HOME AND VEHICLE INSURANCE: INCREDIBLE STRATEGIES TO MASTER YOUR PROTECTION 2026

securing reliable home and vehicle insurance stands out as one of the most brilliant and fundamental strategies for long-term financial stability in the modern united kingdom. recently, we have witnessed uk motor premiums climb rapidly due to inflation and the rising expense of fixing complex driver assistance technologies. navigating this current economic pressure requires us to carefully consider smart financial defenses. merging the protection of our domestic property with our daily transport into a single contract dramatically streamlines our household administration. therefore, we build a formidable barrier against sudden market fluctuations by embracing this integrated method of asset defense.

NOTE:

according to recent data from the association of british insurers, inflation in car parts and labor is a primary driver behind the rising costs of insurance premiums across the united kingdom.

examining these multicover setups shows us exactly how underwriters calculate bundled risk factors. understanding these linked policies helps us safely use our shared household data to secure better terms. securing our assets goes well beyond basic paperwork reduction, acting instead as a major evolution in personal risk assessment. grasping these mechanics gives us a distinct advantage over those who continue juggling separate, unconnected policies. studies highlighted by the national institutes of health suggest that lowering the mental burden of tracking multiple renewals leads to sharper economic choices.

HOW DOES BUNDLING INSURANCE REDUCE THE OVERALL COST?

insurers save on marketing and administrative costs when we buy multiple protections. we benefit because they pass these savings to us to encourage customer loyalty and long-term retention.

throughout this comprehensive guide, we plan to highlight the structural flaws and extended impacts that basic summaries usually miss. identifying issues like algorithmic cross-contamination, independent pricing gaps, and gradual rate creep remains our primary objective here. mapping out this complicated sector step-by-step ensures our protective choices stay remarkably solid, practical, and financially sensible over time.

KEY TAKEAWAYS

- securing combined home and vehicle insurance actively reduces our household administrative friction and cognitive load.

- we must clearly distinguish between genuine multicover agreements and superficial multi-policy promotional discounts.

- hidden rate creep can slowly neutralize our initial bundling discounts over prolonged periods if we fail to monitor renewals.

- algorithmic reassessments at renewal might inadvertently inflate the pricing matrix of our entire combined bundle.

- we should always establish a definitive standalone benchmark price before committing to any consolidated package.

You Might Also Like

1. UNDERSTANDING THE CORE OF COMBINED INSURANCE POLICIES

over the past ten years, the fundamental framework of the industry has undergone a massive transformation. what started as a simple promotional tactic now functions as a highly complex, data-driven financial instrument. industry providers now clearly prioritize total household security rather than hunting for single-policy clients. economic shifts and changing consumer demands naturally forced this broad structural pivot. given the sharp rises in transport coverage costs, we naturally feel compelled to research these combined insurance policies to maximize our domestic economic defenses.

TIPS:

when searching for these products, use terms like “multicover” or “combined policy” to find modern, integrated options that truly sync your renewal dates.

pooling our physical assets together plugs us into a vast system of corporate efficiency. carriers gain huge advantages from this setup since keeping one client across several categories slashes their advertising and onboarding budgets. supplying them with this reliable loyalty generally unlocks better premium rates alongside centralized digital management tools for us. recognizing how this mutual benefit operates gives us the perfect foundation for refining our broad protective strategy.

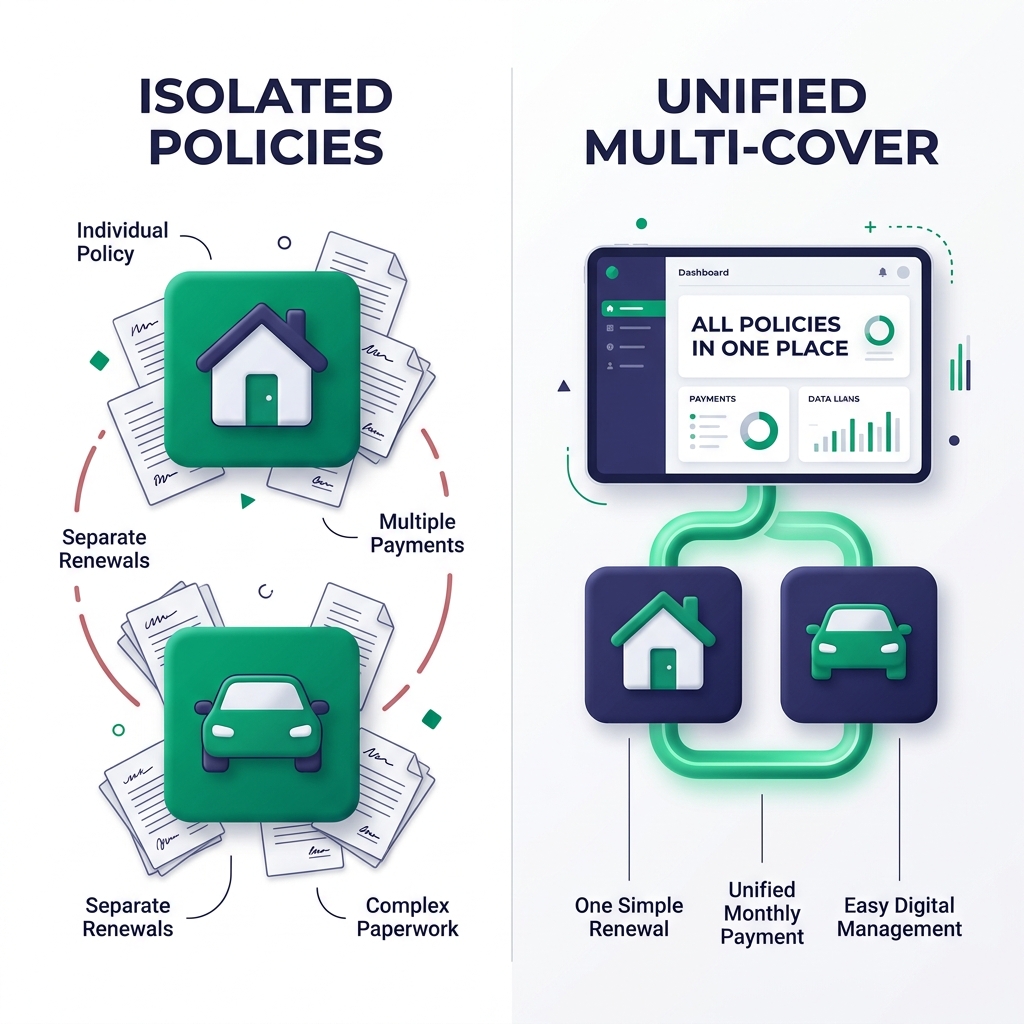

DISSECTING MULTI-COVER POLICIES VS. MULTI-POLICY DISCOUNTS

people often feel overwhelmed by the precise technical terms used to describe these packaged financial services. safely maneuvering through this sector requires us to completely separate a genuine multicover setup from a standard multi-policy discount. treating this difference as a mere technicality is a mistake, because it entirely changes the underlying legal agreement. inside a true multicover system, our various belongings become fully connected under one main profile that operates seamlessly together. achieving this profound level of linkage defines the modern standard for reliable home and vehicle insurance.

REMEMBER:

while convenience is a major factor, our primary goal remains financial optimization and ensuring our coverage remains incredibly comprehensive under all circumstances.

on the other hand, a simple volume discount just trims the final price of completely independent, disconnected agreements bought from the same company. maintaining separate anniversary dates, varying conditions, and divided claims departments remains standard practice with these fragmented deals. sorting through identical mountains of yearly paperwork persists, even if we save a small fraction of money. spotting this core variation helps us easily avoid substandard packages pretending to be fully unified services. aligning everything onto a single renewal deadline instantly cuts down our tedious administrative chores.

THE ALGORITHMIC UNDERWRITING PROCESS EXPLAINED

uncovering the exact methods carriers use to evaluate and charge for grouped liabilities satisfies our need for total transparency. pricing out combined insurance policies today depends heavily on advanced computer models instead of human actuaries. companies instantly pull together our shared background details, financial reliability scores, and detailed neighborhood risk assessments. feeding every piece of data into one central formula allows the provider to build an incredibly precise, overarching snapshot of our family unit.

WARNING:

because these systems are fully automated, any inaccurate data entered during the quote phase can lead to voided coverage or significantly higher premiums during a future claim.

performing a single unified background check severely cuts the processing costs usually tied to creating multiple separate profiles. checking our regional claims background and financial status just one time causes the provider’s internal expenses to drop sharply. capturing a portion of these backend savings becomes possible for us when the company offers its standard package discounts. grasping how this operational machinery functions completely eliminates the confusion surrounding their final rate calculations.

additionally, the software specifically measures the connected probability of loss between our residence and our road routines. keeping a car inside a secure garage while living in a historically safe neighborhood tells the system to multiply our safety scores across both categories at once. applying this intertwined logic explains how high-end grouped packages sometimes deliver massive price drops that individual policies cannot possibly replicate.

2. THE FINANCIAL MECHANICS AND PRIMARY BENEFITS OF BUNDLING

shifting our lens toward deep commercial evaluation helps us find the unshakeable data needed to validate a permanent provider change. rejecting fluffy sales pitches, we elect to concentrate entirely on hard economic metrics and distinct structural advantages instead. dissecting the pure monetary machinery powering home and vehicle insurance grants us the ability to build a mathematically flawless argument for unified profiles. gaining these benefits impacts our lives far beyond simple organizational shortcuts, providing tangible capital preservation.

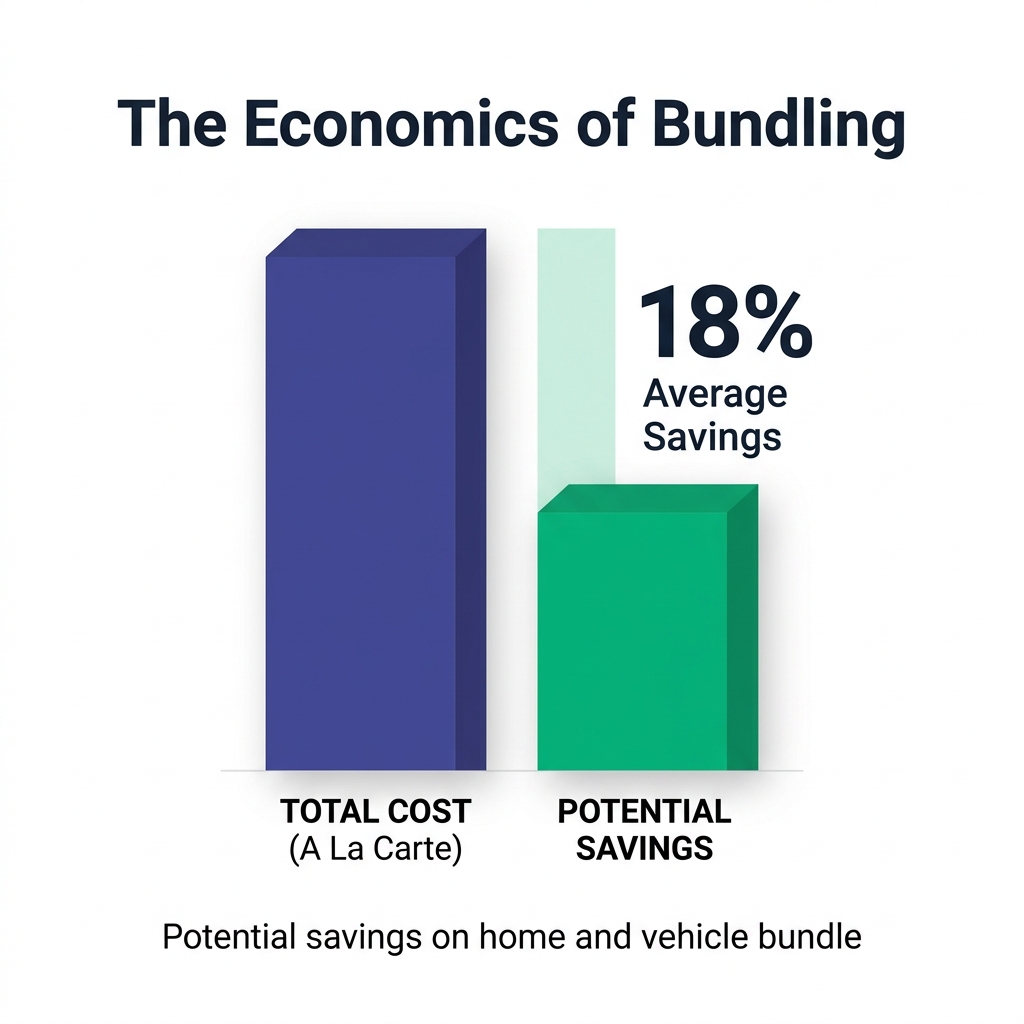

ANALYZING AVERAGE COST REDUCTIONS AND SAVINGS

establishing a grounded expectation of the exact monetary rewards linked to these packages remains crucial. looking closely at current market figures reveals that real multi-line reductions generally sit between sixteen and eighteen percent throughout the united kingdom. nevertheless, a few modern online providers occasionally boast extraordinary yearly savings stretching up to three hundred and eighty-four pounds for their users. stripping away the duplicate processing fees hidden inside separate contracts makes these intense price cuts possible for grouped architectures.

| METRIC | INDUSTRY AVERAGE |

|---|---|

| standard bundle discount | 16% – 18% |

| high-end potential saving | £384 per year |

lockng in these fantastic rates happens purely because of the company’s efficient digital framework and lowered marketing expenses. securing our residential property alongside our daily commuter instantly doubles our long-term profitability in the eyes of the underwriter. offering us a generous initial price drop makes perfect business sense for them under these conditions. taking full advantage of this unique market situation requires us to negotiate fiercely during the initial pricing stage.

placing these financial victories into the context of our current inflationary environment adds vital perspective. dropping a combined bill by eighteen percent basically cancels out the recent market spikes driven by expensive technological vehicle repairs. implementing this exact blueprint does much more than save us a few coins; it effectively shields our total family wealth from unpredictable global economic swings.

THE SHARED EXCESS ADVANTAGE IN CATASTROPHIC CLAIMS

evaluating a highly destructive, albeit uncommon, situation where a single incident harms several belongings at once demands our attention. picturing a massive tree branch smashing through our roof and crushing the car below it, or thieves taking our laptops alongside our vehicle keys, highlights this threat perfectly. holding split policies during such a disaster legally forces us to cover two distinct deductibles, which creates a massive, instantaneous drain on our liquid cash reserves.

TIPS:

check your policy wording for a “single excess” clause. this ensures that in a disaster affecting both home and car, we only pay one deductible total.

high-tier home and vehicle insurance directly eliminates this specific danger by introducing a shared deductible clause. facing a severe event that wrecks our house and transport at the same time means we only ever owe the single highest excess amount instead of both combined. limiting our sudden cash layout through this architectural feature provides immense relief during chaotic, highly emotional emergency situations.

utilizing a unified excess clause offers a monumental, frequently ignored benefit within authentic merged frameworks. forging this kind of heavy financial shield proves virtually impossible when dealing with entirely separate underwriters. preparing meticulously for these severe edge cases pushes our personal safety plan past simple legal requirements and into the realm of expert asset preservation.

INDEPENDENT PROTECTION OF NO CLAIMS DISCOUNTS

tackling the widespread worry regarding cross-contamination means we need to explain exactly how merged agreements treat our past records. quite a few people mistakenly believe that causing a traffic accident instantly destroys the long-standing bonus earned on their residential building. finding peace of mind is easy when we realize that premium combined insurance policies maintain a strict wall between these separate behavioral metrics. underwriters actively process these belongings as completely isolated risk groups throughout the duration of the active term.

REMEMBER:

our car ncd and home ncd remain beautifully separate. a claim on one does not automatically cancel out the massive discount on the other within the same year.

experiencing a tiny fender bender might cause our specific transportation rates to fluctuate slightly, yet our building’s reward status stays perfectly intact. operating with this invisible barrier preserves our primary structural discounts while we continue enjoying the sheer convenience of a synchronized dashboard. maintaining the precise individualized safety features we normally associate with isolated, niche agreements remains totally possible here.

comprehending this strict separation actively stops us from acting out of blind panic or misinformation. linking a very expensive primary residence to our everyday driving machine no longer threatens to collapse our entire financial setup over one careless parking mistake. preserving tight authority over our personal safety histories happens effortlessly while we continuously gather the macro-level economic benefits of packaging.

3. ADMINISTRATIVE EFFICIENCIES AND POLICY LOGISTICS

exploring this segment proves highly valuable for those of us wanting to immediately cut down on frustrating paperwork. running a contemporary family brings enough chaos, and juggling scattered financial documents only makes our daily routines harder. recent technological leaps within the sphere of domestic protection provide a direct cure for this mounting organizational exhaustion. diving into the mechanics of these connected digital tools reveals exactly how they streamline our tedious yearly chores.

SYNCHRONIZING ASYNCHRONOUS RENEWAL DATES

hitting a major scheduling roadblock happens constantly when we try to upgrade, simply because our house and car coverage usually end months apart. dealing with these mismatched timelines frequently discourages us from ever attempting to unify our accounts. luckily, top-tier carriers have designed brilliant solutions that allow for a perfectly staggered integration process. starting the primary agreement using whichever item expires first allows us to legally lock in the remaining items for a delayed merger.

WHAT IF MY POLICIES ARE SIX MONTHS APART?

we can set up the master account now and schedule the second policy to join automatically on its expiry date, ensuring absolutely no double-payment.

advanced internal algorithms smoothly compute the necessary prorated charges to slowly pull every item toward one shared yearly anniversary. reaching its natural end date allows the secondary asset to drop effortlessly into our existing home and vehicle insurance network. dodging those painful early exit penalties from older companies becomes simple while we still guarantee our long-term bundled pricing. initiating this phased entry demands hardly any physical effort from us after we provide the initial green light.

UNIFIED ACCOUNT MANAGEMENT AND TECHNOLOGICAL INTEGRATION

pointing out the radical technological upgrades across the wider financial industry remains highly necessary. massive institutions currently rely on exceptional cloud systems that parse staggering volumes of customer habits without a single glitch. achieving this specific technical milestone allows providers to construct perfectly integrated dashboards for our combined insurance policies. keeping tabs on overall family payments, monitoring ongoing claims, and pulling up legal texts now requires just one primary user tapping a single mobile app.

giving us the power to hand out specific access rights makes these modern platforms even more impressive. letting the main account owner handle the big financial decisions works perfectly while younger relatives use distinct passwords to watch over their own cars. building this detailed level of access protects the personal privacy of novice drivers without forcing us to surrender our essential budgetary control.

walking away from scattered paper folders and messy, disconnected login screens dramatically lowers our daily mental strain. locating an id number, double-checking our exact limits, or triggering an urgent rescue request turns into one lightning-fast action. enjoying this flawless digital harmony beautifully supports the raw monetary savings generated by the underlying package.

4. THE STRUCTURAL DISADVANTAGES AND HIDDEN RISKS OF BUNDLING

ensuring our analysis stands as the most reliable resource in the world means we have to rigorously expose the built-in flaws of these packages. maintaining total neutrality acts as a strict prerequisite whenever we explore convoluted economic networks. swallowing corporate advertising without questioning the submerged dangers leaves our savings completely exposed to steady, long-term depletion. pulling apart the major loopholes that casual observers purposely skip will protect our wealth moving forward.

WARNING:

complacency remains our absolute biggest risk. we must not allow the ease of management to stop us from vigorously price-checking our renewal quotes every single year.

noticing these architectural downsides usually takes a few years because they develop so quietly. staying intensely alert to independent pricing gaps, stubborn premium inflation, and the hidden blending of our safety profiles is an absolute must. completely understanding these warning signs guarantees our use of home and vehicle insurance stays undeniably beneficial to our bottom line.

THE STANDALONE PRICE DISCREPANCY PHENOMENON

investigating the deceptive nature of percentage reductions requires a highly critical, mathematical eye. knocking eighteen percent off a terribly overpriced starting figure still leaves us paying more than if we just bought a sharply priced individual contract. carriers continuously push the ease of multicover products, praying we overlook the artificially high starting point. spotting this specific baseline pricing illusion remains our best defense against the most common snare in the modern sector.

TIPS:

always calculate the total annual cost. a twenty percent discount on a one thousand pound policy is still significantly more expensive than a seven hundred pound standalone policy with zero discount.

hunting down two separate contracts from highly focused, independent underwriters often decisively beats the end cost of a unified deal. pairing a boutique car coverage firm with a small local property entity sometimes produces a total bill much lighter than a giant corporation’s flashy promotion. demanding strict attention to this distinct mathematical reality protects us from lazy, overly trusting financial habits. executing a ruthless comparison between the unified quote and the absolute cheapest pair of separate contracts ensures we never overpay.

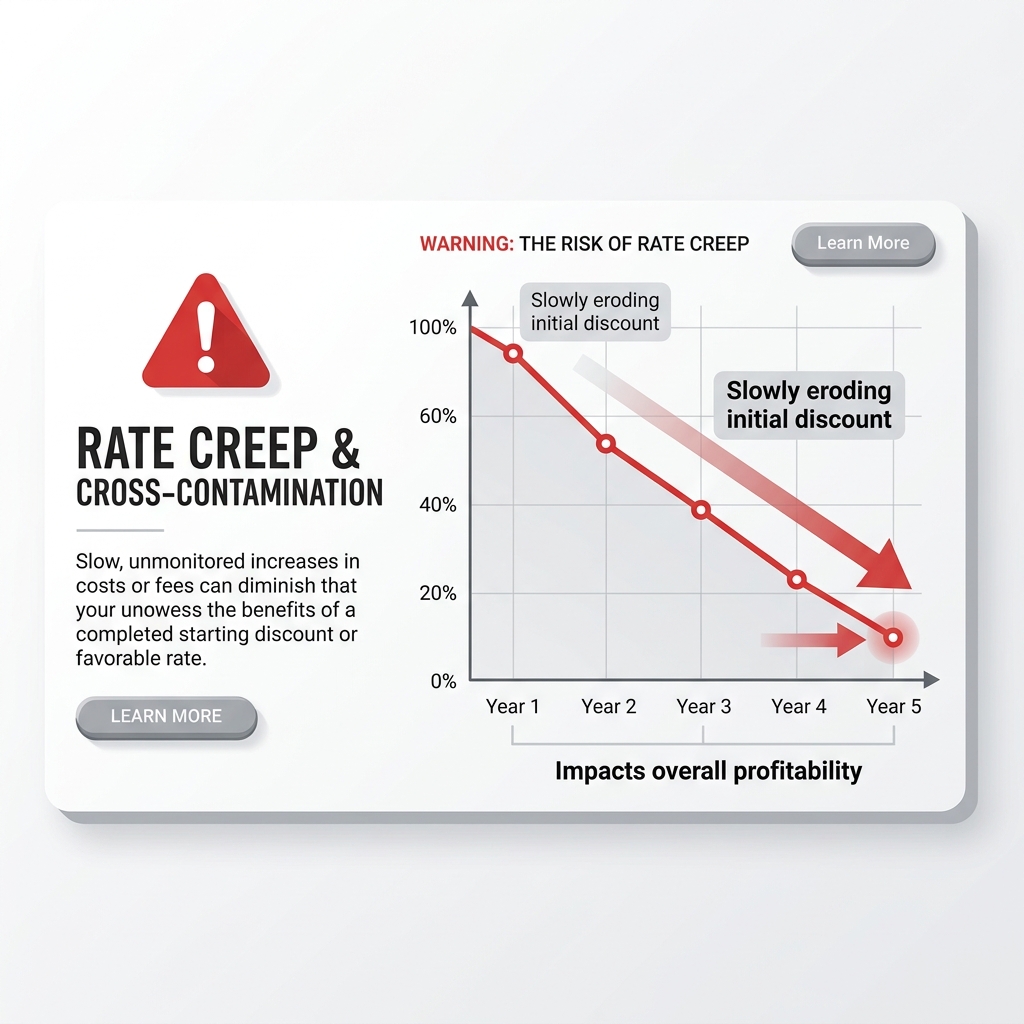

RATE CREEP AND THE EROSION OF LOYALTY DISCOUNTS

diving into the psychological tactics deployed by giant financial institutions reveals exactly how they extract our wealth. utilizing a slow, deliberate tactic known as rate creep allows providers to systematically increase their profits year after year. betting correctly that we will refuse to unpick a complicated setup due to sheer laziness fuels this corporate strategy. dreading the annoying paperwork required to separate our belongings mathematically forces us to accept tiny, regular billing increases without a fight.

pushing the underlying rates up slightly across three to five years successfully deletes the original advantage we secured during sign-up. cheering for a massive twenty percent reduction during our first twelve months usually ends in disappointment when that discount vanishes by the fourth cycle. squeezing passive families through this quiet margin growth pulls massive long-term profits without ever improving the actual service provided.

fighting back against this deliberate financial decay means we should view our merged contracts as strictly short-term tools. handing endless loyalty to a corporation just because their mobile app functions smoothly contradicts our core wealth-building principles. testing our renewal quote against fresh market data annually allows us to ruthlessly drop any provider trying to tax our desire for a quiet life.

CROSS-CONTAMINATION OF RISK PROFILES AT RENEWAL

although standard protective bonuses remain legally shielded during a live contract, we need to expose a sneaky software adjustment that happens at renewal time. recalculating our total family risk based on how often we call for help represents standard operating procedure for modern carriers. reporting several tiny issues around the house, like a cracked window or a small pipe leak, immediately trains the macro-algorithm to label us as a highly demanding client.

NOTE:

this holistic risk assessment means that multiple small events in our home can indirectly influence the perceived overall risk of our driving behavior when the algorithm recalculates at renewal.

registering too many small incidents forces the computer to quietly upgrade our overarching probability of causing future financial losses. reaching the yearly expiration for our home and vehicle insurance under these conditions often results in a vastly inflated total price tag. protecting a flawless driving history suddenly becomes impossible because our house triggered too many red flags within the master processing unit. neutralizing this unseen threat requires us to pay out of pocket for tiny repairs.

THE CASH-FLOW BURDEN OF THE UNIFIED ANNUAL PREMIUM

highlighting a very realistic, though seldom mentioned, economic hurdle brings us to the issue of immense cash-flow bottlenecks. successfully syncing our anniversaries accidentally produces one absolutely staggering yearly invoice. separating these massive payments in the past—perhaps clearing transport in spring and the house in autumn—gave our bank accounts plenty of breathing room throughout the year.

SHOULD I PAY MONTHLY FOR MY BUNDLED POLICY?

we strongly recommend paying annually if possible. monthly installments often carry massive interest rates that can entirely cancel out your initial bundling discount.

facing this massive, consolidated charge all at once frequently pushes surprised families into accepting the provider’s monthly payment schemes. sadly, choosing these staggered installment options almost always triggers harsh interest penalties and aggressive financing taxes that easily top twelve percent. bleeding cash through these secondary lending fees instantly destroys the exact multi-policy reductions we worked tirelessly to obtain. building up enough liquid cash before we trigger a merged strategy acts as our primary defense mechanism here.

5. NAVIGATING REGULATORY ENVIRONMENTS AND MACROECONOMIC PRESSURES

transitioning our guide from simple tips into professional-grade market forecasting requires a shift in perspective. grasping the vast economic currents and governmental structures that control product creation gives us a massive edge. political rulings completely dominate how corporations calculate the cost of our combined insurance policies in the modern era. monitoring these sweeping legislative changes rigorously ensures our domestic plans align perfectly with established legal boundaries.

THE IMPACT OF THE FINANCIAL CONDUCT AUTHORITY PRICING RULES

breaking down the monumental market shockwave initiated by the financial conduct authority and their early twenty twenty-two pricing rules is absolutely essential. forcing this massive legal framework onto the sector permanently changed the way retail protections are valued across the united kingdom. stopping companies from slapping a loyal, returning client with a heavier base rate than a brand-new user with identical risks sits at the core of this legislation.

implementing this aggressive intervention aimed to crush the exploitative billing tactics that historically plagued the public. applying these guidelines to home and vehicle insurance suggests our yearly quotes should stay inherently fair without us constantly jumping between carriers. realizing the truth requires digging deeper, as corporations simply moved their profit-seeking behaviors over to hidden service charges and vastly smaller welcome bonuses to circumvent the absolute letter of the law.

internalizing these strict legal commands gives us immense power whenever we speak to customer service agents. watching our merged renewal cost jump without warning allows us to confidently demand evidence that they are strictly following the newest equality protocols. swinging this exact knowledge like a heavy club helps us effortlessly smash through unfair, unexplainable pricing escalations.

THE ERADICATION OF THE LOYALTY PENALTY AND CROSS-SUBSIDIZATION

expanding on these governmental boundaries requires us to plainly outline the old system of financial cross-subsidization. resting on their laurels for years meant loyal clients accidentally paid for the incredibly cheap, money-losing introductory rates handed to constant switchers. burning cash to grab fresh signatures forced carriers to relentlessly overcharge the quiet families who never bothered checking the broader market.

pointing out that the state successfully killed the loyalty penalty also means we must accept the death of unbelievably cheap welcome offers. consumers who jump ship every twelve months currently face a flattened landscape where heavily subsidized deals barely exist anymore. lifting the absolute bottom price threshold completely transformed the baseline economics for everybody involved in the domestic protection market.

watching the market normalize proves that authentic multi-line reductions are now among the very few legitimate ways to slash our bills safely. pulling savings directly from actual backend processing efficiencies, instead of fake promotional budgets, allows these packages to thrive under intense government watch. surviving this harsh legal climate proves exactly why structural grouping remains superior to chasing dead loss-leader promotions.

SOLVENCY II AND MARKET DATA TRANSPARENCY

solidifying our deep technical knowledge means understanding how massive guidelines like solvency ii control the fundamental health of the business. policing these heavy capital rules falls to the prudential regulation authority, effectively guaranteeing that british carriers hold gigantic piles of usable cash. forcing this intense level of financial readiness empowers massive corporations to build and sell highly complicated, deeply intertwined pricing algorithms.

WARNING:

always ensure your chosen underwriter is strictly authorized by the pra and heavily regulated by the fca to guarantee your ultimate financial protection in case of a catastrophic market failure.

operating without this brutal data clarity and deep cash padding would prevent any single company from safely absorbing a family’s entire risk profile at once. creating a viable home and vehicle insurance product depends entirely on these unseen, aggressive political rules keeping the economic scales perfectly balanced against systemic collapse. leaning on this precise data allows us to completely trust the financial backbone of our selected underwriters.

6. CONSUMER DEMOGRAPHICS: IDENTIFYING THE IDEAL BUNDLING CANDIDATE

shifting our focus toward helping our community accurately judge their own compatibility with this setup comes next. realizing that not every living situation gains the exact same advantages from deep grouping prevents costly errors. marching toward a final purchase means we must ruthlessly analyze our own structural needs at home. pinpointing the precise type of family unit that extracts the absolute most wealth from combined insurance policies remains our ultimate goal here.

MULTI-VEHICLE HOUSEHOLDS AND EXTENDED FAMILIES

identifying that integrated packages work miracles for highly complicated, multi-generational homes is remarkably easy. elite-level contracts routinely allow us to list six or seven distinct cars onto one massive, overarching file. pulling the main breadwinners, risky teenage learners, and cheap weekend runabouts into a single, aggressively reduced pricing bubble changes the entire financial game.

additionally, these high-end frameworks easily stretch to protect cars parked at short-term locations, like college dormitories for older teenagers. trying to juggle four completely different auto contracts while keeping the main house protected quickly turns into an administrative nightmare. forcing all of these elements into a dedicated home and vehicle insurance application deletes countless hours of frustrating desk work every single year.

layering multiple car reductions directly on top of the base property savings works perfectly for these crowded family environments. calculating the final tally for a massive four-car estate wrapped together proves that this strategy utterly destroys any loose combination of fragmented retail contracts floating around the open market.

ASSESSING SUITABILITY FOR NON-STANDARD RISKS

broadcasting an intense, immediate caution to incredibly wealthy individuals or those with highly unusual belongings is deeply necessary. recognizing that basic integrated systems depend completely on stiff, mass-market formulas designed for sheer speed keeps us grounded. processing normal family cars and standard brick houses is their specialty, but they crumble instantly when confronted with highly exotic, unquantifiable risk factors.

consequently, needing protection for historically protected grade ii listed buildings, cliffside houses, or radically tuned hypercars means we should completely avoid basic consumer packages. shoving a bizarre, unique asset into a rigidly coded computer sequence results in either instant denial or ridiculously high billing attempts that insult our intelligence.

facing these extreme scenarios means we highly recommend dropping the hunt for standard retail combinations altogether. pivoting sharply toward custom-built agreements assembled by niche, independent experts or private wealth managers ensures our exotic risks are handled with human intelligence and bespoke calculations instead of raw, unforgiving code.

INTEGRATING UMBRELLA LIABILITY AND ADDITIONAL ASSET CLASSES

pushing our defensive boundaries well past the standard house and car setup remains an ongoing mission for us. utilizing contemporary master accounts grants us astonishing room to add on vital secondary products. blending these extra layers of security into our core setup widens the protective moat around our life savings, all while keeping the paperwork firmly locked inside a single digital vault.

bringing personal umbrella liability into the conversation highlights an absolutely vital, yet constantly overlooked, piece of our defensive wall. designing this overarching safety net ensures it triggers exactly when the basic caps of our primary coverage tap out during a massive, legally problematic disaster. acting as our supreme emergency brake, it actively protects us from utterly ruinous lawsuits brought by injured third parties.

triggering a brutal multi-car crash that leaves multiple people severely hurt can instantly burn through standard automotive payout limits. lacking that secondary safety net leaves our physical houses and retirement funds totally exposed to rapid confiscation by angry legal teams. locking this broad shield into our home and vehicle insurance package represents an absolute requirement if we actually care about long-term wealth survival.

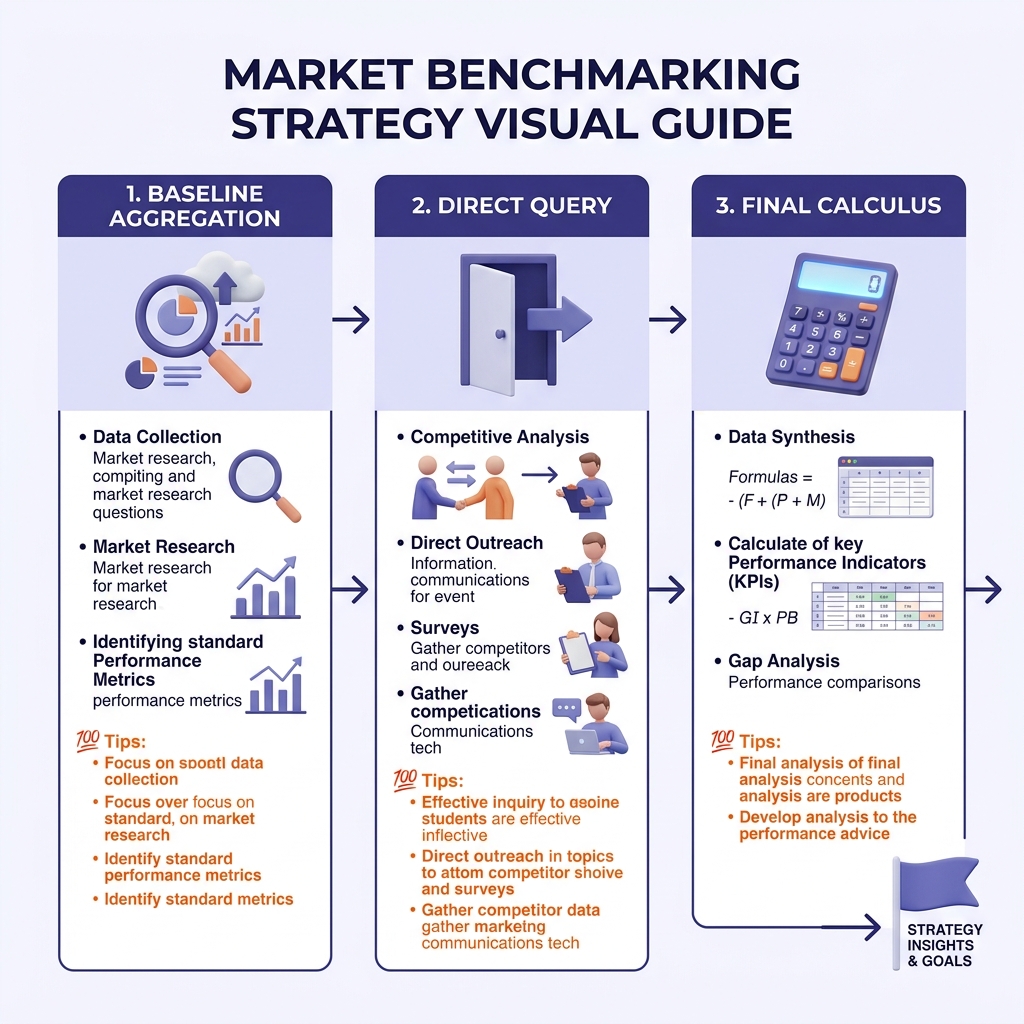

7. THE DEFINITIVE MARKET BENCHMARKING STRATEGY AND IMPLEMENTATION

transforming our deep theoretical research into a sharp, instantly usable battle plan happens right now. following this specific sequence guarantees we walk away with the absolute finest economic result possible. rejecting blind luck entirely, we prefer to launch a highly organized, layered attack against the retail market to secure our family’s future.

STEP 1: ESTABLISHING THE STANDALONE BASELINE VIA AGGREGATORS

advising our readers to start their search entirely disconnected from the main corporate providers sits at the very heart of our strategy. launching our initial probe means we lean heavily on unbiased comparison engines to find the cheapest isolated rates for our living space and our cars. performing this essential drill locks in a pristine, mathematically sound baseline cost.

REMEMBER:

the “benchmark price” is the strictly calculated total cost of the two absolutely cheapest separate policies you can find. this is the sacred figure the bundle must conclusively beat.

raking through the open sector aggressively allows us to spot the absolute lowest price possible for living a disconnected life. treating this fragmented total as our unshakeable reference point is vital. lacking this basic intelligence leaves us wandering in the dark, wholly unable to properly judge if a pitched combined insurance policies package actually holds any genuine monetary value.

STEP 2: ENGAGING DIRECT MULTI-COVER PROVIDERS

acknowledging a very deliberate oddity in today’s landscape is crucial: some of the richest, most competitive package designers absolutely refuse to list their goods on standard comparison boards. grabbing those premium, combined offers means we have to walk right up to their digital front doors entirely on our own volition.

clicking directly into their private systems, we carefully type out our vast array of personal facts, making sure the numbers match perfectly with our earlier aggregator searches. pushing their internal software to spit out a deeply tailored, comprehensive rate gives us the localized data we desperately need to make an informed choice.

investing this sweat equity is completely non-negotiable. trusting only broad comparison engines guarantees we overlook the secret formulas massive companies use specifically to destroy fragmented retail pricing. dragging the direct market into a fierce bidding war over our combined assets is the only guaranteed way to win.

STEP 3: THE FINAL COST-BENEFIT CALCULUS

finishing our strategic assault demands a chillingly logical, math-based review. stacking the private, unified offer directly against our highly refined, unbundled baseline price is all that matters now. letting the raw numbers dictate our ultimate move completely removes dangerous human emotion and brand loyalty from the final equation.

pulling the trigger on the home and vehicle insurance deal happens only if the total sum decisively beats our separated reference point. however, if the combined setup costs just a tiny bit more—maybe a handful of pounds a year—we have to coldly evaluate whether gaining a sleek digital interface and dodging hours of paperwork is truly worth the minor financial premium.

EXECUTING THE SWITCH AND AVOIDING COVERAGE GAPS

managing our exit mechanics carefully guarantees we stay on the right side of the law. syncing the absolute start time of our fresh package directly to the very minute our old papers die requires extreme, undivided focus. nailing this surgical crossover provides constant, unbroken shielding for our highly exposed physical investments.

breaking an old agreement right in the middle of its life cycle is generally a terrible idea, unless the raw savings from the fresh package utterly crush the painful exit taxes applied by the old firm. leaning on the delayed integration tools usually works best for us, letting our belongings slide peacefully into the main profile as their natural clocks run out.

CONCLUSION

lockng down dependable, hyper-optimized domestic protection demands way more effort than simply clicking the first cheap banner ad we see on the internet. diving deep into this highly technical topic proved that the real magic of packaging comes from mastering the computer’s logic, grasping the legal walls between our various risks, and exploiting the sheer speed of a globally connected digital dashboard. pushing back violently against rising living costs happens exclusively when we insist on intelligently built, fiercely debated unified setups that actively guard our family’s hard-earned wealth.

still, promising ourselves total market awareness means we have to stay constantly paranoid about invisible industry snares. refusing to get caught by baseline pricing illusions or the quiet, steady bleeding of normalized rate hikes remains our top operational priority. forcing our package deals to constantly fight against highly optimized, independent retail numbers ensures our long-term economic plans stay totally bulletproof and mathematically flawless for decades to come.

in the end, pulling off a perfect shift toward a grouped contract effortlessly cleans up our daily routines while throwing a massive iron wall around our most treasured physical goods. sticking closely to the layered blueprints, regulatory analyses, and legislative secrets mapped out in this document lets us completely dominate the british financial sector, securing a profound level of financial peace that simply cannot be matched by fragmented, outdated planning.