Travel Insurance With Asthma: Your Complete Guide to Affordable Cover 2026

Securing flights and reserving hotels usually marks the exciting start of our holiday plans. But a lingering question often interrupts the excitement. Do we actually hold the proper travel insurance with asthma? Countless travelers manage this respiratory condition internationally every year; unfortunately, many of us forget to disclose it or purchase policies full of hidden coverage gaps. Ignoring these policy details risks massive medical bills or emergencies abroad without proper support.

The World Health Organization estimates 262 million people live with asthma globally. Despite this massive number, it routinely stays off standard medical declarations. Thinking a mild inhaler routine doesn’t matter, we might brush past the screening questions. The actual rules are far stricter. Finding appropriate coverage is rarely difficult or overly expensive, making it an absolute necessity for our upcoming trips. Taking a few minutes to verify our documents secures both our physical well-being and our bank accounts.

Inside this guide, we break down exact disclosure methods, policy comparisons, overseas medication management, and emergency action plans. Our goal is simple: organizing the facts so we can board the plane confidently.

Note:

according to “WHO”, asthma affects an estimated 262 million people worldwide. despite being so common, it remains one of the most frequently undisclosed conditions in travel insurance applications — placing millions of travellers at financial risk.

KEY TAKEAWAYS

- asthma is a pre-existing medical condition that must be declared when purchasing travel insurance

- failing to declare asthma can invalidate your entire policy, not just the medical section

- specialist insurers often offer better value asthma travel insurance than standard providers

- the cost of asthma travel insurance depends on your severity, recent hospital admissions, and destination

- annual multi-trip policies can be more cost-effective if you travel more than twice a year

- always carry a written asthma action plan, your rescue inhaler, and extra medication when travelling

- emergency medical cover should be a priority — not an afterthought — in any asthma travel policy

You Might Also Like

WHAT IS TRAVEL INSURANCE WITH ASTHMA AND WHY DOES IT MATTER?

travel insurance with asthma is not a separate product category — it is a standard travel insurance policy that explicitly includes asthma as a declared pre-existing medical condition within its scope of cover. standard policies typically exclude all costs arising from conditions that predated the policy start date, unless those conditions are specifically declared and a medical premium applied. for people with asthma, the consequence of skipping that declaration step is stark: any treatment costs arising from an asthma-related episode abroad would fall entirely on your own shoulders.

the financial exposure here is genuinely serious. emergency treatment in the united states, parts of australia, or even several european countries can easily run into tens of thousands of pounds. a single severe asthma attack requiring hospitalisation, specialist respiratory care, or an emergency medical repatriation flight could cost far more than years’ worth of insurance premiums combined. the financial logic for obtaining proper asthma travel insurance is compelling — and the reassurance it brings to both traveller and family is, in many ways, priceless.

Can I get travel insurance if I have asthma?

yes — having asthma does not prevent you from getting travel insurance. most mainstream and specialist travel insurers will cover asthma as a declared pre-existing condition. the key is to declare your condition fully and honestly during the application process. your cover and premium will then reflect your specific situation.

it’s worth being clear: travel insurance for asthma sufferers isn’t some obscure niche product available only from a handful of specialist companies. what you’re looking for is a travel insurance policy that accepts your asthma as a declared condition and incorporates it fully within the medical cover section. the difference between providers lies in how they assess your specific asthma, what questions they ask during screening, and what loading — if any — they apply to your premium.

WHY ASTHMA IS CLASSIFIED AS A PRE-EXISTING MEDICAL CONDITION

in the context of travel insurance, a pre-existing medical condition is defined as any health condition, illness, or injury that existed before the policy was purchased. asthma meets this definition without exception — it is a chronic, persistent respiratory condition that doesn’t resolve between holidays. regardless of how mild or how well-controlled your asthma may be at the time of booking, it is always considered pre-existing in insurance terms. that classification doesn’t change based on symptom frequency or medication use.

this creates a genuine area of confusion for people with mild or infrequent asthma. some assume that occasional use of a reliever inhaler doesn’t really “count” as a health condition requiring declaration. according to “Asthma + Lung UK”, this assumption is incorrect. every form of asthma — mild, moderate, or severe — should be disclosed when arranging travel insurance. the severity of your condition may influence the premium you’re quoted, but failing to declare it entirely creates legal and financial risks that no short-term saving justifies.

Remember:

even mild, well-controlled asthma is classified as a pre-existing medical condition by insurers. always declare it — regardless of whether you currently use a preventer inhaler, how infrequently you use your reliever, or how long ago you were diagnosed.

You Might Also Like

DO YOU NEED TO DECLARE ASTHMA ON TRAVEL INSURANCE?

yes — declaring asthma on your travel insurance is not a choice. it is both a legal and a contractual requirement. when you take out a travel insurance policy, you enter into a contract with the insurer that is founded on the legal principle of utmost good faith. that principle requires you to disclose everything a reasonable insurer would want to know when evaluating the risk of covering you. asthma is unambiguously within that category of disclosable information.

the screening process for travel insurance with asthma typically involves answering a series of medical questions — either online or over the phone. you’ll likely be asked when you were diagnosed, whether you use a preventer and/or reliever inhaler, whether you’ve visited a GP, hospital, or A&E for asthma in the past year or two, whether you’ve ever been prescribed oral steroids for asthma, and whether your condition has changed recently. your responses shape the insurer’s risk assessment and determine whether your asthma is covered, excluded, or subject to a premium adjustment.

Tips:

before completing a medical screening questionnaire, gather your asthma records — including the date of diagnosis, your current medications and doses, and any recent GP or hospital visits related to your asthma. having this information ready makes the process faster and ensures your answers are accurate.

some insurers operate automated online screening tools that generate a quote immediately after you answer their questions. others — particularly for more complex asthma histories — prefer to conduct telephone assessments with trained medical underwriters. either way, the process adds only a few minutes to your application, and it’s a non-negotiable step that protects you the moment you set foot outside the country.

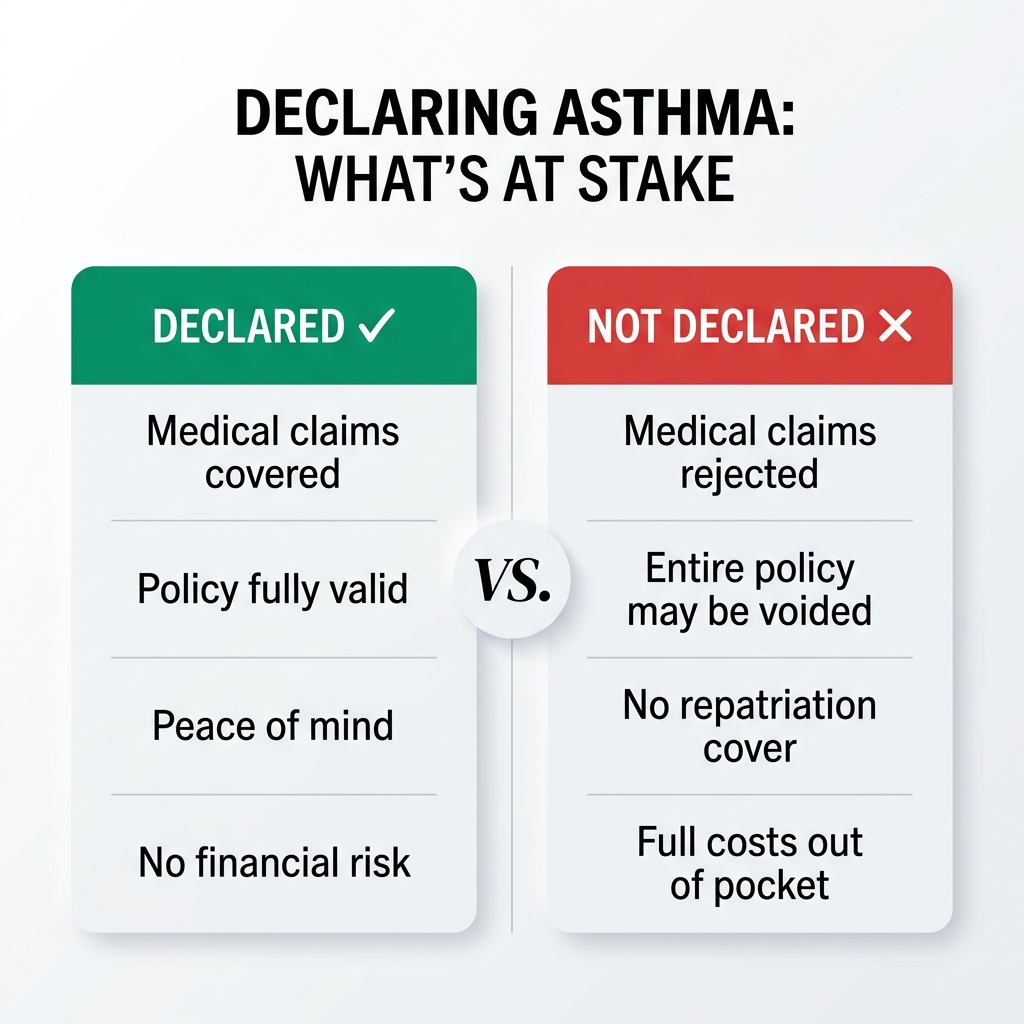

WHAT HAPPENS IF YOU DON’T DECLARE YOUR ASTHMA?

the consequences of non-disclosure are severe and potentially wide-reaching. most immediately, any medical expenses connected to your asthma while abroad will almost certainly be declined. the insurer will access your medical records post-claim, confirm that asthma was a diagnosed, pre-existing condition at the time of purchase, and reject the claim on the basis that it was never declared. you would then bear the full financial cost of treatment — which in some countries can be catastrophic.

what surprises many people is that non-disclosure doesn’t just affect asthma-related claims. if an insurer concludes that material information was withheld at the point of sale, they are legally entitled to void the entire policy. this means no cancellation cover, no lost luggage cover, no personal liability protection — nothing. the “Financial Conduct Authority” (FCA) has addressed this area explicitly, and insurers regularly exercise this right. the cost saving of hiding your asthma in the application is never worth the exposure it creates.

Warning:

failing to declare asthma can result in your entire travel insurance policy being voided — not just the medical section. this means you could lose all protection including cancellation cover, lost luggage, and personal liability, in addition to any asthma-related medical claims being rejected.

the arithmetic here is straightforward. the potential financial damage from an uncovered asthma episode abroad — thousands or tens of thousands of pounds — dwarfs any premium saving achieved by non-disclosure. always declare accurately, and if the cost still feels high, invest the effort in shopping around through specialist platforms rather than gambling with your cover.

WHAT DOES TRAVEL INSURANCE WITH ASTHMA ACTUALLY COVER?

once your asthma is properly declared and confirmed as a covered condition, your policy should protect you across several key areas. the exact scope varies by insurer and by the level of policy you select — which is precisely why reading the policy documents thoroughly matters so much. that said, most well-constructed asthma travel insurance policies share a common set of core protections.

EMERGENCY MEDICAL TREATMENT ABROAD

emergency medical cover is the single most important element when it comes to travel insurance with asthma. this provision pays for the treatment you receive abroad if your asthma deteriorates suddenly — covering local clinic visits, in-patient hospitalisation, specialist respiratory consultations, diagnostic investigations, and any medications prescribed during the episode. many policies also include emergency repatriation under medical supervision if your condition is severe enough to require transport back to the UK.

What does travel insurance cover for asthma sufferers?

when asthma is declared and covered, good travel insurance typically includes: emergency medical treatment abroad, hospitalisation, specialist consultations, prescription medications, emergency repatriation, trip cancellation due to asthma flare-ups, and curtailment cover if you must return home early due to your condition.

the appropriate level of emergency medical cover is heavily influenced by destination. within europe, a Global Health Insurance Card (GHIC) can provide access to state-funded healthcare alongside your policy — but it is not a substitute for comprehensive travel insurance, as it covers neither repatriation nor private treatment. for travel to high-cost healthcare destinations such as the united states or canada, aiming for at least £1 million to £2 million in emergency medical cover is advisable. “Asthma + Lung UK” has highlighted that respiratory emergencies can deteriorate rapidly, making very high cover limits particularly important for asthma travellers.

CANCELLATION AND CURTAILMENT COVER FOR ASTHMA FLARE-UPS

cancellation cover protects you financially if your asthma deteriorates so significantly before your trip departs that you’re hospitalised or your doctor advises you not to travel. in such circumstances, a good policy will reimburse pre-paid, non-refundable costs — including flights, accommodation, and other bookings. asthma is inherently unpredictable: seasonal changes, new triggers, or an unrelated respiratory infection can trigger a significant flare even in people whose condition has been well-controlled for years.

curtailment cover protects you when you’re already at your destination. if an asthma attack or a severe deterioration forces you to return home before your trip ends, curtailment pays for the unused portion of your accommodation and the additional cost of bringing your return journey forward. this element of cover is frequently underestimated — but on a long-haul or high-value holiday, the financial protection it provides can be substantial.

You Might Also Like

HOW MUCH DOES TRAVEL INSURANCE COST FOR ASTHMA SUFFERERS?

the premium for travel insurance with asthma varies considerably, and it’s impossible to give a single representative figure. for people with mild, well-controlled asthma — no recent hospital admissions, no oral steroid dependence, no ongoing destabilisation — the additional loading above a standard policy is often quite modest. in some cases the difference amounts to just a few pounds. for those with a more complex or unstable asthma history, the premium uplift will be more significant. the key in either scenario is to shop around through the right channels rather than accepting the first quote you receive.

Will asthma make my travel insurance more expensive?

not necessarily by a large amount. for many people with mild or well-controlled asthma, the additional premium is relatively small — sometimes just a few pounds. the uplift is larger for those with a history of hospitalisation, frequent oral steroid use, or unstable asthma. shopping around using specialist platforms typically yields the best results.

specialist medical travel insurance comparison platforms — designed specifically for people with pre-existing conditions — consistently outperform standard comparison sites when it comes to finding competitive asthma travel insurance. standard comparison aggregators sometimes struggle to correctly price complex medical histories, while specialist platforms work with underwriters who understand conditions like asthma deeply. the “British Insurance Brokers’ Association” (BIBA) maintains a directory of specialist brokers who can assist with more complex cases. taking the extra time to use these channels is almost always worthwhile.

FACTORS THAT AFFECT THE PREMIUM FOR ASTHMA TRAVEL INSURANCE

insurers evaluate asthma travel insurance applications through the lens of several clinical risk indicators. the current severity of your asthma — mild intermittent versus moderate-to-severe persistent — plays a significant role in the pricing calculation. your recent medical history carries at least equal weight: any hospitalisation, A&E attendance, or course of oral corticosteroids for asthma in the preceding 12 to 24 months signals a higher level of unpredictability to underwriters and typically results in a higher premium.

your destination, trip duration, and age all factor into the final figure as well. european travel to countries with strong healthcare infrastructure is generally assessed as lower risk than long-haul destinations where medical facilities may be limited or treatment costs very high. longer trips carry proportionally greater statistical risk than shorter breaks, and older travellers — particularly those over 60 — typically pay more regardless of condition severity. additional declared conditions on top of asthma — particularly other respiratory, cardiovascular, or immune-related conditions — will also push premiums higher.

none of these factors should discourage honest disclosure. the pricing model exists to fairly reflect risk, not to penalise people for having health conditions. facing a higher-than-expected premium is always preferable to finding yourself financially exposed to a large medical bill with an invalid or voided policy behind you.

HOW TO COMPARE TRAVEL INSURANCE POLICIES FOR ASTHMA

approaching a comparison of asthma travel insurance policies requires a different mindset to reviewing standard cover. the headline premium is just one data point — and arguably not the most important one. what matters far more is whether the policy you’re buying genuinely covers your specific asthma history, at the level your destination and trip type demand. comparing thoughtfully takes a little more time than selecting the cheapest quote, but the difference in protection it provides can be enormous.

the most effective approach is to obtain quotes from multiple sources simultaneously: a mainstream comparison site, a specialist medical travel insurance platform, a dedicated medical travel insurer accessed directly, and — for more complex cases — a broker experienced in pre-existing condition cover. once you have those quotes in front of you, set the premiums aside and examine the policy documents side by side before making any decision.

KEY THINGS TO LOOK FOR IN AN ASTHMA INSURANCE POLICY

when reviewing any candidate policy, start with the most fundamental question: is asthma explicitly confirmed as a covered condition in the documents? some policies accept your declaration at purchase but bury exclusion language in the small print that could complicate or invalidate a claim. clear, unambiguous language confirming that your declared asthma is included in the medical cover — not merely not excluded — is the baseline requirement.

next, verify the emergency medical cover limit. for european travel, a minimum of £2 million is generally recommended; for long-haul destinations, aim for £5 million or more if possible. check explicitly whether repatriation under medical supervision is included. confirm whether the policy provides a genuine 24-hour emergency assistance line — not a voicemail service or a daytime-only contact number. also check whether changes to your asthma medication that occur after the policy is purchased are covered, since some policies only cover the specific regime declared at the point of sale.

Tips:

when comparing asthma travel insurance, create a simple checklist of key elements: medical cover limit (aim for £1-2m+), repatriation included, 24-hour emergency helpline, cancellation for asthma flare-ups, medication changes covered, excess levels, and clarity on asthma being explicitly included — not just not excluded.

scrutinise the cancellation clause carefully. the policy should specifically include asthma flare-ups as a valid reason for cancellation — and the standard of evidence required should be reasonable. some policies demand only a GP letter advising against travel; others impose more stringent evidential requirements. finally, examine the excess applied to medical claims. a policy with a lower premium that carries a very high excess — £500 or more — may provide less value in practice than a slightly more expensive policy with a lower or zero excess.

BEST TYPES OF TRAVEL INSURANCE FOR ASTHMA SUFFERERS

structuring your asthma travel insurance involves two main decisions: choosing between single trip and annual multi-trip cover, and choosing between specialist and standard providers. the right answers depend on how frequently you travel, how complex your asthma history is, and what level of specialist knowledge you want from your underwriter.

SINGLE TRIP VS ANNUAL MULTI-TRIP ASTHMA TRAVEL INSURANCE

single trip travel insurance for asthma sufferers covers a specific, defined journey from your point of departure back to it. it is generally the most economical option if you take one or two holidays per year. the medical screening reflects your condition at the time of booking, and the premium is calculated for that specific trip and destination. for occasional travellers with asthma, single trip policies are straightforward, accessible, and often competitively priced.

annual multi-trip policies cover all journeys taken within a 12-month period, up to a maximum per-trip duration that varies by policy (commonly 31, 45, or 60 days). if you travel three or more times annually, an annual policy frequently works out cheaper overall than purchasing multiple single trip policies. for asthma sufferers who travel regularly, there’s an additional convenience: you declare your condition once at the start of the year, and you don’t need to repeat the medical screening each time you book a trip.

Note:

most annual multi-trip policies have a maximum trip duration per journey — commonly 31 or 45 days. if you plan a longer trip (e.g. a 6-week itinerary), make sure your policy accommodates it, or consider purchasing a single-trip policy for that specific longer journey.

a critical caveat applies to all annual policies: the maximum per-trip duration. if you plan a trip that exceeds this limit — for example a six-week winter escape — your annual policy may not cover it. always verify the maximum trip length before purchasing, and if necessary consider a separate single trip policy for any journey that falls outside it.

SPECIALIST VS STANDARD TRAVEL INSURANCE FOR ASTHMA

specialist medical travel insurers are organisations whose core business is insuring travellers with pre-existing health conditions. their underwriters understand the clinical nuances of conditions like asthma, their screening processes are designed for medical complexity, and their policies are built from the ground up to provide genuine protection for people with ongoing health needs. standard travel insurers, by contrast, are primarily designed for healthy travellers, with medical conditions bolted on as an extension of a general product.

for asthma sufferers with a mild, uncomplicated history and good current control, a standard insurer may well provide adequate cover at a competitive price. however, for those with a history of hospitalisation, frequent courses of oral steroids, or asthma complicated by other conditions, a specialist insurer is typically both more prepared to offer cover and more likely to structure that cover in a way that genuinely protects you. providers including AllClear, Staysure, Insurewith, and Free Spirit Travel Insurance have established reputations as reliable options for people seeking specialist travel insurance for asthma.

HOW TO TRAVEL SAFELY WITH ASTHMA: TIPS BEFORE YOU GO

securing the right insurance is foundational — but it’s only one part of travelling well with asthma. real confidence comes from thorough preparation across every aspect of your trip, from your medical review through to the information you carry in your wallet at the airport. asthma need not dictate where you go or what you do on holiday. with the right preparation, millions of asthma sufferers travel freely and extensively, and you can too.

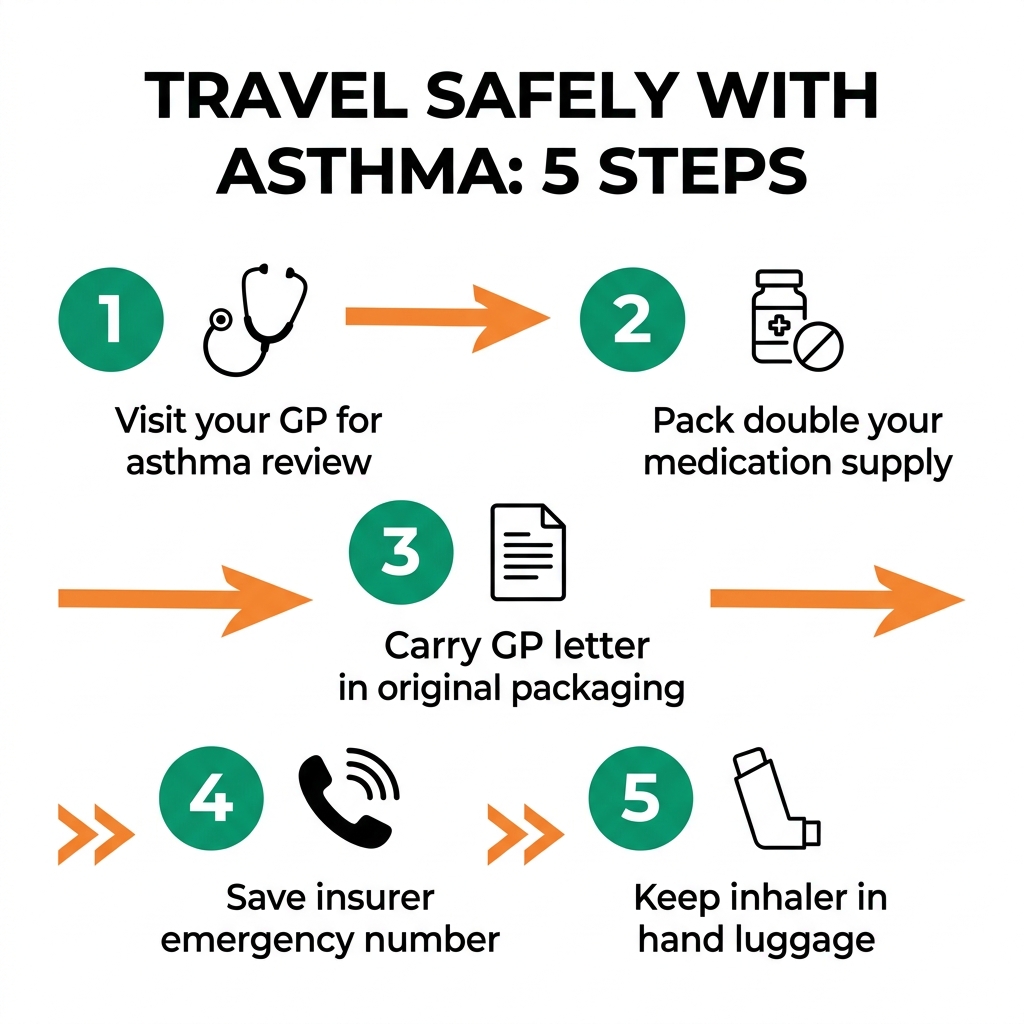

the most important pre-trip step is scheduling a review with your GP or asthma nurse, especially if you haven’t had one recently. this is particularly advisable before long-haul travel, travel to a very different climate, or travel during a period when your asthma has been less stable than usual. a pre-trip review allows your clinician to update your written asthma action plan, optimise your medication, and flag any destination-specific environmental risks — air quality, altitude, pollen, humidity — that might be relevant to your condition.

MANAGING YOUR ASTHMA MEDICATION WHILE TRAVELLING

medication planning is one of the most practical and highest-impact things you can do to travel safely with asthma. “Asthma + Lung UK” recommends carrying at least double your normal medication supply — divided between your carry-on bag and your checked luggage. this redundancy protects against lost baggage, delays, or unexpected extensions to your trip. your reliever inhaler should always be in your hand luggage, accessible at any point during the journey.

all medications should be kept in their original pharmacy packaging with labels clearly intact. countries vary in their regulations around medications — particularly certain inhaler propellants — and original packaging eliminates potential complications at customs and border control. if you travel with a nebuliser, confirm your airline’s policy in advance; most major carriers can accommodate medical devices, but prior notification is usually required. carrying a GP letter or medical certificate confirming your diagnosis and treatment plan gives local healthcare providers an immediately useful clinical picture if an emergency arises.

What should I carry when travelling with asthma?

we recommend always travelling with: your rescue/reliever inhaler in your hand luggage, at least double your usual medication supply, all medications in original packaging with pharmacy labels, a written asthma action plan from your GP, a GP letter confirming your diagnosis and medications, and your travel insurer’s emergency assistance number saved in your phone.

for travel to countries where english is not widely spoken, a brief translated medical summary — listing your condition, current medications, dosages, and any known triggers — can be invaluable. this can usually be prepared with minimal effort using a reliable translation service or through your GP surgery, and it significantly reduces the communication barriers you might face if you need urgent care abroad.

FLYING WITH ASTHMA: WHAT YOU NEED TO KNOW

air travel is generally well-tolerated by people with asthma, and the vast majority fly without any asthma-related incident. that said, a handful of factors specific to the flying environment are worth understanding. aircraft cabins are pressurised to an equivalent altitude of roughly 6,000 to 8,000 feet. this mild degree of reduced air pressure lowers blood oxygen saturation slightly, which is clinically insignificant for most people with asthma — but those with severe asthma or co-existing respiratory conditions should discuss long-haul flight specifically with their doctor as part of their pre-trip review.

the dry air circulated in aircraft cabins can irritate the airways and occasionally trigger symptoms in people who are sensitive to low humidity. drinking plenty of water throughout the flight, avoiding alcohol — which can worsen dehydration — and keeping your reliever inhaler in the seat pocket rather than the overhead storage are all straightforward measures that significantly reduce in-flight risk. for long-haul flights, occasional walks along the aisle also help to maintain circulation and reduce the monotony of extended periods in a fixed position.

airports themselves can present triggers for some people: cleaning products, heavy perfumes, duty-free fragrance counters, and the close proximity of large crowds. if you have known sensitivities to airborne particles or fragrances, passing quickly through trigger-dense areas and wearing a light mask if needed are both practical and reasonable responses. the goal is not to restrict your travel choices — it’s to be prepared.

WHAT TO DO IF YOU HAVE AN ASTHMA ATTACK ABROAD

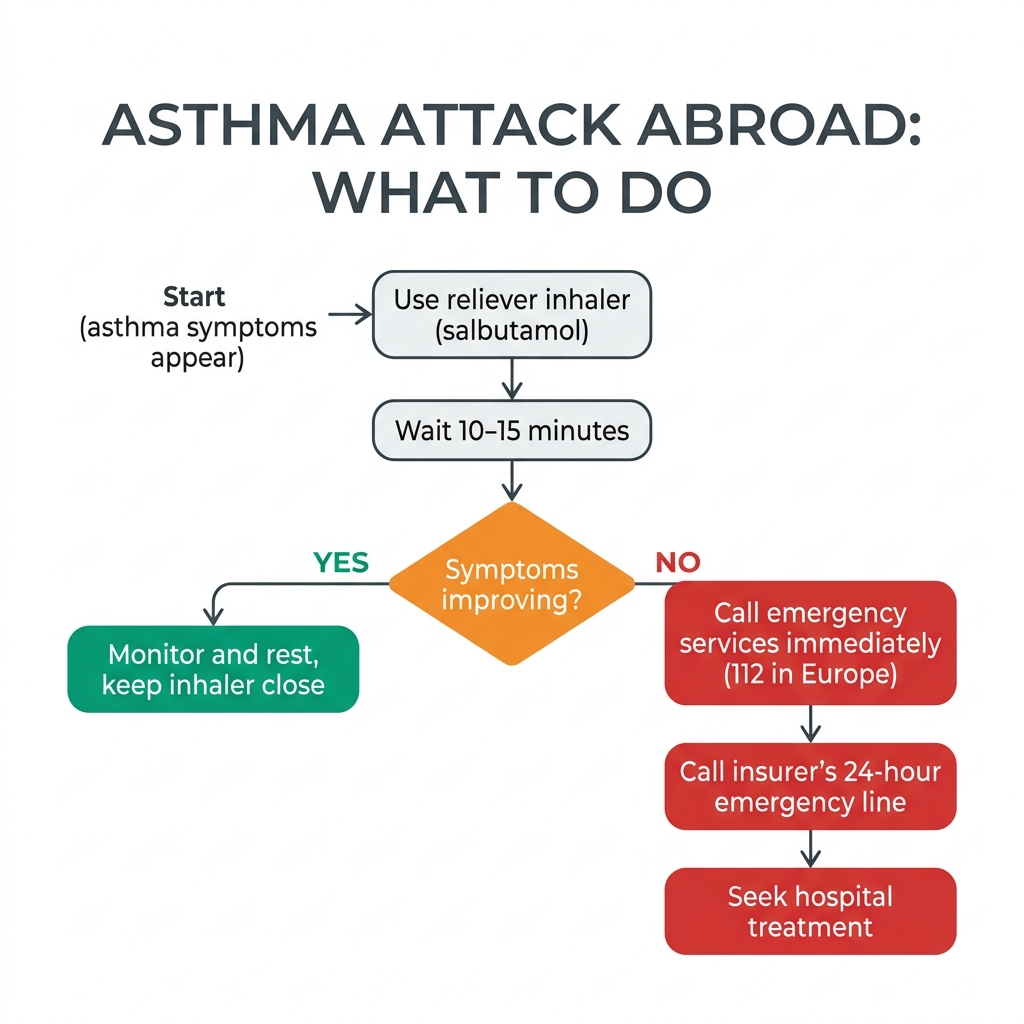

even the most careful preparation cannot guarantee that asthma will never flare while you’re away. knowing your response protocol in advance is as important as any other element of your preparation. if symptoms begin, act immediately according to your written asthma action plan — use your reliever inhaler (typically salbutamol) as directed, sit upright, and try to breathe slowly and as calmly as possible. if your reliever is not immediately accessible, ask someone nearby for assistance.

if symptoms do not improve meaningfully within 10 to 15 minutes of using your reliever, or if they worsen at any point, treat this as an emergency and seek medical help without delay. do not wait for a second or third cycle of treatment before making that call. in europe, 112 is the standard emergency services number across all EU member states. the policy documents provided by your insurer should include the local emergency number for each destination — along with the all-important 24-hour emergency assistance line for your insurer.

Warning:

if your asthma symptoms do not improve after 10–15 minutes of using your reliever inhaler, do not wait and see — seek emergency medical help immediately. respiratory emergencies can escalate quickly. in europe, call 112. have your insurers emergency assistance number already saved in your phone before you travel.

HOW TO USE YOUR TRAVEL INSURANCE EMERGENCY LINE

your insurer’s 24-hour emergency assistance line is one of the most valuable features of any good travel insurance with asthma policy — and it’s worth using early in a deteriorating situation, not only after an emergency is already in full swing. the team on this line can advise on appropriate local medical facilities, liaise directly with treating hospitals, pre-authorise treatment where possible, and provide translation assistance if you’re struggling to communicate in a foreign language. they can also begin the claims process while you’re still being treated, reducing your administrative burden significantly.

save the emergency number in your phone before you travel, and write it down on a physical card that lives in your wallet — separate from your phone. if your phone is lost, stolen, or runs out of power during an emergency, you’ll still be able to access the number. it’s also worth ensuring that your travel companion — or a family member at home — has a copy of the number, your policy number, and your asthma action plan. if you’re incapacitated and unable to communicate the details yourself, having someone who can relay that information to the emergency team could meaningfully speed up the response.

Tips:

before you travel, write your insurer’s emergency assistance number and your policy number on a card and keep it in your wallet — separately from your phone. if your phone is lost or runs out of battery during an emergency, a physical backup could be the difference between swift help and a stressful delay while abroad.

COMMON MYTHS ABOUT TRAVEL INSURANCE WITH ASTHMA

a handful of persistent misconceptions about asthma travel insurance lead people to make decisions that increase their financial risk. the most damaging is the belief that mild asthma is exempt from declaration requirements. this misunderstanding is widespread — and wholly incorrect. every form of asthma, without exception, is a pre-existing condition that must be disclosed. no insurer or regulator defines a lower threshold of severity below which declaration becomes optional.

the second common myth is that travel insurance with asthma is unaffordable or hard to access. neither is true for most people. the majority of mainstream and specialist insurers cover asthma routinely, and for those with well-managed, stable asthma, the additional premium over a standard policy is often negligible. the perception of difficulty usually traces back to the experience of using the wrong comparison tools — standard aggregators that aren’t built for medical declarations — rather than reflecting the actual marketplace for asthma travel cover.

Is a GHIC card a substitute for travel insurance for asthma sufferers in Europe?

no. a Global Health Insurance Card (GHIC) gives access to state healthcare in EU/EEA countries at local rates — but it does not cover private treatment, emergency repatriation, trip cancellation, lost luggage, or asthma-specific cover. it is a valuable supplement to travel insurance, not a replacement for it.

the third widespread myth concerns the Global Health Insurance Card (GHIC). many people believe a GHIC card removes the need for travel insurance when visiting europe. this is incorrect. a GHIC provides access to state-funded healthcare within the EU and EEA at local resident rates — a useful benefit, but a very narrow one. it covers neither private medical treatment, emergency repatriation, nor any of the non-medical aspects of travel insurance such as cancellation, curtailment, lost luggage, or personal liability. relying on a GHIC alone leaves enormous financial risk uncovered.

finally, many asthma sufferers assume that declaring their condition will result automatically in an exclusion — that the insurer will accept their premium but then exclude asthma from the cover entirely. this is a misunderstanding of how the system works. declaring asthma does not trigger exclusion; it triggers assessment and appropriate pricing. exclusions are typically reserved for conditions that are very recent, very unstable, or where the applicant has not engaged with advised treatment. the vast majority of asthma sufferers who apply honestly and accurately will find their condition included in the scope of their cover.

CONCLUSION

travel insurance with asthma is more accessible, more affordable, and less complicated than many asthma sufferers believe — but approaching it correctly does require honesty, care, and a willingness to go through the application process properly. the foundation is accurate, complete declaration of your condition. everything else — comparing policies, understanding cover scope, choosing the right type of policy, and preparing practically for the trip — builds on that foundation to create genuine protection.

asthma doesn’t have to restrict your travel ambitions. with the right asthma travel insurance in place — clearly covering your declared condition, providing appropriately high emergency medical limits, and backed by a genuine 24-hour assistance line — you’re protected against the financial consequences of even the most unexpected respiratory episode. that protection is always worth having, and the risk of being without it is never worth the saving.

every asthma sufferer planning an international trip deserves to travel with real confidence. take time before booking to research your insurance options properly, engage with specialist platforms where helpful, and prepare practically so that your asthma management is never a last-minute thought. your holiday should be defined by great experiences — not by anxiety about what might happen if your asthma acts up. with the right preparation and the right travel insurance with asthma, those experiences are completely within reach.

references and sources

- World Health Organization (WHO) — Asthma Fact Sheet

- Asthma + Lung UK — Travel Insurance Guidance

- Asthma + Lung UK — Travelling with Asthma

- NHS — Asthma Overview

- British Insurance Brokers’ Association (BIBA)

- Financial Conduct Authority (FCA) — Travel Insurance Consumer Guide

- UK Government — Global Health Insurance Card (GHIC)