Auto Home Insurance Quotes: 7 Proven Secrets to Beat Rising Premiums

meta description post excerpt: securing competitive auto home insurance quotes is the most effective strategy to shield your household budget from skyrocketing premiums and unexpected market volatility in 2026. facing a staggering 63.8% surge in motoring costs, we must recognize that securing combined auto home insurance quotes acts as a crucial financial buffer for our households. observing the current volatile economic climate, our approach to asset protection has dramatically shifted. tracking down reliable auto home insurance quotes early in the renewal cycle represents a vital strategy for resilience, rather than just a simple convenience. keeping household budgets afloat is increasingly difficult as inflation applies constant pressure across all sectors. evaluating joint policies, as our findings suggest, frequently uncovers unexpected advantages extending well beyond basic premium reductions. striking the perfect balance demands that we carefully evaluate multiple shifting market dynamics.

WHY SHOULD WE CONSIDER BUNDLING INSURANCE POLICIES?

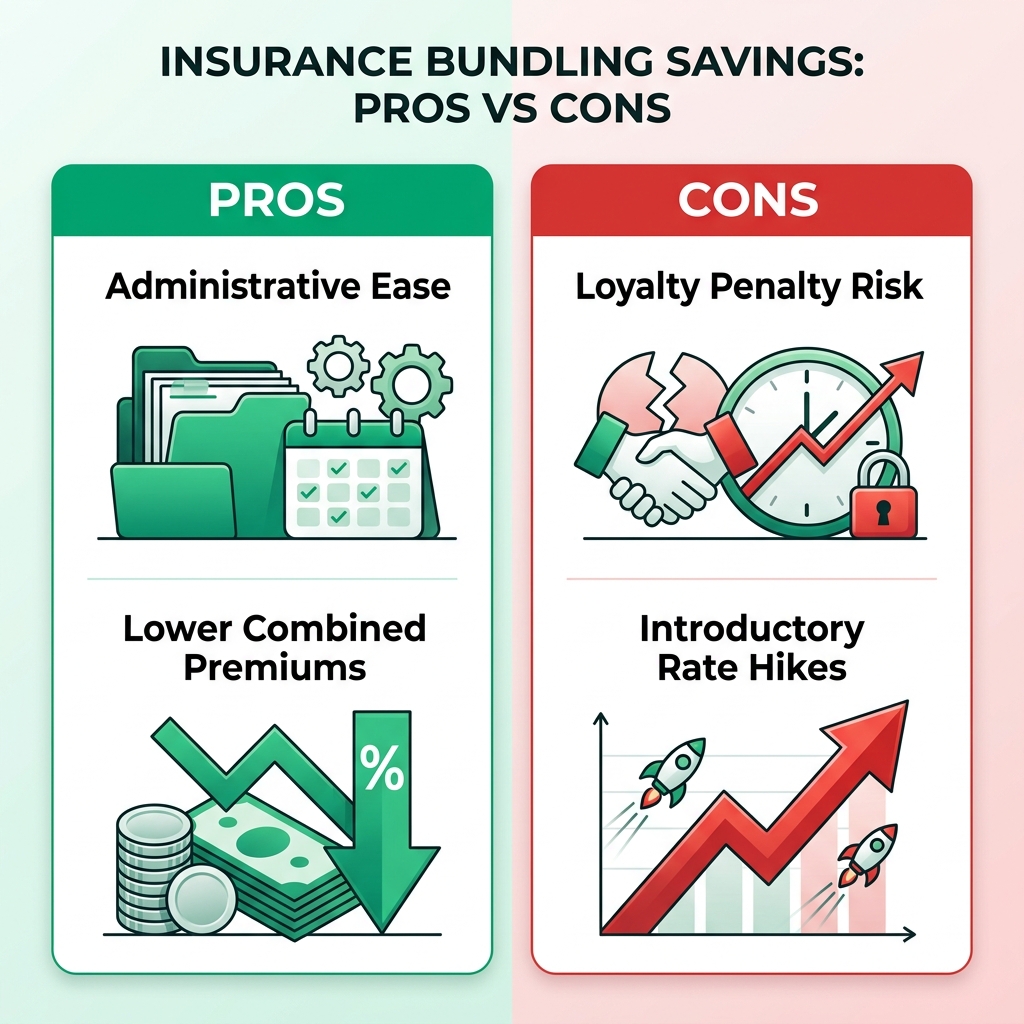

grabbing a bundle usually grants us access to a robust multi policy discount that simply does not exist in the standalone market. streamlining our finances becomes much easier when we rely on a single renewal date and one primary contact point.

rather than taking a passive stance, we need a strategic method to navigate the complex ecosystem of modern coverage providers. feeling overwhelmed by the sheer volume of available options is something we completely understand. contrasting auto home insurance quotes side-by-side exposes just how differently major underwriters calculate our personal risk. a recent report from the “office for national statistics” clearly outlines the escalating financial strain associated with carrying standalone policies. grasping the hidden mechanisms behind these bundles puts us in a much stronger position to make sound, informed choices. diving into the structural nuances of today’s protection landscape will help us build a better defense.

TIPS FOR COMPARISON:

keeping a copy of our current policy schedule close at hand while requesting new rates ensures we always compare identical coverage levels.

technological advancements and economic shifts prove that the coverage landscape is anything but static. looking into joint options gives us a distinct perspective on our broader financial well-being. gathering thorough auto home insurance quotes empowers us to merge our defensive strategies, guarding against sudden liabilities. mastering the structural foundations of these agreements is the first real step we take toward securing optimal household protection.

REMEMBER:

hunting for the cheapest option does not always yield the best result, so we must confirm the limit of indemnity fully covers our total asset value.

KEY TAKEAWAYS

- comparing auto home insurance quotes mitigates the impact of recent premium inflation.

- bundled packages offer significant administrative consolidation and simplified renewals.

- understanding the difference between multicover and a standard multi policy discount is crucial.

- loyalty does not always guarantee the lowest rates in the current economic climate.

- specialist risks often require standalone policies despite the appeal of unified packages.

You Might Also Like

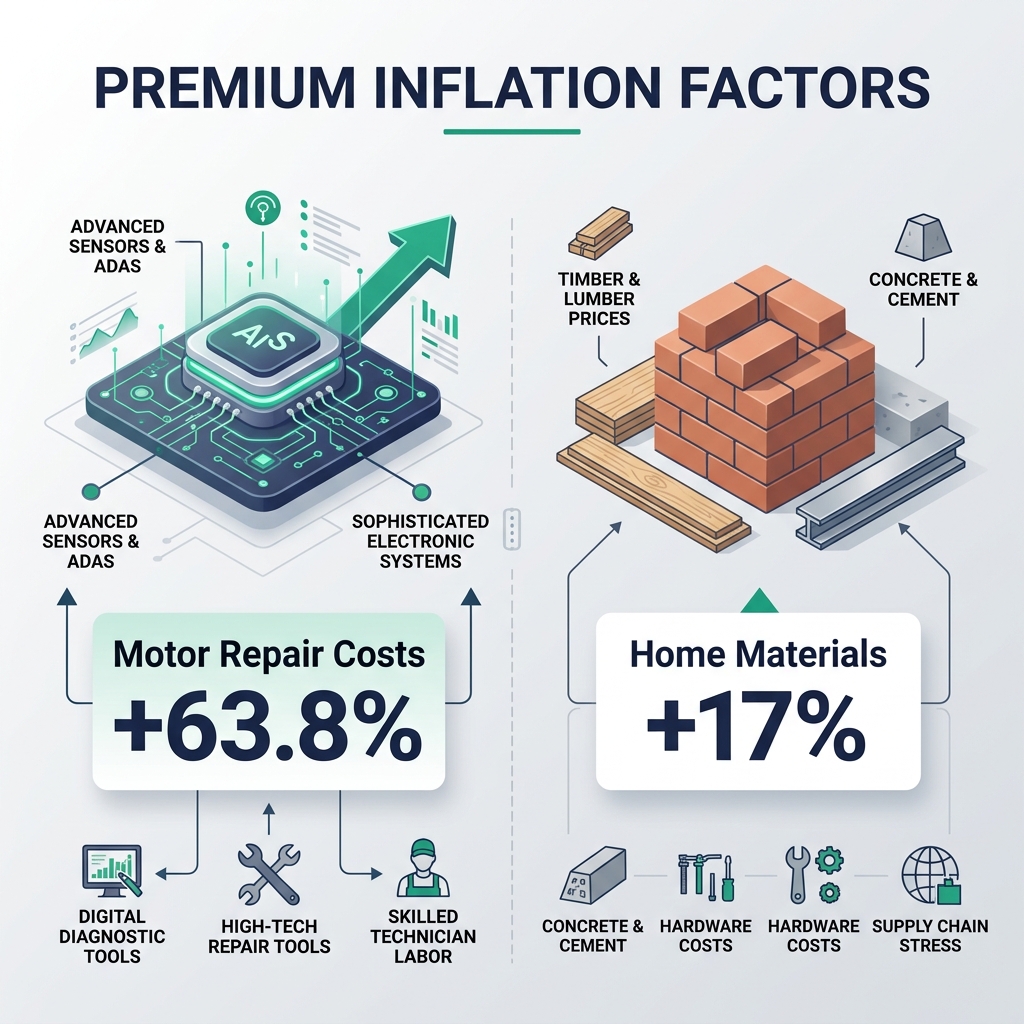

1. THE MACRO-ECONOMIC STATE OF UK INSURANCE (2025-2026): A CRISIS OF PREMIUM INFLATION

evaluating auto home insurance quotes for our daily requirements has fundamentally changed due to the current financial climate. confronting unprecedented challenges, we have watched motoring coverage costs rocket upward by a staggering 63.8 percent recently. household liquidity is feeling the squeeze as home protection premiums have simultaneously jumped by 17 percent. tracing these trends back to their source, we see that global supply chain disruptions heavily fuel this ongoing pricing crisis. external market pressures like these directly dictate the final numbers we see on our auto home insurance quotes.

WARNING:

neglecting to revise our home rebuild cost during times of steep inflation creates a risk of underinsurance, potentially leaving us personally responsible for any massive shortfall.

actuaries and underwriters now grapple with a bizarre paradox caused by advanced driver assistance systems in their risk matrices. preventing minor fender benders is great, yet replacing those delicate technological sensors massively inflates the payout for actual collisions. construction sectors are battling identical inflationary pressures, watching material expenses skyrocket endlessly over the last twelve months. requesting auto home insurance quotes today means we are essentially footing the bill for compounded inflation across both property restoration and automotive repair. mapping out this macroeconomic reality helps us manage our household financial expectations much more effectively.

HOW DOES GEOGRAPHY AFFECT OUR INSURANCE QUOTES?

assessing local crime statistics and environmental risks like flooding requires insurers to rely heavily on postcode rating models. higher vehicle density in urban zones predictably leads to steeper premiums for those of us living in cities.

major financial institutions complicate their pricing models even further by factoring in vast regional variations across the country. baseline tariffs in urban centers are significantly steeper, driven mostly by dense vehicle populations and elevated property crime rates. breaking down these geographical differences allows us to grasp the specific localized factors driving up our personalized risk assessments. we have to supply incredibly precise location details when generating auto home insurance quotes if we want a true reflection of our neighborhood’s risk.

inflationary pressures are projected to persist throughout the rest of the decade, according to a recent report from the “bank of england”. protecting our physical assets against these harsh economic headwinds requires us to adopt a strictly long-term perspective. securing unified agreements right now allows us to lock in favorable rates and shield ourselves from inevitable future premium hikes. pinning down fixed-rate auto home insurance quotes acts as a vital anchor while we navigate an incredibly turbulent financial sea.

You Might Also Like

2. DEFINING THE STRATEGIC BUNDLE: MULTICOVER VS MULTI POLICY DISCOUNT OPTIONS

reviewing our auto home insurance quotes carefully means we must distinguish between unified legal contracts and simple independent discounted policies. legally binding our vehicle and our property together under one single master document is the core function of a multicover agreement. consolidating everything definitely cuts down on paperwork, but it tightly weaves our risk profile across entirely different asset classes. maintaining separate legal boundaries while still granting a lucrative multi policy discount is the primary benefit of utilizing independent setups. analyzing both of these structures side-by-side gives us a much clearer understanding of their true long-term value.

NOTE:

preventing us from being misled about actual savings is why the financial conduct authority strictly regulates how companies present these specific discounts.

processing claims and managing renewals changes drastically depending on the structural differences between these two distinct approaches. our entire annual financial commitment is dictated by a single renewal date whenever we select a unified multicover route. staggered renewal dates from independent policies, conversely, can really help us manage our monthly household cash flow. consumers are strongly advised by the financial conduct authority to review all terms meticulously prior to locking into any specific framework. pulling comparative auto home insurance quotes for both methodologies is undoubtedly the most effective strategy we can deploy.

TIPS:

verifying if a bundle features a common renewal date is essential because it drastically lowers the administrative tracking we face annually.

critical coverage details are frequently overshadowed by the sheer appeal of administrative convenience during our decision-making process. sacrificing essential protections for the sake of simplicity is a trap we avoid by heavily scrutinizing the fine print. a uniform excess policy buried inside a unified contract might completely clash with our personal risk appetite. picking apart distinct auto home insurance quotes allows us to uncover dangerous coverage gaps hiding within seemingly perfect bundled packages.

blending the best elements of both structural frameworks, new hybrid solutions are rapidly emerging on the market. keeping the actual legal underwriting strictly separated while offering a shared administrative dashboard is the genius of these innovative products. engaging with major financial institutions provides the perfect opportunity for our households to ask about these highly flexible options. gathering a diverse range of auto home insurance quotes ultimately empowers us to construct a portfolio perfectly aligned with our administrative habits.

3. ADMIRAL MULTICOVER: AUTO HOME INSURANCE QUOTES AND ADMINISTRATIVE CONSOLIDATION

offering highly structured multicover options has allowed admiral to historically dominate the landscape of administrative consolidation. categorizing their offerings into standard, gold, and platinum levels reveals a fascinating, tiered protection model. scaling our coverage based on strict asset valuations and specific risk tolerance becomes possible through this unique hierarchical system. baseline pricing is instantly influenced by this tier system whenever we pull auto home insurance quotes from this particular underwriter. deciphering how these specific tiers operate guarantees that we never overpay for flashy, unnecessary features.

WHAT HAPPENS TO MY NO-CLAIMS BONUS IN A MULTICOVER POLICY?

submitting a claim against our home protection generally will not impact the no-claims bonus on our motor coverage, seeing as they operate as segregated policy sections.

overcoming a primary hurdle in policy consolidation was finally achieved through the introduction of specialized transition mechanisms. merging our property and vehicle coverage often turns into a massive struggle due to totally misaligned renewal dates. aligning varying timelines without triggering aggressive cancellation fees from our old providers is a huge advantage of this feature. targeting auto home insurance quotes that boast these alignment tools can reward us with incredible, long-term administrative relief.

high-net-worth households demanding incredibly robust protection will find extensive, tailored benefits when evaluating the top premium tiers. enhanced emergency assistance and comprehensive legal cover frequently come baked in as standard features at this elite level. assessing whether these luxurious additions actually justify the heavily elevated premium is a necessary step for our specific financial circumstances. weighing these elite tier packages directly against standard auto home insurance quotes remains a vital exercise in basic economic prudence.

You Might Also Like

4. LV= MULTI COVER: SIMPLICITY AND THE PRICE GUARANTEE ADVANTAGE

diving into the specific packages from lv= highlights a refreshing emphasis on absolute simplicity and transparent pricing logic. expanding our policy later in the annual cycle becomes much less stressful thanks to their unique price guarantee mechanism for additional vehicles. locking in our baseline pricing parameters effectively shields us from creeping mid-term inflation during the contract year. securing auto home insurance quotes that respect these solid guarantees offers us tremendous peace of mind within a highly volatile market.

REMEMBER:

checking if vandalism protection exists within our motor section is vital; it frequently preserves our no-claims bonus if the vehicle suffers damage while parked in our driveway.

a highly consumer-centric approach becomes obvious when we analyze specific bundle promises like dedicated vandalism and misfuelling protections. standard policies frequently exclude misfuelling incidents, even though we know they cause absolutely catastrophic, expensive engine damage. weaving these specific perils explicitly into a multicover package drastically boosts the intrinsic financial value of the entire offering. actively searching for these targeted risk mitigations is mandatory whenever we sit down to generate fresh auto home insurance quotes.

managing complex, overlapping household risks highlights the sheer administrative elegance of using a single master document. relying on just one primary point of contact is incredibly beneficial when we face a highly stressful, multi-asset claim scenario. reducing our cognitive load during chaotic emergencies is a direct result of this beautifully streamlined communication channel. evaluating prospective auto home insurance quotes means we must always heavily weight this qualitative, customer-service-driven aspect.

5. DIRECT LINE MULTI PRODUCT FLEXIBILITY AND THE ISOLATED RISK MODEL

encouraging product consolidation while championing an alternative, isolated risk model is the core philosophy at direct line. stopping the dreaded phenomenon of risk contagion is entirely possible because their framework insures every single vehicle individually. triggering a major motor claim by one household member will never damage the hard-earned no-claims discount of another driver. implementing this kind of structural firewall is an absolutely crucial consideration as we compare auto home insurance quotes for busy, multi-driver families.

TIPS:

placing a young driver on an isolated risk model prevents their statistically higher volatility from artificially inflating the premiums for the rest of our household.

rewarding existing motor policyholders who decide to expand their protective umbrella is a highly calculated strategy embedded in their introductory discounts. applying a flat ten percent reduction when we attach property protection to an active vehicle profile is a tactic we see frequently. lowering the financial barrier to entry for robust, comprehensive asset defense is the primary goal of this aggressive cross-selling incentive. leveraging our pre-existing brand loyalty to secure exclusive auto home insurance quotes consistently yields immediate, incredibly tangible economic benefits.

determining the ultimate fit requires us to carefully weigh the isolated risk model against the undeniable convenience of fully unified contracts. younger, higher-risk drivers in the family usually make this distinctly separated approach financially superior for us over the long haul. shielding our broader household budget from brutal, sudden premium spikes means we absolutely must isolate the volatility of inexperienced motorists. conducting a rigorous, mathematical analysis of auto home insurance quotes across both of these structural frameworks is something we highly recommend.

deliberately isolating specific demographic risks inside our household portfolio effectively prevents the financial contamination of low-risk drivers and our stable property assets. treating bundling as a powerful strategic tool, rather than just some default obligation, changes how we manage our wealth entirely.

6. THE ACTUARIAL SYNERGY: WHY INSURERS REWARD POLICY CONSOLIDATION

examining the underlying mathematics of modern risk assessment perfectly explains why major underwriters aggressively push consolidated protection packages. digging into cross-domain risk modeling uncovers a truly fascinating behavioral correlation between meticulous property maintenance and overall driving safety. cautious driving behaviors statistically align with homeowners who proactively maintain their physical dwellings, according to top actuarial data. gathering competitive auto home insurance quotes becomes much more rewarding because this specific actuarial synergy directly justifies those massive bundle discounts.

HOW DO INSURERS BENEFIT FROM US BUNDLING?

linking multiple policies together means we are far less likely to switch, which massively improves customer retention and slashes the insurer’s acquisition costs.

aggressive corporate pricing strategies are also heavily influenced by the sheer, brutal economics of modern customer acquisition. capturing a much larger share of the household wallet from just one family drastically slashes an underwriter’s ongoing marketing overhead. cross-selling to an existing client costs significantly less than launching massive campaigns to acquire a totally brand new customer. funneling these massive operational savings directly back to us results in highly competitive, surprisingly affordable auto home insurance quotes.

consolidating our protective measures under a single corporate umbrella dramatically boosts the long-term retention metrics of that specific institution. jumping to a new provider feels incredibly daunting because the psychological barrier naturally increases alongside the complexity of integrated policies. maintaining intense vigilance against incremental price creeping is our responsibility, even if this stickiness deeply benefits the insurer’s financial stability. ensuring we maintain a fair pricing equilibrium requires us to continuously perform regular market testing through fresh auto home insurance quotes.

7. QUANTIFYING THE SAVINGS: BENCHMARKS AND MATHEMATICAL REALITY

pulling apart average uk car coverage costs, carefully segmented by age and driving experience, is exactly how we establish our accurate benchmarks. seasoned motorists enjoy relatively stable rates in 2026, while inexperienced drivers continue to face profoundly punishing, sky-high baseline tariffs. applying a generic multi policy discount to a mixed household portfolio often severely skews the perceived value because of this massive pricing discrepancy. calculating the actual, tangible savings derived from our auto home insurance quotes forces us to strictly separate our property baselines from our motor baselines.

NOTE:

realizing a net saving is impossible if we accept a 20% discount on a base premium that was already secretly inflated 30% above the true market average.

dissecting those heavily advertised ten to twenty-five percent bundle discounts through strict mathematical analysis exposes a few unsettling economic realities. knocking twenty percent off an artificially inflated base rate provides zero real-world savings for our household, as we frequently discover. executing an essential auditing step means we must compare these flashy bundled figures directly against the boring, standalone benchmarks from niche specialist providers. evaluating complex auto home insurance quotes requires us to blindly trust hard empirical data while completely ignoring shiny marketing percentages.

illustrating the stark potential variance between independent pathways and consolidated setups is exactly why we constructed this detailed comparison.

| coverage type | standalone average (£) | bundled average (£) | net difference (£) |

| standard motor | 850 | 720 | 130 |

| buildings & contents | 420 | 350 | 70 |

| combined total | 1270 | 1070 | 200 |

assuming our base risk profiles are perfectly standard, the table above clearly demonstrates a very tangible, immediate monetary benefit. introducing even slightly non-standard variables into the mix, however, will violently distort these clean mathematical projections, a fact we must constantly emphasize. interpreting heavily generalized discount promises requires extreme caution if our household possesses wonderfully complex, multi-layered coverage needs. relying on fully customized auto home insurance quotes remains the single most effective method for guaranteeing highly accurate financial planning.

WARNING:

remaining deeply suspicious of flashy introductory offers that silently expire after 12 months helps us avoid the dreaded loyalty penalty when we re-evaluate our position annually.

assuming a bundled discount will remain financially superior indefinitely is a mistake; we strongly urge everyone to run these exact calculations annually. initial savings presented during the honeymoon phase of a consolidated agreement can be rapidly destroyed by subtle, algorithmic pricing adjustments. keeping a fiercely proactive mindset ensures that the auto home insurance quotes we ultimately choose will continually serve our core economic interests.

8. THE SHARED EXCESS PHENOMENON: A HIDDEN FINANCIAL SAFEGUARD

a critical yet frequently overlooked feature known as the shared excess phenomenon appears when we deeply investigate the internal mechanics of unified contracts. dealing with a single catastrophic event, like a vicious winter storm tearing apart both our roof and our parked cars, is a scenario we occasionally encounter. facing multiple excess charges is bypassed entirely under a consolidated agreement, where we are typically only required to pay one single deductible. uncovering this beautiful, hidden safeguard significantly amplifies the overall appeal of securing truly comprehensive auto home insurance quotes.

REMEMBER:

functioning as a highly valuable feature of bundled policies, a single excess easily saves us hundreds of pounds during a chaotic, major claim event.

incorporating the massive financial relief of a single deductible into our long-term planning is something we simply cannot underestimate during a major crisis. watching a massive falling tree simultaneously crush both a detached garage and the expensive vehicle parked inside is a tragedy we have witnessed firsthand. juggling two entirely separate claims processes while hemorrhaging distinct excess payments generates a tremendous amount of unnecessary emotional and financial distress. anchoring our strategy around auto home insurance quotes that explicitly feature unified excess conditions guarantees a much more robust, comforting safety net.

assuming a shared excess clause applies universally to all concurrent incidents is dangerous; we must meticulously verify the exact legal wording first. coordinated criminal activities, such as simultaneous home burglary and vehicle theft, are sometimes excluded by institutions that restrict this benefit exclusively to natural disasters. grasping the absolute boundaries of this specific financial protection requires us to read the complex policy definitions incredibly closely. relentlessly interrogating the fine print attached to any prospective auto home insurance quotes represents a strictly non-negotiable step in our entire acquisition process.

9. NAVIGATING THE UNDERINSURANCE TRAP IN HOME QUOTES

conflating a property’s rebuild cost with its current market value is a highly critical, incredibly common error we continuously observe during the quotation phase. land valuation is baked directly into the market value, whereas the strict rebuild cost solely accounts for raw reconstruction materials and necessary labor, a distinction we must master. paying for heavily inflated premiums that provide absolutely zero practical protection is the usual result of accidentally insuring a property for its full market value. dialing in these specific parameters accurately is wonderfully vital whenever we set out to request our customized auto home insurance quotes.

WHAT IS THE DIFFERENCE BETWEEN MARKET VALUE AND REBUILD COST?

selling your house today establishes its true market value, while paying for the labor and raw materials to construct it from scratch dictates the actual rebuild cost.

protecting our specialized electronics and high-value collectibles makes the tedious process of compiling a room-by-room inventory incredibly apparent and necessary. replacing bespoke furnishings or highly specialized equipment usually costs far more than what generic, algorithmic contents estimates will ever cover, as we consistently note. suffering devastating financial shortfalls during a tense claims settlement process is the direct penalty for failing to declare these unique items specifically. leaning on rigorous, detailed documentation is the only way to ensure the auto home insurance quotes we review actually reflect our true physical exposure.

TIPS:

photographing and detailing our personal belongings with a dedicated room-by-room inventory app provides us with incredibly vital evidence should we ever face a major claim.

consecutive annual cycles allow quiet inflation to dramatically rot away the core accuracy of our initially stated coverage limits. accounting for the ever-rising costs of imported goods and raw construction materials is why we strongly recommend applying an index-linked buffer. defending ourselves against the terrifying prospect of accidental underinsurance is much easier with policies that automatically adjust for underlying economic inflation. filtering the market for auto home insurance quotes that explicitly incorporate these dynamic, automatic adjustment features is something we naturally prioritize.

initial risk assessments frequently neglect the crucial step of surveying our valuable external property assets, like custom outbuildings or incredibly high-end landscaping. replacing detached structures fully is often impossible because standard policy limitations quietly cap the maximum payout far below the true, current replacement value. finalizing a truly ironclad defensive strategy means adjusting these specific sub-limits is an absolutely crucial, mandatory exercise. reviewing truly comprehensive auto home insurance quotes means we should see the exact boundaries of our external physical asset protection detailed transparently.

10. MODERN HOUSEHOLD RISKS: LIABILITY AND THE GIG ECONOMY

multigenerational living arrangements brilliantly highlight how the rapid evolution of the modern household introduces deeply complex, new liability implications. altering our daily occupancy dynamics by having elderly parents move in or adult children return home suddenly exposes us to entirely unique risks. guaranteeing adequate, ironclad protection for every single resident requires us to completely reassess our personal liability thresholds following any major structural household change. matching the highly nuanced realities of our specific, current living situations is exactly what comprehensive auto home insurance quotes are designed to do.

WARNING:

engaging in business use like hosting paying guests or working as a delivery driver can instantly void our entire policy, seeing as standard agreements strictly exclude these activities.

hiding our participation in the gig economy from our underwriters introduces a surprisingly severe, immediate danger to our long-term financial security. standard motor coverage agreements are instantly invalidated the moment we find ourselves using a personal vehicle for totally undisclosed ridesharing gigs. demanding specialized commercial endorsements becomes necessary because operating a quiet home-based business fundamentally alters the legal liability profile of our residential property. laying out all of our income-generating activities with total transparency is a strict requirement whenever we start seeking fresh auto home insurance quotes.

- undisclosed delivery driving invalidates standard domestic and commuting motor policies.

- home-based client visits require explicit public liability endorsements on residential coverage.

- storing commercial inventory at a private residence breaches standard contents terms.

- renting out spare rooms temporarily alters the fundamental risk profile of the dwelling.

failing to adequately address the messy intersection of commercial and personal risk creates a terrifying grey area within most standard policies. deriving a significant portion of our household income from gig-based endeavors or freelance work means we really should consult directly with specialist brokers. bridging the dangerous gap between pure commercial liability and standard residential protection is something these experts achieve by identifying highly bespoke products. supporting the complex nuances of these modern hybrid lifestyles is incredibly difficult, which is why standard auto home insurance quotes rarely provide the necessary depth.

11. THE ART OF THE SWITCH: MIGRATION STRATEGIES FOR MAXIMUM EFFICIENCY

optimizing our ultimate financial outcome when migrating between different coverage providers depends heavily on our mastery of timing. actuarial algorithms consistently offer their absolute most competitive rates during a highly specific, three-week sweet spot right before our official renewal date, as we have identified. generating inflated, incredibly punishing premium proposals is the invariable result of either initiating our searches way too early or waiting until the absolute final day. extracting the maximum possible value from any prospective auto home insurance quotes requires us to completely master this delicate, algorithm-driven timeline.

WHEN IS THE BEST TIME TO GET A QUOTE?

snagging the absolute lowest prices often happens when we request a quote roughly 21 to 26 days before the new policy is officially scheduled to commence, according to recent pricing research.

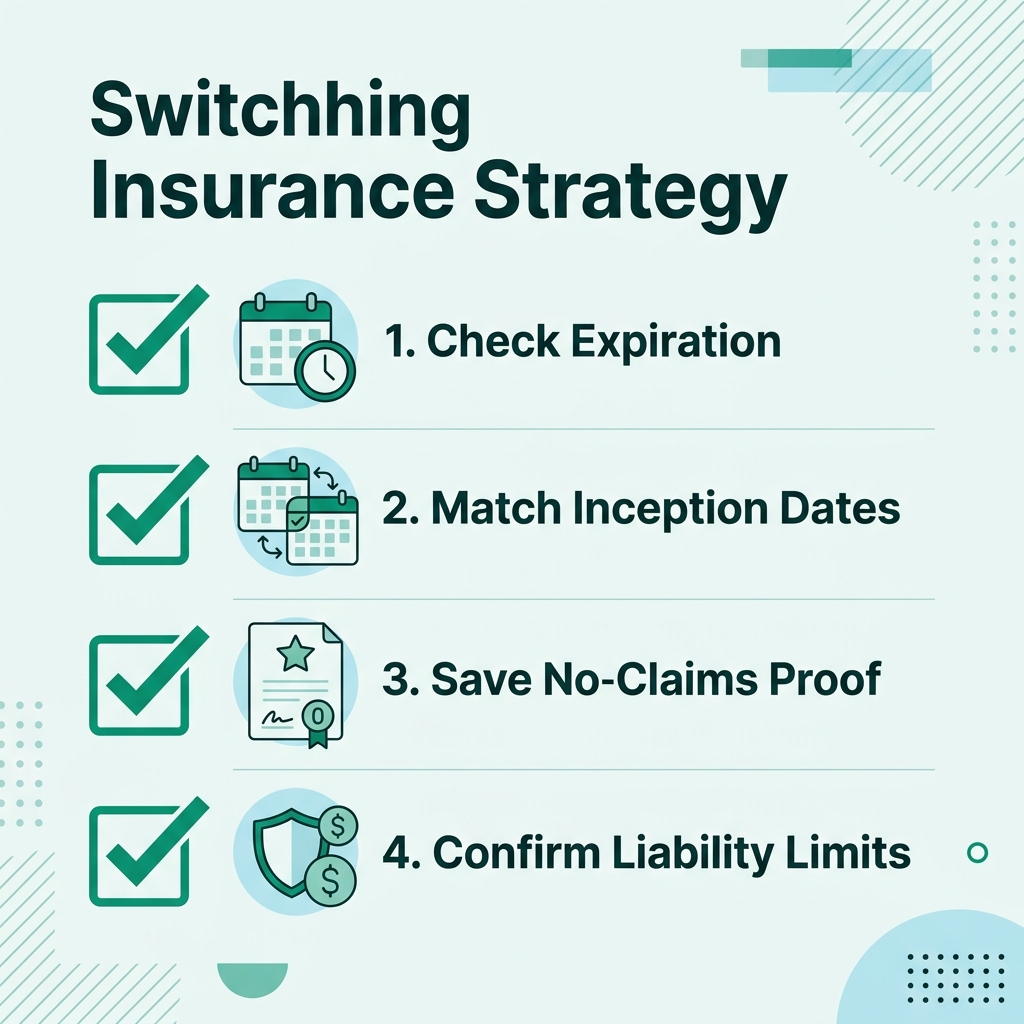

preventing terrifying, temporary gaps in our daily protection requires us to execute a completely seamless transition using a highly meticulous audit checklist. aligning the exact inception dates of our new unified contracts perfectly against the cancellation of our old agreements is something we absolutely must verify. jeopardizing our driving privileges and committing a serious legal violation can occur from a coverage lapse lasting just a few short hours.

- confirm the exact expiration time of current standalone policies.

- schedule the new consolidated agreement to begin one hour before the old ones expire.

- download all proof of no-claims bonuses before terminating existing online accounts.

- verify that the chosen auto home insurance quotes explicitly cover the transition period.

factoring in the painful exit fees associated with breaking a current agreement mid-term serves as a strictly mandatory step within our broader migration strategy. migrating to a consolidated package immediately sometimes backfires when we discover that the hefty administrative penalties completely devour our projected savings. exposing the true net benefit of a switch requires us to aggressively factor in every single hidden charge quietly levied by the departing institution. applying rigorous, uncompromising mathematical scrutiny guarantees that the specific auto home insurance quotes we pursue will genuinely elevate our overall financial standing.

12. NEGOTIATION INTELLIGENCE: HAGGLING WITH RETENTION DEPARTMENTS

unlocking highly lucrative, totally unadvertised bundling bonuses from corporate retention departments requires us to apply very specific psychological negotiation techniques. holding concrete alternative proposals from competing institutions and hard empirical data is the only way we should ever approach these tense conversations. authorizing much deeper, highly discretionary discounts is frequently triggered within their internal algorithms the moment we express a genuine, calculated willingness to migrate our entire portfolio. elevating standard auto home insurance quotes into truly exceptional deals is perfectly achievable when we properly leverage this advanced negotiation intelligence.

NOTE:

prompting a retention agent to magically authorize a vastly superior “manual” discount usually happens the second we strategically mention competing offers from rival, well-known brands.

facing incremental, stealthy price hikes as loyal customers creates a toxic environment of price walking that demands an incredibly proactive defensive posture from us. penalizing our inertia through subtle optimization algorithms remains a widespread practice, even though we know regulatory bodies have valiantly attempted to curb it. pushing our unblemished claims history and long-standing loyalty directly into the underwriter’s face serves as an incredibly powerful, effective negotiating lever. dominating these critical renewal discussions becomes much easier when we casually utilize highly competitive auto home insurance quotes as undeniable, heavy leverage.

choosing aggressive confrontation rarely works, whereas maintaining a polite yet fiercely firm demeanor during intense telephone negotiations consistently yields vastly superior outcomes. reflecting our true, low risk through a mutually beneficial pricing structure is the ultimate goal when we aim to collaborate nicely with the representative. bypassing the tight script restrictions placed on basic frontline customer service agents is sometimes possible if we calmly request a rapid escalation to a senior manager. proving our conversational finesse and endless persistence is often the deciding factor in successfully securing the absolute best auto home insurance quotes.

13. WHEN BUNDLING FAILS: THE CASE FOR STANDALONE POLICIES

accepting that unified packages are absolutely not a magical, universal panacea is crucial, especially when our profile includes highly unusual specialist risks. breaking the rigid, standard algorithms utilized by mass-market underwriters happens instantly when households incorporate heavily modified vehicles or unpredictable teen drivers. contaminating the baseline pricing of our entire portfolio is the usual consequence of recklessly inserting these highly volatile elements directly into a tightly bundled arrangement. overriding the shiny appeal of combined auto home insurance quotes is necessary in these messy scenarios, as we must instead isolate the specific danger using targeted, standalone policies.

REMEMBER:

utilizing a standard bundle usually fails when dealing with modified vehicles or high-risk flood areas, forcing us to rely on expert specialist brokers who can tailor coverage much more effectively.

specialized, highly tailored attention is absolutely demanded by properties situated directly in high-risk flood zones or built using totally non-standard construction methods. applying massively prohibitive financial penalties to the bundle, or simply refusing to cover the anomalies altogether, is how mainstream providers typically react, as we frequently find. seeking out niche underwriters who truly comprehend these complex, specific structural nuances guarantees us vastly superior protection alongside highly accurate property valuations. managing entirely unconventional physical assets requires us to completely ignore basic, heavily generic auto home insurance quotes and look further afield.

beating out traditional loyalty bundles with purely standalone, new-customer introductory rates is a fascinating byproduct of the incredibly aggressive acquisition strategies deployed by certain firms. outshining a neatly consolidated package is sometimes achieved simply by combining a promotional property discount with a heavily subsidized motor rate, an anomaly we occasionally discover. comparing heavily fragmented setups against tightly integrated structures via rigorous parallel calculations is exactly how we exploit this glaring market inefficiency. validating the true, mathematical efficacy of our auto home insurance quotes means exhaustive, side-by-side comparison remains our only viable strategy.

14. THE FUTURE OF BUNDLING: IOT, AI, AND HYPER-PERSONALIZATION

ushering in an entirely new era of hyper-dynamic pricing models across the industry is the rapid, widespread integration of telematics and smart home sensors. transitioning away from boring, static annual assessments, we are now witnessing a fascinating shift toward real-time risk evaluations fueled by continuous, massive data streams. monitoring absolutely everything from the moisture levels hiding in our basements to our aggressive highway braking patterns is now seamlessly handled by embedded internet of things devices. reflecting our highly precise daily behaviors is now possible because underwriters leverage this immense wealth of data to generate incredibly personalized auto home insurance quotes.

TIPS:

bringing down our overall risk profile and unlocking far lower future rates is easily accomplished by simply installing a modern telematics device or a smart leak detection system.

calculating complex future risks within the uk market is being fundamentally altered as artificial intelligence aggressively drives advanced predictive claims modeling. anticipating sudden environmental hazards or quiet mechanical component failures with totally unprecedented accuracy is something we observe modern machine learning algorithms executing flawlessly. offering proactive, life-saving intervention services, rather than just mailing out purely reactive financial compensation checks, is now a reality thanks to this immense predictive capability. becoming increasingly fluid and breathtakingly customized is the inevitable destiny for the underlying structure of auto home insurance quotes as these technologies rapidly mature.

pushing toward intense hyper-personalization naturally raises incredibly valid concerns surrounding basic data privacy and the terrifying potential exclusion of vulnerable, higher-risk demographic segments. dictating our personal access to fundamental financial protections via opaque algorithms introduces massive ethical implications that we absolutely must navigate carefully. forcing massive transparency regarding exactly how our private behavioral data secretly influences final pricing decisions remains a hugely critical challenge for both average consumers and powerful regulators alike. balancing immense technological efficiency perfectly against basic consumer rights will heavily define the upcoming, next generation of customized auto home insurance quotes.

automating the incredibly tedious claims process entirely through the use of blockchain-based smart contracts is exactly what we expect as these digital frameworks continue to radically evolve. accelerating critical payout timelines for fully authenticated incidents while simultaneously slashing massive administrative overhead is the primary benefit of this technological transition. participating in these highly exclusive, beautifully optimized risk pools will unfortunately require us to dramatically adapt our traditional expectations regarding total personal privacy. pointing directly toward a seamlessly integrated, fully digital ecosystem is the undeniable trajectory for the continuous evolution of modern auto home insurance quotes.

15. STRATEGIC CONCLUSION: SYNTHESIZING A ROBUST PERSONAL PROTECTION PORTFOLIO

abandoning deeply ingrained, passive renewal habits and lazy, generalized assumptions is absolutely demanded if we want to synthesize a truly robust personal protection portfolio. defining the modern underwriting landscape are incredibly complex structural nuances and harsh macroeconomic realities that we must actively, aggressively engage with. exposing ourselves to dangerously inflated premium structures and terrifying hidden coverage gaps is the direct consequence of blindly relying solely on the hollow promise of basic administrative convenience. serving as the absolute cornerstone of highly effective household risk management is our relentless, consistent pursuit of perfectly accurate auto home insurance quotes.

REMEMBER:

treating our underlying financial protection as a vital strategic asset means we must manage it with the exact same intense care we apply to our retirement accounts or stock portfolios.

hinging entirely upon highly unique, deeply individual household variables, the monumental decision to either bundle or strictly separate our policies is something our ongoing analysis definitively confirms. isolating highly volatile or unusual specialist risks is sometimes necessary, and we must heavily weigh that need against the incredibly tempting actuarial synergies of total consolidation. maximizing the absolute peak value of our ongoing financial commitments is guaranteed only when we cleverly employ advanced negotiation intelligence alongside calculated, strategic migration techniques. transforming the boring acquisition of auto home insurance quotes from a dreaded annual chore into a massive, undeniable strategic advantage is easily achieved by rigorously applying these exact methodologies.

requiring fiercely proactive market engagement and endless, continuous education is the only way to successfully navigate the intense complexities of modern dual-asset protection. empowering our own crucial financial decisions means we firmly remain fully committed to endlessly dissecting the highly secretive, evolving strategies deployed by massive corporate underwriters. refining our unique ability to secure truly optimal, rock-solid coverage will depend heavily on how quickly we adapt to these massive, impending technological shifts. securing incredible, lasting peace of mind within an increasingly terrifying, unpredictable world ultimately comes down to thoroughly mastering the subtle nuances of securing the best auto home insurance quotes.

CONCLUSION

securing highly reliable coverage for our absolute most valuable physical assets means we have successfully navigated an incredibly dense, multifaceted corporate environment. realizing that a lazy, one-size-fits-all approach is deeply, inherently flawed is the first lesson we learn when unpacking the bizarre intricacies of isolated risk models and multicover discounts. extracting absolute maximum value from absolutely any major financial institution becomes highly probable once we finally understand the complex, underlying actuarial mechanics driving their specific decisions. eliminating incredibly costly, hidden coverage gaps and ruthlessly negotiating vastly superior terms is easily accomplished when leveraging this powerful, insider knowledge. acting as our ultimate, impenetrable defense against rampant premium inflation is the simple habit of aggressively analyzing all incoming auto home insurance quotes through a highly skeptical, critical lens.

evolving our personal strategies concurrently is strictly mandatory as the broader market rapidly transitions heavily toward intense dynamic pricing and AI-driven predictive modeling. redefining exactly how our core baseline risks are coldly calculated by faceless algorithms is the inevitable result of integrating smart home data with advanced automotive telematics. embracing the incredible financial efficiencies these wild new technologies promise is exciting, yet we absolutely must remain fiercely vigilant regarding our own personal data privacy. guaranteeing we are never suddenly caught totally off guard by aggressive, sweeping industry shifts requires us to relentlessly stay highly informed. dedicating ourselves absolutely to continuous, granular market research is the steep, unavoidable price for securing truly optimal auto home insurance quotes.

resting entirely upon our own fiercely proactive efforts, the ultimate responsibility of maintaining a totally robust, impenetrable financial firewall belongs exclusively to us. expecting blind, historical loyalty to magically shield us from brutal macroeconomic inflationary pressures or sneaky algorithmic price walking is a massive, costly delusion we cannot afford. guaranteeing our sustained, powerful economic advantage relies directly on mastering the exact timing of the switch while implementing incredibly strict, unforgiving personal auditing schedules. dominating the chaotic annual renewal cycle is completely within our grasp now that we are heavily armed with these highly comprehensive, tested strategies. securing our absolute long-term household stability and peace of mind naturally follows once we completely master the complex, shifting landscape of modern auto home insurance quotes.