free treatment in public hospitals and subsidized visits to our local gp. however, the private system operates as a powerful parallel, providing features that the public safety net does not encompass, such as the ability to choose our own doctor in a private facility or bypassing long wait times for elective procedures. we have consistently seen that the most effective health outcomes occur when we utilize both branches of the system strategically. by maintaining private health insurance australia, we reduce the burden on public resources, ensuring they remain robust for those in most urgent need while securing our own pathway to rapid care.

TIPS:

we found that using medicare for secondary consultations while maintaining private hospital cover for specialists provides a balanced approach. it allows us to save on day-to-day costs while staying protected for major events.

the clear distinction between these two primary sectors is vital for anyone attempting to manage their personal health finances over the long term. while medicare is essentially funded through our general tax contributions, private insurance requires us to make regular premium payments to a registered provider of our choice. we have observed that many australians view private cover as much more than just a medical fallback; it is a lifestyle investment that grants us significantly more autonomy over our medical journey. the “world health organization” frequently cites the strengths of this mixed model, noting that it maintains a very high standard of care across a wide range of demographics. our shared duty is to recognize exactly where medicare’s coverage ends so we can decide which australian health plans are best suited to fill the gaps in our personal health defense.

MEDICARE: THE FOUNDATION OF AUSTRALIAN HEALTHCARE

we consider medicare to be the very heartbeat of our medical infrastructure, having been founded in 1984 to provide every australian with fair access to treatment. it is primarily supported by a 2% levy on our taxable income, which most of us contribute as part of our standard tax commitments. we all benefit from this system in three major areas: it manages the entire cost of public hospital admissions, provides free or heavily subsidized doctor visits through the medicare benefits schedule, and lowers the cost of prescription drugs via the pharmaceutical benefits scheme. without this critical foundation, the expense of even a minor consultation or life-saving surgery would be completely out of reach for many in our community. we must value the fact that medicare guarantees a baseline of care and dignity for every person living on our shores.

REMEMBER:

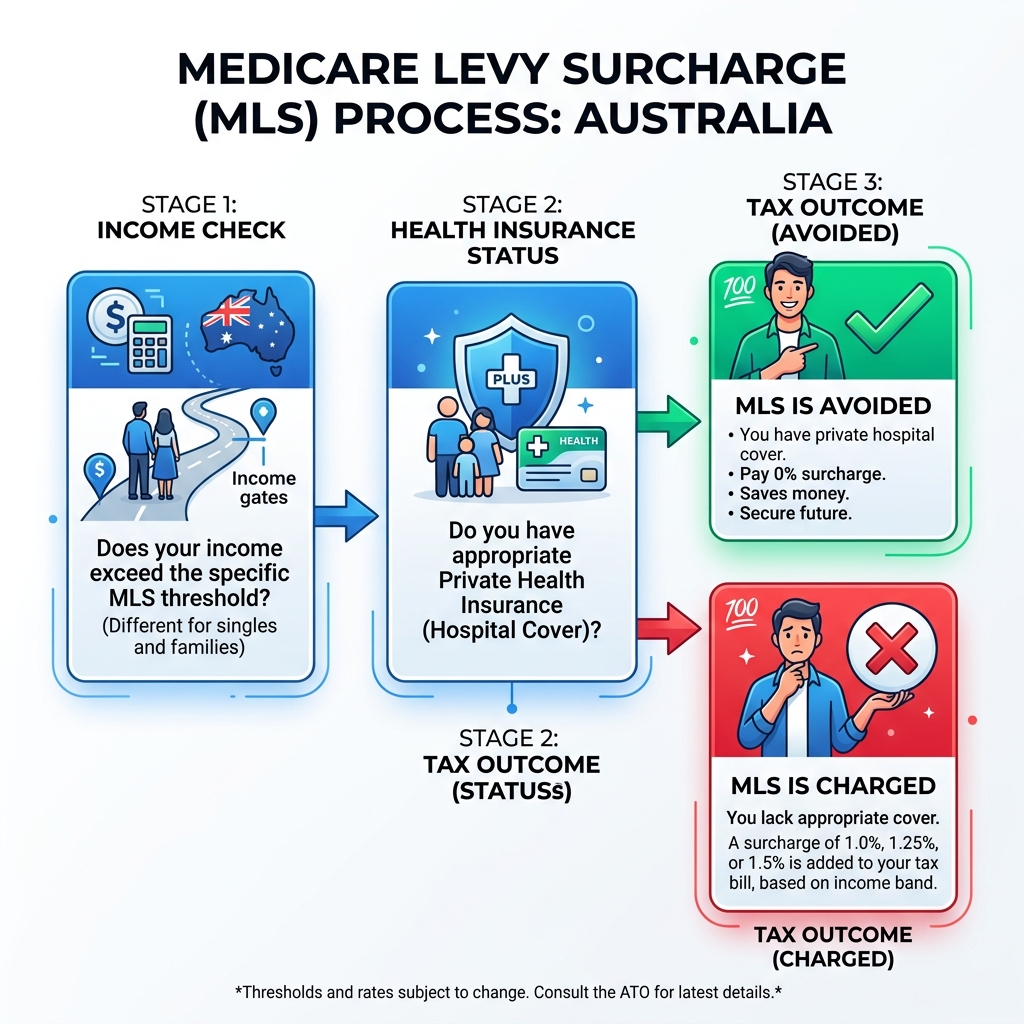

the medicare levy is usually 2% of your taxable income. however, this is separate from the medicare levy surcharge (mls), which only applies to those without private hospital cover who earn above a specific threshold.

nevertheless, we have to admit that medicare is not designed to be a catch-all for every medical need, which is precisely why so many of us begin investigating more specialized australian health plans. services such as private hospital accommodation, extensive dental work, physiotherapy, and corrective optical gear are generally not supported by the public fund. we also frequently encounter much longer waiting lists for non-urgent surgeries in the public sector, which can be a massive disadvantage for those managing chronic but not immediately life-threatening conditions. by fully grasping these inherent limitations, we are much better prepared to evaluate our personal need for additional private cover. medicare remains our ultimate safety net, but we must decide how to build upon it to ensure our total health security.

WARNING:

visits to private hospital emergency departments are usually not covered by private hospital insurance. these are often considered outpatient services, meaning you may be responsible for the full consultation fee even if you have premium australian health plans.

WHY MANY AUSSIES OPT FOR PRIVATE HEALTH INSURANCE

there are several very persuasive reasons why we might choose to sign up for private health insurance australia even with the existence of a high-quality public system. for many of us, it is primarily about having control and flexibility; we want the right to pick our own specialists, and those specialists often operate exclusively within private hospital networks. additionally, being able to bypass the long public waiting lists for elective procedures like hip replacements or cardiac care is a significant motivator for our families. we also deeply value the increased comfort that comes from having a private room and a quieter environment for recovery. modern australian health plans provide a level of customized care that a universal public system simply cannot match in every scenario.

WHAT HAPPENS TO WAITING TIMES WITH PRIVATE INSURANCE?

having private insurance typically allows us to bypass the public waiting lists for elective surgeries. while urgent care is always handled quickly in public hospitals, private care ensures you get your non-urgent procedures done on your own schedule.

another major factor in our decision-making is the array of financial incentives provided by the australian government. for those of us with higher incomes, the medicare levy surcharge can often be more expensive than the actual premiums of an entry-level private hospital policy. we also take advantage of the private health insurance rebate, which is a significant government contribution toward our costs based on our age and how much we earn. by choosing to take out private cover, we are not only protecting our physical well-being but also our financial health by avoiding tax penalties and securing subsidies. this is a strategic move that millions of us make every year, highlighting the vital role of private providers within the broader australian health plans economic landscape.

NOTE:

the medicare levy surcharge can range between 1% and 1.5% of your taxable income. we suggest calculating if the surcharge is higher than the cost of a basic hospital plan to see if you can save money while getting covered.

You Might Also Like

TYPES OF PRIVATE HEALTH INSURANCE PLANS IN AUSTRALIA

we typically categorize private health insurance into three distinct areas: hospital cover, extras cover, and combined cover. hospital cover is specifically built to help us manage the high costs of being a private patient, encompassing theater fees and specialist accommodation costs. extras cover, which we often call ‘ancillary’ insurance, helps us pay for those vital services outside of the hospital that medicare rarely covers, such as dental care, optical needs, and physiotherapy. we always suggest that the most effective way to evaluate these australian health plans is to look at our family’s medical history and anticipate our future needs. by picking the right type of policy, we ensure we aren’t wasting money on services we won’t use while maintaining total protection where it counts.

TIPS:

select a plan that aligns with your current life stage. for instance, young professionals might prioritize dental and optical extras, while families should focus on speech therapy and orthodontics for children within their australian health plans.

many of us find that combined cover is the most straightforward solution for our health management needs. these policies bundle hospital and extras together into one convenient package, often providing us with a small discount compared to buying them separately. however, we must be diligent in reviewing the ‘benefit limits’ and individual caps that apply to each service in an extras plan. for example, a policy might claim to offer “comprehensive” dental but have a very restrictive cap on major orthodontic work. by comparing different formats of australian health plans, we can strike a balance that fits our current lifestyle, whether we are young and independent or managing chronic conditions that require frequent allied health support. our goal is to always find the most direct path to wellness through smart insurance selection.

HOSPITAL COVER: WHAT’S INCLUDED AND WHAT’S NOT?

we recognize that hospital cover is the absolute cornerstone of most private australian health plans, focusing on the massive expenses of inpatient treatment. when we are admitted as private patients, our insurance works to cover the costs of nursing care, the hospital theater, and our accommodation. we are also permitted to claim for the medical devices used in our procedures, such as pacemakers or orthopedic pins. it is vital for us to realize that while the policy pays for these hospital-specific costs, we might still be liable for a portion of the doctors’ fees if they charge above the rates set by the government. this makes it essential for us to request a white-and-black quote before any surgery to prevent unexpected bills.

REMEMBER:

most clinicians charge the medicare schedule fee, but some charge more. this difference is known as the “gap,” and it is an out-of-pocket cost you must pay unless your insurer has a gap cover agreement with that specific doctor.

it is just as important for us to be aware of what is usually excluded from standard hospital cover. we find that most basic and even some bronze plans do not include pregnancy or birth-related coverage, which typically requires a higher-level gold policy and a 12-month waiting period. similarly, complex medical procedures like spinal surgery or dialysis are often limited to the most expensive categories of insurance. we should also keep in mind that emergency department visits at private hospitals are not generally covered by our policies, as they are treated as outpatient services. by carefully examining the fine print of our australian health plans, we can ensure our expectations match the reality of our cover when we need it most.

WARNING:

be aware that exclusions and restrictions apply to many lower-tier policies. if a service is “restricted,” it means your insurer only pays a small amount toward a public hospital bed, leaving you with significant costs in a private setting.

EXTRAS COVER: DENTAL, OPTICAL, AND BEYOND

we often interact with extras cover more frequently than any other part of our australian health plans, as it supports our day-to-day wellness. we rely on these policies to help cover the cost of our regular dental cleaning, our new glasses, and those necessary physiotherapy sessions after we pick up a minor injury. these services are absolutely essential for maintaining our quality of life and preventing minor health issues from escalating into major problems. many in our community find that the true value of extras comes from these frequent, smaller claims that gradually add up over the year. by taking full advantage of our extras, we are participating in the type of preventive health that “the lancet” describes as the most effective way to lower the global burden of disease.

CAN I GET EXTRAS WITHOUT HOSPITAL COVER?

yes, many providers allow us to purchase standalone extras policies. this is great if you are happy with medicare for hospital needs but want help with dental, optical, and physiotherapy costs throughout the year.

however, we must always keep a close eye on the ‘benefit limits’ that are attached to our extras. every policy has a strict maximum amount it will pay for any given service in a year; once we hit that ceiling, we are responsible for the full cost of any further treatments until the plan resets. some australian health plans also feature ‘lifetime limits’ for specific high-cost services like orthodontics, meaning once we claim that total, we can never claim for it again. we strongly encourage everyone to shop around and find a policy that distributes its limits toward the services we use the most. for instance, if we have ongoing eye issues, a plan with high optical limits and lower podiatry limits within our private health insurance australia framework would be a much better fit for us.

NOTE:

check your benefit percentage. some plans pay a fixed amount per service, while others pay a percentage (e.g., 60% or 75%) of the cost. we found that percentage-based plans are often easier to predict for budgeting purposes.

COMBINED COVER: FINDING THE RIGHT BALANCE

for a large number of us, the most convenient way to manage our overall well-being is through a combined policy that brings hospital and extras under a single roof. we have found that these australian health plans are usually tailored for specific stages of life, such as plans for ‘young families’ or ‘senior comprehensive’ options. by picking a combined policy, we can simplify our monthly administration and often gain access to valuable loyalty perks or wellness programs. these programs might result in discounted gym memberships or free health assessments, which further support our fitness goals. we believe that a well-designed combined plan provides the most comprehensive approach to using our health insurance effectively.

TIPS:

look for insurers that offer loyalty rewards. some australian health plans increase your extras limits or reduce your excess the longer you stay with them, providing long-term value for consistent membership.

TIERS OF HOSPITAL COVER: GOLD, SILVER, BRONZE, AND BASIC

to make the process of comparing different australian health plans much more transparent, the government recently introduced a mandatory tiered system for hospital insurance: gold, silver, bronze, and basic. this standardized framework ensures that every single policy within a tier must cover a specific minimum range of medical services. for instance, every bronze plan is required to cover procedures like joint reconstructions, while silver plans must also include coverage for heart and vascular treatments. we find this system extremely helpful because it allows us to compare different insurers on an “apples to apples” basis. if we know we need specialized care, we can instantly focus our search on the appropriate tier, saving us from countless hours of reading irrelevant policy documents.

REMEMBER:

the tier system applies only to hospital cover. extras plans are not standardized in the same way, so you still need to compare the specific benefits and limits for dental and optical across different australian health plans.

as we move up through the tiers, the coverage inevitably becomes more comprehensive, but our premiums will also increase accordingly. basic plans are often selected by those who simply wish to avoid tax surcharges and don’t anticipate needing much hospital care, whereas gold plans offer the highest level of protection, including things like obesity surgery and private health insurance australia pregnancy services. we have noticed that silver and “silver plus” plans often provide the most balanced value for growing families who want serious protection without the premium cost of a gold policy. by understanding which specific clinical categories are mandatory for each level, we can make a very precise choice based on our age and individual health risks. these tiers have finally brought some much-needed clarity to the world of australian health plans.

You Might Also Like

KEY FACTORS TO CONSIDER WHEN CHOOSING AN AUSTRALIAN HEALTH PLAN

beyond just looking at the type of cover, there are several systemic details we must analyze when we evaluate our options for australian health plans. the true cost of a policy isn’t just the monthly fee; it also includes any excesses or co-payments we might have to settle if we are admitted to a hospital. we also have to examine the ‘benefit caps’ on our extras and any ‘restrictions’ on hospital procedures. for example, a policy might cover a specific surgery but only if we are treated as a private patient in a public facility, which might not be what we originally wanted. we always advise everyone to consider their total “out-of-pocket” risk rather than just the initial price to get a true sense of a plan’s value.

we must also pay close attention to the reputation and member support record of each insurance provider. some funds have developed better working relationships with hospitals, which often results in fewer surprise costs for us, while others might offer better mobile apps that make claiming for our dental visits simple and fast. we highly value providers that integrate into our lives seamlessly, allowing us to focus on our recovery rather than on endless paperwork. by weighing these practical considerations alongside the actual clinical cover, we can ensure that our chosen australian health plans are both functional and reliable when we really need to use them. our health journey is unique, and our insurance should support us with relevant and easily accessible care.

WAITING PERIODS: MANAGING THE TRANSITION

we have to accept that waiting periods are a standard part of all australian health plans, designed to protect the system from people who only join when they already know they need surgery. for most general hospital and extras services, we typically have to wait 2 months, but this extends to 12 months for pre-existing conditions and pregnancy-related care. it is a system based on mutual responsibility, where we contribute to the collective fund for a while before we can claim significant benefits. we recommend planning well in advance if we are considering starting a family or scheduled surgery, as there is simply no way to skip these waiting periods once they are in place. starting our cover early is the only real way to ensure we are fully protected when the time comes to use it.

IS THE PRE-EXISTING CONDITION WAITING PERIOD ALWAYS 12 MONTHS?

yes, government regulations set a standard 12-month waiting period for any ailment or illness that existed in the 6 months prior to joining or upgrading. the only exceptions are psychiatric, palliative, and rehabilitation care, which usually have a 2-month wait.

THE “GAP”: UNDERSTANDING OUT-OF-POCKET COSTS

perhaps the most frequent source of confusion we encounter in australian health plans is the “gap.” this situation arises because doctors are legally allowed to charge whatever they feel is appropriate, which is often higher than the combined rebate from medicare and our private insurer. as a rule, medicare covers 75% of the schedule fee for inpatient services, with our insurance picking up the remaining 25%. if our surgeon charges 150% of that fee, we are left to pay the additional 50% ourselves. we have found that “gap cover” schemes offered by many insurers can help us avoid these costs, but only if our doctor agrees to participate in that specific plan. it is a critical detail that requires us to have open conversations with our medical team.

NOTE:

always ask your specialist for informed financial consent. this is a written estimate of all expected costs, including surgeons, anaesthetists, and hospital fees, so you can calculate your potential gap before the surgery.

we can significantly reduce our financial risk by choosing specialists and doctors who are known for having no gaps or who participate in our insurer’s preferred provider network. many modern australian health plans provide online search tools to help us locate these “participating” clinicians. we should also never hesitate to ask our specialist for informed financial consent before any procedure, which is a full breakdown of every expected cost. by being assertive and well-prepared, we can navigate the complexities of medical fees and ensure our insurance is doing the hard work of protecting our savings. it’s about being an active participant in our own healthcare to achieve both the best medical and financial results possible.

LIFETIME HEALTH COVER (LHC) LOADING: THE IMPORTANCE OF STARTING EARLY

we must also consider the lifetime health cover (lhc) loading, a government tool meant to keep the system sustainable by encouraging us to join early. if we don’t have a private hospital plan by the july 1st following our 31st birthday, we are charged a 2% loading on our premiums for every year we are over 30 when we finally sign up. for example, if we wait until we are 40 to get cover, we will end up paying 20% more than someone who joined at 30, and this penalty lasts for 10 years of continuous membership. we see this as a very strong nudge to get younger australians into the private system, ensuring that the risk pool remains diverse. it is a clear example of the “carrot and stick” approach used within the australian health plans framework.

WARNING:

the july 1st deadline after your 31st birthday is strict. missing this even by a few days could mean you are paying extra for your health insurance for a decade. plan ahead and get your cover active before you hit this age milestone.

for those of us who have spent significant time living overseas or who are recently arrived migrants, there are very specific sets of rules regarding lhc loading. generally, we have a 12-month grace period from the time we become eligible for medicare to sign up for private hospital cover before the loading begins to accrue. it is essential that we take these deadlines seriously, as the cumulative cost of the loading can add up to many thousands of dollars over time. by understanding and following these rules, we can keep our australian health plans affordable and avoid paying these unnecessary long-term penalties. these policies are designed to encourage us to participate early, making the entire private system more viable as our population ages.

You Might Also Like

TAX IMPLICATIONS OF HEALTH INSURANCE IN AUSTRALIA

the australian government effectively uses our tax system to manage the balance between public and private care through the medicare levy surcharge and the private health insurance rebate. we find that for many in our community, these tax factors are the number one reason to sign up for australian health plans. the system is built to be “progressive,” meaning that those of us with higher incomes get smaller rebates and suffer larger penalties if we don’t have private cover. we believe this strategy helps maintain the overall fairness of our system while providing a loud financial message to those who can afford to use the private market. understanding where we stand in terms of tax is key to making an informed and cost-effective insurance decision.

HOW IS THE REBATE CALCULATED?

the private health insurance rebate is tiered based on your income. there are three income tiers; the higher your income, the lower your rebate. as you get older (especially over 65), the percentage of the rebate increases.

we should also think about how our choice of insurance affects our annual tax return at the end of every financial year. if we have the right level of hospital cover, we can avoid the medicare levy surcharge entirely, which can save us between 1% and 1.5% of our entire taxable income. for high-income earners, the savings from avoiding this tax can actually be greater than the cost of the premiums themselves, making it a very logical financial move. we also have the option of taking our rebate as an immediate reduction in our premiums or claiming it as a lump sum later on. by aligning our australian health plans with our broader tax strategy, we can achieve more efficient financial results for our households while supporting the national budget.

MEDICARE LEVY SURCHARGE (MLS): AVOIDING THE EXTRA TAX STING

we understand the medicare levy surcharge (mls) as a specific tax penalty designed for those of us who earn above a certain threshold and don’t maintain private hospital insurance. it’s important that we distinguish this from the standard 2% medicare levy that nearly everyone in the workforce contributes. the mls is an extra charge intended to motivate us to use private facilities, which in turn reduces the demand on our public hospitals. we often see that people are shocked by this surcharge when they receive their tax bill, which only emphasizes the need for us to stay informed about our australian health plans options. if we find ourselves in a higher income bracket, opting for hospital cover is almost always the smartest way to protect our income from this unnecessary charge.

PRIVATE HEALTH INSURANCE REBATE: CLAIMING YOUR GOVERNMENT SUBSIDY

the private health insurance rebate is a long-standing government initiative that provides us with a direct financial contribution toward our insurance premiums. the exact percentage we receive is calculated based on our income tier and the age of the oldest person listed on the policy. as we grow older, that rebate percentage usually increases, highlighting the government’s commitment to helping seniors maintain their chosen australian health plans. for many australian families, this rebate is the factor that makes mid-tier or even high-tier policies truly affordable, allowing them to access great care without stressing their monthly budgets. it is a clear investment from the state into our collective well-being and the strength of our private healthcare market.

we are able to choose whether we want this rebate applied directly to our monthly bills, which keeps our cash flow higher, or if we prefer to claim it as a refundable tax offset when we file our returns. most in our community prefer the immediate relief of lower premiums, but we must be careful to estimate our income accurately at the start of the year. if we end up earning more than we predicted, we might find ourselves having to pay back some of that rebate when tax time rolls around. by staying mindful of these details, we can maximize the benefits of our australian health plans while avoiding any unpleasant surprises from the tax office. it is another layer of support that makes high-quality healthcare a reality for millions of us.

COMPARING THE “BIG FOUR” AND BEYOND: MEDIBANK, BUPA, HCF, AND HBF

the competitive landscape of australian health plans is largely dominated by what we call the “big four” providers: medibank, bupa, hcf, and hbf. together, these giants cover a massive portion of the insured population across the country. medibank is currently our largest provider, offering an incredible range of plans and a vast network of partner clinics. bupa, as a global healthcare entity, brings a lot of international expertise and advanced digital tools to the table for its members. on the other hand, hcf and hbf operate as “not-for-profit” mutuals, which means they are managed for the benefit of their members rather than outside shareholders. we have often found that these mutual organizations offer some of the highest member satisfaction ratings due to their focus on service.

nevertheless, we shouldn’t overlook the smaller, more specialized restricted funds that might be available to us. many of these providers are exclusively for people in specific industries, such as teachers, nurses, or mining employees, and they frequently offer australian health plans with extraordinary value. if we are eligible to join one of these funds, we might find that they outperform the big names in terms of both benefits and lower premiums. we believe that the best approach for us is to look beyond the massive brands and use a reliable comparison tool to see how all the available options measure up against our specific needs. the healthy competition in our market ensures that we, as consumers, have a wide variety of innovative choices to suit our unique circumstances.

You Might Also Like

HOW TO CHOOSE THE BEST HEALTH PLAN FOR YOUR LIFE STAGE

we must remember that our health needs are always fluctuating as we move through different phases of our lives, and our australian health plans should be flexible enough to reflect that. what works perfectly for a fit and independent 20-year-old is almost certainly going to be insufficient for someone starting a family or approaching their retirement years. we highly recommend that we all review our coverage at least every two years, or whenever we hit a major milestone like getting married or switching careers. by making sure our cover aligns with our current reality, we can avoid paying for services we no longer need while ensuring we have the right protection for our most likely future health events. it is a smart, proactive way to ensure our insurance remains a genuine asset throughout our entire lives.

we also need to think about which “extras” are most relevant to our current situation. a younger member might prioritize dental care and massage for sports recovery, while someone in their 40s might need more robust coverage for optical care and physiotherapy to manage the everyday strains of a busy life. for those of us in our 60s and beyond, our australian health plans might need to focus more on joint health and hearing support. by selecting a plan that offers high caps on the services we actually use, we get the best possible return on our premium dollars. our health is always evolving, and our approach to insuring it should be just as dynamic and forward-thinking to provide us with true peace of mind. finding the right private health insurance australia is about looking ahead, not just at our current health status.

BEST HEALTH PLANS FOR SINGLES AND YOUNG PROFESSIONALS

for young singles and professionals, the primary goal of their australian health plans is often a mix of basic protection and tax efficiency. we normally look for basic or bronze hospital plans that allow us to step away from the medicare levy surcharge while providing cover for sudden issues like appendicitis. in terms of our extras, we typically find the most value in dental care and physiotherapy, especially if we are lead active, athletic lives. we also see a lot of younger members opting for plans that include lifestyle “extras” such as discounted gym fees or wellness apps, which provide an actual daily benefit from their membership. at this stage, it’s about staying protected while keeping our costs managed and predictable.

this is also the critical time for us to start the “insurance clock” to avoid getting hit by future lifetime health cover (lhc) penalties. by securing our cover before we turn 31, we effectively lock in lower rates for the rest of our lives, which is a major long-term financial win for our future selves. we would encourage every young australian to view their insurance as a long-term investment in their financial future as much as a safeguard for their health. while it might seem like an unnecessary cost when we are young and healthy, the total savings and avoided penalties are massive over several decades. australian health plans for the young are all about building a solid foundation for the years to come.

AFFORDABLE FAMILY COVERAGE: HOSPITAL AND EXTRAS FOR KIDS

as soon as we start a family, our priorities inevitably shift toward comprehensive protection that looks after everyone from the infants to the parents. many australian health plans specifically designed for families offer features like ‘child-only’ extensions or allow children to stay on the policy at no extra cost until they are 21 or even 25. we look for plans with strong coverage for those frequent childhood medical needs, such as dental care or tonsil surgery. for us as parents, having private cover means we have the option of choosing our own obstetricians and a private room, which can make the experience of welcoming a new child much more comfortable. we just have to remember to check those 12-month waiting periods for pregnancy and plan ahead for our private health insurance australia needs.

COMPREHENSIVE SUPPORT FOR SENIORS AND RETIREES

as we move into our retirement years, our medical needs tend to become more frequent and more complex, making a move toward higher-tier australian health plans a very wise decision. at this stage of life, we are often looking for silver or gold tiers that fully cover major joint replacements, heart health, and the management of chronic conditions. we also place a high value on extras that provide substantial rebates for things like hearing aids and high-end dental work like bridges or crowns. many providers now offer specialized seniors’ plans that include home-based rehabilitation services, allowing us to recover in the comfort of our own homes after a hospital stay. these features are absolutely vital for us as we focus on maintaining our independence and our quality of life.

we must also consider the shift in our finances during retirement, where our regular income might drop while our health risks are statistically higher. the government’s private health insurance rebate becomes even more valuable here, as it increases for those of us over the age of 65. we suggest that seniors work very closely with their gp to identify what their most likely future health needs will be, ensuring their australian health plans are ready when the time comes. whether it’s managing cataract surgery or needing fast access to a cardiac surgeon, having the correct level of cover is about protecting the hard-earned freedom of our retirement. our collective wisdom in picking the right insurer allows us all to age with dignity and the best medical support available.

CONCLUSION

to wrap things up, we believe that navigating the world of australian health plans is a strategic exercise in balancing our medical needs, our financial reality, and our personal freedom of choice. we have seen how the public foundation of medicare provides a solid start, while the private sector offers the extra autonomy and speed that so many of us value. from understanding the tiered hospital system to successfully avoiding tax surcharges like the medicare levy surcharge, every bit of knowledge we acquire helps us make smarter decisions for our families. the australian system is a true source of pride for our nation, and by participating in it thoughtfully, we ensure it stays strong for every single person who calls this country home.

we strongly encourage you to take an active role in your own health management by conducting regular reviews of your cover and staying up to date with changes in government rules. the “ideal” plan is always a moving target that will change as your life moves forward, and staying with the same policy for decades can often lead to poor coverage or wasted money. by using modern comparison tools, asking for informed financial consent, and understanding how waiting periods and the gap function, you can turn your insurance from a confusing monthly cost into a powerful asset for your wellness. our journey through the australian medical landscape is a long one, and having the right australian health plans by our side makes the road ahead much more secure. choosing private health insurance australia is a critical part of that security.

finally, we must never lose sight of the fact that the ultimate goal of all these systems is our individual and collective well-being. whether we are receiving care in a large public hospital or a specialized private clinic, the quality of our medical professionals is truly world-class. research from “the lancet” and other eminent journals continues to highlight the high standards of australian medicine and the positive impacts of our hybrid system. by making smart choices about our insurance, we support this standard of excellence and protect our most valuable possession-our health. we hope this guide has given us the clarity and the confidence to master australian health plans and secure a healthy, vibrant future in the lucky country.

Disclaimer: This article is for informational purposes only and does not constitute medical, financial, or legal advice. Always consult with a qualified professional before making decisions about your healthcare or insurance coverage.

references and sources

- The Commonwealth Fund: Mirror, Mirror 2021: Reflecting Poorly

- World Health Organization (WHO): Australia Health Profile

- The Lancet: Measuring Performance on the Healthcare Access and Quality Index

- Australian Taxation Office (ATO): Medicare Levy Surcharge

- PrivateHealth.gov.au: Lifetime Health Cover Loading