ACA HEALTH PLANS: YOUR COMPLETE GUIDE TO AFFORDABLE COVERAGE 2026

navigating the complex maze of health insurance often feels like wandering without a map, particularly when you are trying to make sense of aca health plans. we totally understand the frustration that bubbles up when facing terms like premiums, deductibles, and those confusing subsidies, yet finding the correct coverage remains essential for your financial safety and physical health. the affordable care act, which most people know as obamacare, was crafted to make sure health coverage became accessible to everyone, no matter their income level or medical history. at its very core, this system strives to bridge the dangerous gap between high-cost private insurance and the risk of having no protection at all.

we have witnessed firsthand how securing proper health coverage transforms lives, offering not just necessary medical care but also deep peace of mind for families and individuals across the nation. aca health plans represent more than simple insurance policies; they act as a vital safety net ensuring that essential health benefits remain available to people who might otherwise be locked out of the healthcare system. whether you are currently self-employed, working a part-time job, or just exploring your options during the open enrollment window, understanding these plans is your first real step toward protecting your future. let us guide you through the intricacies of the marketplace so you can make a smart, informed decision that fits your specific needs.

Note:

comparing multiple aca health plans before enrolling is crucial, as premiums and provider networks can vary significantly even within the same metal tier.

choosing the optimal plan requires you to balance monthly costs against the potential for medical expenses, a strict calculation that demands careful thought about your personal health circumstances. we aim to simplify this entire process by breaking down the complicated tiers and benefit structures into clear, manageable pieces of information. by the time you finish this guide, you will possess a comprehensive understanding of exactly how aca health plans work and how you can leverage them for maximum protection. join us as we explore the essential details of affordable care act coverage.

KEY TAKEAWAYS

- aca health plans provide comprehensive coverage for pre-existing conditions and essential service.

- subsidies like premium tax credits can significantly lower your monthly insurance costs.

- plans are categorized into metal tiers: bronze, silver, gold, and platinum based on cost-sharing.

- silver plans are the only tier eligible for extra savings through cost-sharing reductions.

- open enrollment occurs yearly, but special situations may qualify you for early access.

WHAT ARE ACA HEALTH PLANS?

UNDERSTANDING THE AFFORDABLE CARE ACT (OBAMACARE)

signed into law back in 2010, the affordable care act fundamentally shifted the landscape of american healthcare by creating a regulated marketplace specifically for insurance. aca health plans are private insurance policies that must comply with strict federal guidelines to ensure fair treatment for every single policyholder. according to the “Centers for Medicare & Medicaid Services”, these regulations stop insurers from denying coverage based on health status, a harsh practice that previously left so many people vulnerable. we recognize that this massive shift has allowed millions of people to access care who were previously deemed uninsurable.

Remember:

under current law, insurance companies are strictly prohibited from denying coverage or charging higher rates due to pre-existing conditions.

these plans are typically sold through federal or state exchanges, which are commonly known as the health insurance marketplace, where consumers like you can compare options side-by-side. we find that the standardization of benefits makes it much easier for you to evaluate policies based on true value rather than worrying about hidden exclusions. essentially, aca health plans guarantee a solid baseline of coverage that protects you from the most common and expensive medical events. this system promotes broad risk pooling, which helps to stabilize premiums over time for everyone involved.

HOW ACA PLANS DIFFER FROM SHORT-TERM OR PRIVATE INSURANCE

it is absolutely crucial to distinguish legitimate aca health plans from those short-term or catastrophic insurance policies that often float around the market. unlike fully compliant plans, short-term insurance is not required to cover essential health benefits or pre-existing conditions, which leaves you exposed to significant financial risk. strictly speaking, non-aca plans might look cheaper upfront, but they often exclude coverage for maternity care, mental health services, or even necessary prescription drugs. we always advise scrutinizing the fine print, as these alternative policies usually come with annual or lifetime limits on exactly what the insurer will pay.

aca health plans, in sharp contrast, offer robust consumer protections that strictly prohibit annual dollar limits on essential coverage. this means that no matter how expensive your medical treatment becomes, your insurance company cannot simply stop paying for covered services. we believe that this unlimited coverage is a cornerstone of financial security for families dealing with chronic illnesses or unexpected emergencies. choosing a compliant plan ensures that you are not left drowning in a mountain of debt after a major health event occurs.

WHO IS ELIGIBLE FOR ACA MARKETPLACE COVERAGE?

eligibility for aca health plans is designed to be incredibly broad, ensuring that the vast majority of legal residents can apply for coverage. to qualify, you must live in the united states, be a u.s. citizen or national, or be lawfully present. additionally, you typically cannot be incarcerated at the time of your enrollment. we often remind people that eligibility for the marketplace does not automatically guarantee financial assistance, but it does guarantee access to a compliant plan.

CAN I GET SUBSIDIES IF I HAVE A JOB?

generally, if your employer offers affordable coverage that meets minimum value standards, you will not qualify for marketplace subsidies, even if basic aca health plans appear cheaper.

individuals who have access to affordable, comprehensive insurance through an employer generally do not qualify for marketplace subsidies, though they can still buy a full-price plan. however, if your employer’s offer is considered unaffordable or does not meet minimum value standards, you might still be eligible for savings on an aca plan. we recommend checking your specific status each year, as changes in income or household size can alter your eligibility for assistance. ultimately, the marketplace is open to nearly everyone looking for solid health protection.

You Might Also Like

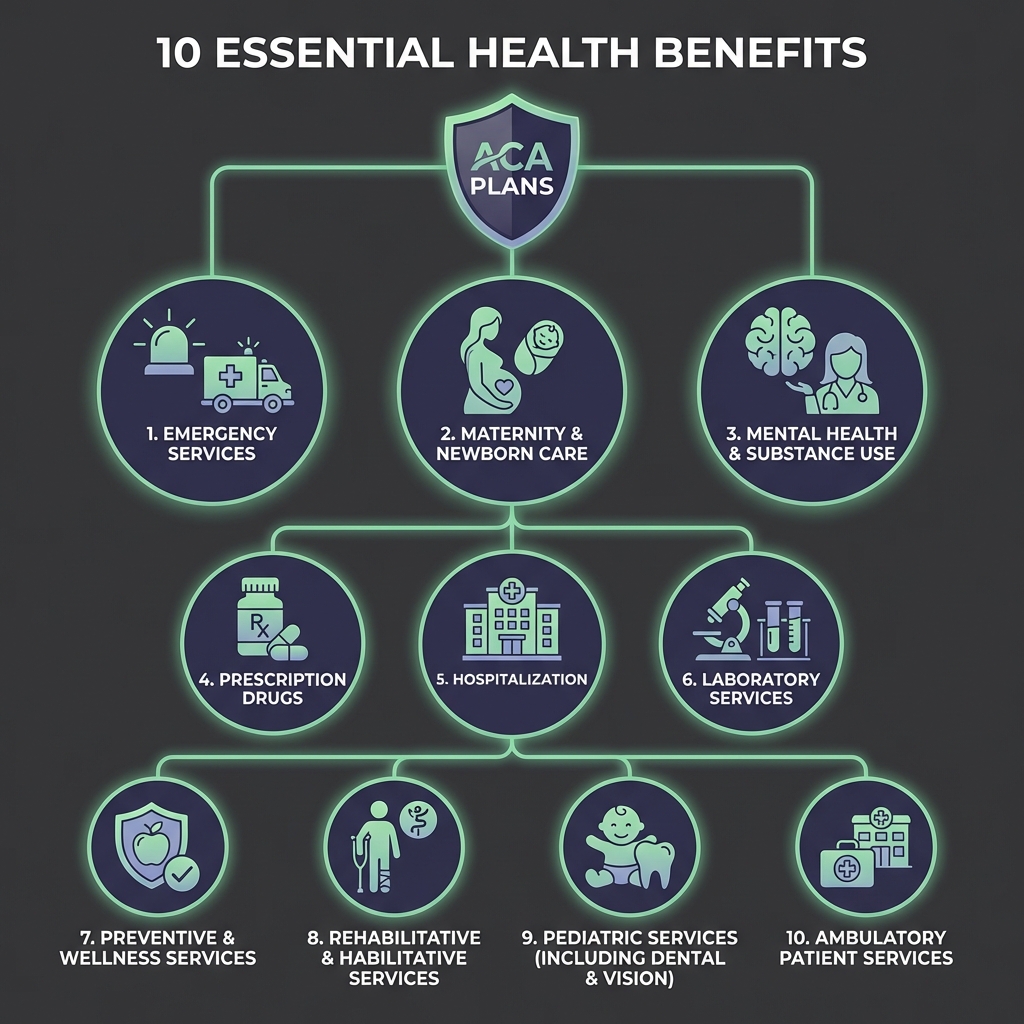

THE 10 ESSENTIAL HEALTH BENEFITS EVERY ACA PLAN MUST COVER

EMERGENCY SERVICES AND HOSPITALIZATION

one of the most critical requirements for aca health plans is the mandatory coverage of emergency services without prior authorization. this ensures that if you face a life-threatening situation, you can seek immediate care at the nearest hospital without worrying about network restrictions or penalties. “Healthcare.gov” confirms that insurance companies cannot charge you higher copayments for out-of-network emergency room visits. we know that in an emergency, the last thing on your mind should be dealing with administrative hurdles.

Tips:

always identify the nearest in-network hospital for non-emergencies, but rest assured that true emergencies are covered at in-network rates anywhere.

hospitalization coverage extends far beyond just the emergency room to include inpatient care like surgeries and overnight stays. costs for hospital services can escalate rapidly, often reaching tens of thousands of dollars for a single admission. aca health plans absorb the bulk of these expenses once you meet your deductible, preventing medical bankruptcy. we view this as a fundamental protection that safeguards your financial future against unpredictable health catastrophes.

MATERNITY, NEWBORN CARE, AND PEDIATRIC SERVICES

before the affordable care act, maternity coverage was often excluded from individual health policies or treated as an expensive rider. today, all aca health plans must cover pregnancy, labor, delivery, and newborn care as standard benefits. this shift ensures that expectant mothers receive necessary prenatal screenings and support without facing discriminatory pricing. we celebrate this change as a vital step toward improving maternal and infant health outcomes across the country.

Note:

comprehensive maternity care includes prenatal visits, screenings, and breastfeeding support, ensuring a healthy start for both mother and baby.

pediatric services extend this protection to children, covering their medical needs including dental and vision care. unlike adult dental and vision coverage, which is optional in most exchange, pediatric care is deemed essential. “The American Academy of Pediatrics” emphasizes the importance of early preventative care, which is fully supported under these guidelines. we encourage parents to verify the specific pediatric network providers to ensure their children have access to the best available care.

MENTAL HEALTH AND SUBSTANCE USE DISORDER SERVICES

mental health is just as important as physical health, and aca health plans are required to treat them equally. coverage includes behavioral health treatment such as psychotherapy and counseling, as well as inpatient services for mental health conditions. importantly, plans generally cannot impose stricter limits on mental health visits than they do on medical or surgical visits. we see this parity as essential for removing the stigma and barriers associated with seeking help.

Warning:

federal parity laws require insurers to cover mental health services comparably to medical services, so report any discrepancies if you face coverage denials.

substance use disorder treatment is also a mandated benefit, ensuring access to rehabilitation and recovery services. this includes coverage for detoxification, outpatient counseling, and medication-assisted treatment where appropriate. the “Substance Abuse and Mental Health Services Administration” reports that expanding access to these services saves lives and strengthens communities. we believe that comprehensive coverage helps individuals recover and regain control of their lives without the crushing burden of treatment costs.

PRESCRIPTION DRUGS AND PREVENTIVE WELLNESS VISITS

prescription drug coverage is a standard feature of every compliant plan, ensuring you have access to necessary medications. insurers organize drugs into tiers, with generic medications typically costing less than brand-name drugs. while the specific formulary—the list of covered drugs—varies by plan, all therapeutic categories must be represented. we advise reviewing the formulary carefully if you rely on specific medications to manage a chronic condition.

ARE ALL MY MEDICATIONS COVERED?

not necessarily. each plan has a unique formulary, so you must check if your specific prescriptions are included before enrolling.

preventive services are perhaps the most accessible benefit, often provided at zero cost to the policyholder. this includes immunizations, cancer screenings like mammograms and colonoscopies, and annual wellness check-ups. according to the “CDC”, preventive care significantly reduces the risk of developing severe diseases later in life. we emphasize taking full advantage of these free services to maintain your health and catch potential issues early.

KEY PROTECTIONS: NO PRE-EXISTING CONDITION EXCLUSIONS

the prohibit on denying coverage for pre-existing conditions is arguably the most popular provision of the aca health plans. prior to this law, individuals with asthma, diabetes, or even a history of cancer could be denied insurance or charged exorbitant rates. now, insurers must accept all applicants and cannot charge more based on health status or gender. we regard this protection as a moral imperative that ensures healthcare is a right, not a privilege for the healthy.

WILL ILLNESS INCREASE MY PREMIUMS?

no, insurers cannot charge you more based on your health history or current medical conditions; rates are based only on age, location, and tobacco use.

this protection extends to coverage limitations; insurers cannot refuse to pay for treatment related to your pre-existing condition. once you are enrolled, your benefits apply fully to all your medical needs from day one. we know this brings immense relief to millions who previously lived in fear of losing their coverage or being priced out of the market. security and fairness are the bedrock principles of the current system.

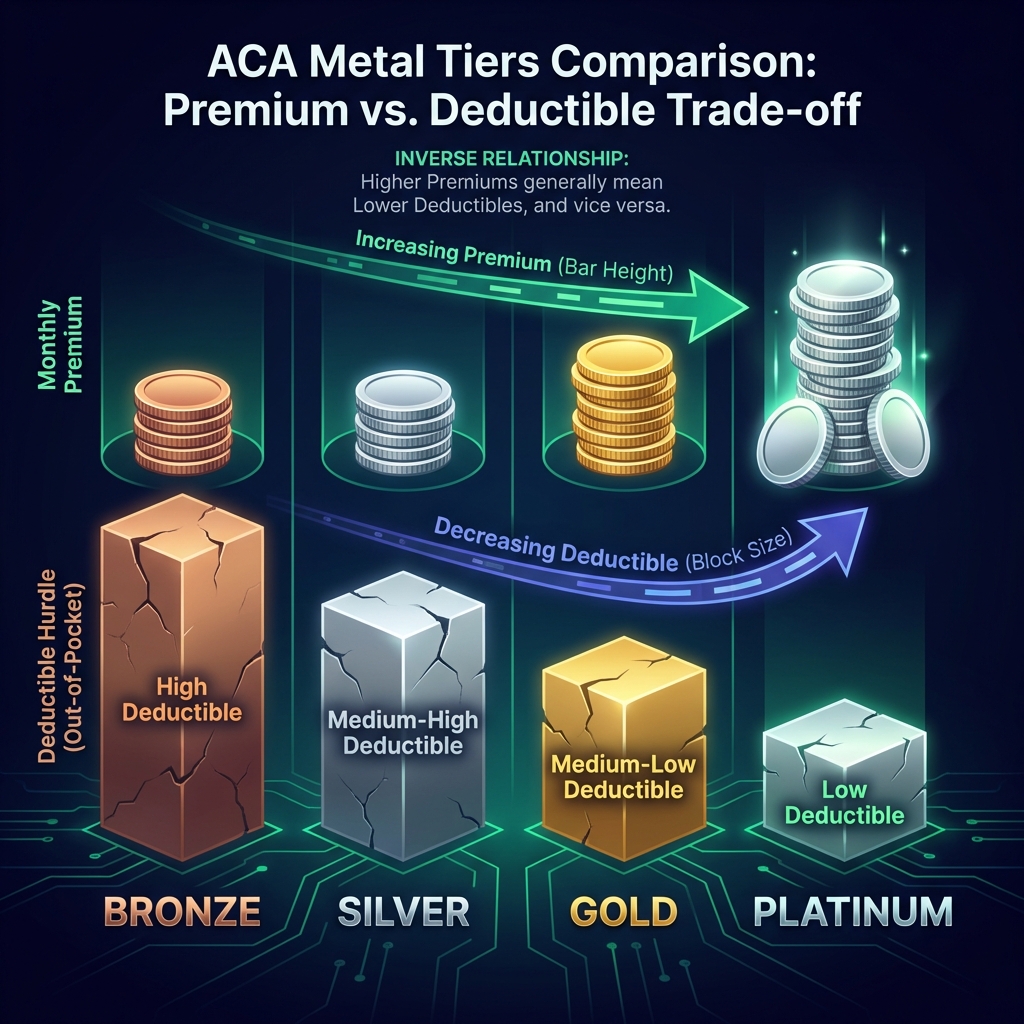

UNDERSTANDING ACA METAL TIERS: BRONZE, SILVER, GOLD, AND PLATINUM

BRONZE PLANS: LOWEST PREMIUMS, HIGHER DEDUCTIBLES

bronze plans are designed for those who want to minimize their monthly payments while maintaining protection against serious medical issues. these plans typically have the lowest premiums among the metal tiers but come with the highest deductibles and out-of-pocket costs. “KFF” analysis suggests that bronze plans cover about 60% of total average acts costs for the insured population. we consider these plans suitable for healthy individuals who do not expect to see a doctor frequently.

Warning:

while monthly costs are low, a serious illness on a bronze plan could result in thousands of dollars in out-of-pocket expenses before coverage kicks in.

however, because of the high deductible, you will pay full price for most routine care until that threshold is met. practically, this means a broken arm or minor surgery could cost you thousands out of pocket before insurance kicks in. we caution potential buyers to have an emergency savings fund if they choose a bronze plan. it is a trade-off between immediate monthly savings and potential future expenses.

SILVER PLANS: THE “BENCHMARK” FOR COST-SHARING REDUCTIONS

silver plans occupy the middle ground, offering a balance between monthly premiums and out-of-pocket costs. on average, they act to cover about 70% of healthcare costs, making them a moderate choice for many families. crucially, silver plans are the only category eligible for cost-sharing reductions (csr) if your income qualifies. we find that for many lower-income households, a silver plan with csr offers essentially platinum-level coverage at a reduced price.

Tips:

if you qualify for cost-sharing reductions, you must select a silver plan to receive the benefits of lower deductibles and copays.

these plans serve as the benchmark for calculating premium tax credits, influencing the subsidy amount you receive. for most consumers, silver plans provide the best value sweet spot, especially when subsidies are applied. we strongly recommend checking your eligibility for cost-sharing reductions before overlooking the silver tier. often, the extra financial protection makes a silver plan far superior to gold or bronze options.

GOLD AND PLATINUM PLANS: HIGHER PREMIUMS, LOWER OUT-OF-POCKET COSTS

gold plans act to cover approximately 80% of medical costs and come with higher premiums but lower deductibles than silver or bronze. these are increasingly popular for individuals who know they will need regular medical care, such as frequent specialist visits or expensive prescriptions. by paying more each month, you significantly reduce the bill you see at the checkout counter. we see gold plans as a smart investment for those managing chronic conditions.

Note:

paying a higher premium for a gold or platinum plan can save you money overall if you frequently utilize medical services and prescriptions.

platinum plans sit at the top of the tier, covering about 90% of costs, drastically minimizing your out-of-pocket exposure. they have the highest monthly premiums and are relatively rare in some operational markets. offering nearly complete coverage from the start, platinum plans are best for those with very high expected medical usage. we advise calculating your total annual health spend to see if the higher premium pays for itself in savings.

CATASTROPHIC PLANS: COVERAGE OPTIONS FOR UNDER-30S

catastrophic plans are a separate category available principally to people under 30 or those with a hardship exemption. they feature very low monthly premiums but incredibly high deductibles, offering a safety net primarily for worst-case scenarios. routine care is generally not covered until the deductible is met, except for three primary care visits per year and preventive services. we view these as a strictly emergency option for young, healthy adults.

importantly, catastrophic plans are not eligible for premium tax credits or other subsidies, meaning you pay the full sticker price. often, a subsidized bronze or silver aca health plan works out to be cheaper than a catastrophic plan. we recommend careful comparison, as you might get better coverage for less money on standard metal tier. never assume catastrophic is the cheapest option without checking the numbers.

You Might Also Like

ACA SUBSIDIES AND FINANCIAL ASSISTANCE

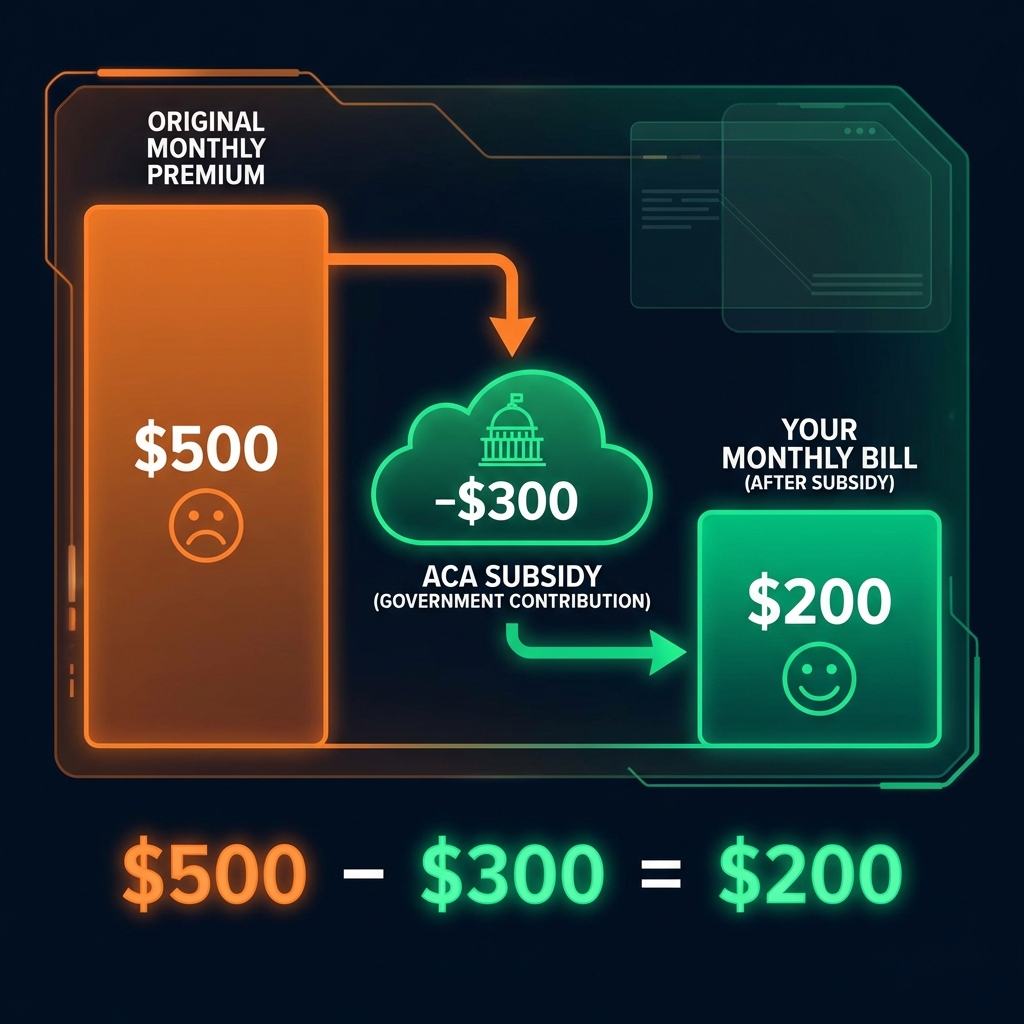

HOW PREMIUM TAX CREDITS (PTC) LOWER YOUR MONTHLY PAYMENT

premium tax credits are the primary mechanism making aca health plans affordable for millions of americans. these credits work on a sliding scale based on your household income relative to the federal poverty level. essentially, the government pays a portion of your premium directly to the insurance company, and you pay the remaining difference. we have seen these credits reduce monthly premiums to under $10 for many eligible consumers.

Remember:

you must reconcile your premium tax credit when you file your federal taxes to ensure you received the correct amount based on your actual income.

you can choose to use some, all, or none of your tax credit in advance to lower your monthly bill. if you use less than you qualify for, you get the difference back as a refund when you file your taxes. conversely, if your income increases during the year, you may have to repay some of the credit. we advise reporting income changes immediately to keeping your subsidy accurate and avoiding tax time surprises.

EXPLAINING COST-SHARING REDUCTIONS (CSR) FOR SILVER PLANS

cost-sharing reductions go a step further than premium credits by lowering the actual amount you pay for medical services. available only with silver plans, these reductions decrease your deductible, copayments, and coinsurance. for example, a standard silver plan deductible might drop from $4,000 to just a few hundred dollars with strong csr eligibility. we consider this one of the most valuable, yet often misunderstood, features of the marketplace.

DO I APPLY SEPARATELY FOR CSR?

no, your eligibility is automatically calculated based on your income when you apply, but you must choose a silver plan to activate it.

eligibility depends also on income, typically favoring those earning between 100% and 250% of the federal poverty level. unlike tax credits, you do not have to “reconcile” these savings on your tax return; the benefit is applied automatically to the plan design. if you qualify, upgrading to a silver plan is almost always the financially sound choice. we urge you to look beyond the premium price and see the real value of reduced out-of-pocket maximums.

INCOME LIMITS AND ELIGIBILITY FOR SUBSIDIES IN 2026

income limits for subsidies are adjusted annually, tied to the federal poverty guidelines which change with inflation. recently, the “inflation reduction act” removed the income cap for premium credits, allowing even higher earners to avoid paying more than 8.5% of their income on insurance. this expanded eligibility has opened the door for many middle-class families to access aca health plans affordably. we recognize this as a critical expansion of the safety net.

Tips:

use online income calculators on healthcare.gov to estimate your subsidy eligibility before browsing plans to see accurate prices.

to qualify, you must estimate your income for the coverage year, including wages, self-employment income, and other taxable sources. accurately predicting income can be challenging for freelancers, so we suggest engaging in conservative estimates. remember, falling below 100% of the poverty level may disqualify you in non-medicaid expansion states. checking the current year’s specific thresholds is essential for accurate planning.

HOW TO ENROLL IN AN ACA HEALTH PLAN

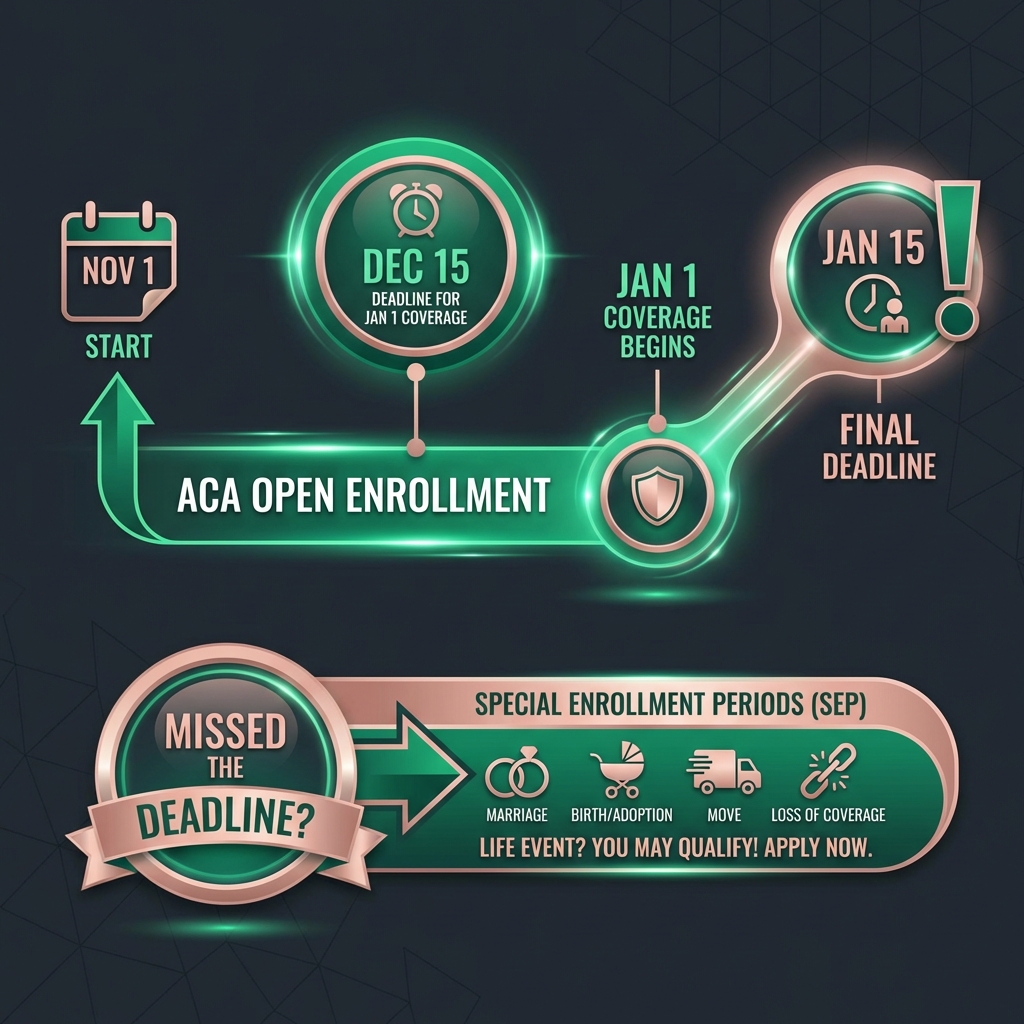

WHEN IS THE OPEN ENROLLMENT PERIOD?

open enrollment is the designated yearly window when anyone can sign up for or change their aca health plans for the upcoming year. typically running from november 1st to january 15th, this period is critical for securing continuous coverage. missing this window means you usually have to wait a full year to get insured, unless you qualify for an exception. we emphasize marking these dates on your calendar as non-negotiable deadlines.

Warning:

missing the open enrollment deadline typically leaves you locked out of aca health plans for the entire year unless you experience a qualifying life event.

enrollment deadlines vary slightly by state if your state runs its own exchange, but generally, enrolling by december 15th ensures coverage starts on january 1st. plans selected in january typically start on february 1st, potentially leaving a gap in coverage. we believe early enrollment is the best strategy to avoid administrative delays. procrastination can result in weeks without protection.

SPECIAL ENROLLMENT PERIODS: BUYING COVERAGE AFTER A LIFE EVENT

life is unpredictable, and qualifying life events trigger a special enrollment period allowing you to sign up outside standard dates. common events include getting married, having a baby, losing other health coverage, or moving to a new zip code. generally, you have 60 days from the date of the event to select a new plan. we stress acting quickly, as documentation is often required to prove eligibility for the special period.

WHAT DOCUMENTS DO I NEED?

you will usually need proof of your life event, such as a marriage certificate or letter of coverage loss, to confirm eligibility for a special enrollment period.

simply quitting coverage voluntarily or failing to pay premiums does not qualify you for a special enrollment period. the system is designed to accommodate genuine life transitions rather than casual switching. ensure you have documents like marriage certificates or loss-of-coverage letters ready to upload. we see this flexibility as a vital component preventing gaps in care during major life changes.

A STEP-BY-STEP GUIDE TO THE HEALTH INSURANCE MARKETPLACE

getting started is as simple as visiting healthcare.gov or your state’s specific exchange website. the first step is to create an account and fill out a basic application with your household and income information. the system will instantly determine your eligibility for subsidies and medicaid. we find the interface user-friendly, allowing you to filter plans by premiums, deductibles, and doctors.

once you view your results, you can compare aca health plans side-by-side to see the details of coverage. pay close attention to the “summary of benefits” document for each plan, which outlines specific copays for services you use often. after selecting a plan, you must pay your first premium directly to the insurance company to activate the policy. we encourage double-checking that your preferred doctors are in-network before hitting the submit button.

You Might Also Like

PROS AND CONS OF ACA HEALTH PLANS

ADVANTAGES: COMPREHENSIVE COVERAGE AND SUBSIDY AVAILABILITY

the biggest advantage of aca health plans is the guarantee of comprehensive coverage without fear of denial. knowing that your insurance includes maternity, mental health, and unlimited hospitalization provides immense peace of mind. furthermore, subsidies make these comprehensive plans financially viable for millions who would otherwise be priced out. we regard the combination of access and affordability as the system’s greatest success.

Note:

utilizing free preventive care services is one of the smartest ways to maximize value and stay healthy on your new plan.

preventive care at no cost is another huge plus, encouraging people to stay healthy rather than just treating sickness. this proactive approach can catch conditions early when they are cheaper and easier to treat. additionally, the ability to keep children on plans until age 26 supports young adults launching their careers. we see these structural benefits as creating a healthier society overall.

DISADVANTAGES: NETWORK RESTRICTIONS AND POTENTIAL COSTS FOR HIGH EARNERS

on the downside, many aca health plans utilize narrower provider networks, often hmos or epos, to keep costs down. this means you generally have no coverage for out-of-network care except in emergencies, limiting your choice of doctors. “The Commonwealth Fund” notes that finding specialists in rural areas can sometimes be challenging within exchange networks. we advise verifying networks carefully if you have established relationships with specific physicians.

Remember:

check the provider network carefully; seeing an out-of-network doctor can leave you responsible for the entire bill.

for individuals with higher incomes who do not qualify for substantial subsidies, the premiums can still feel steep. while the expanded subsidies have helped, those on the borderline can face a significant “cliff” in costs. deductibles on bronze and silver plans can also be high without cost-sharing reductions. we acknowledge that for unsubsidized healthy people, the value proposition requires careful math.

COMMON CONCERNS ABOUT ACA COVERAGE

FREELANCERS AND SELF-EMPLOYED INDIVIDUALS

freelancers and gig workers often worry about proving income or finding flexible coverage. aca health plans are actually ideal for self-employed individuals because eligibility is based on projected net income. expenses listed on your schedule c tax form can lower your income, potentially increasing your subsidy amount. we recommend keeping detailed records to facilitate accurate income estimation.

variable income is a common reality, and the marketplace allows adjustments throughout the year. if your business takes off or slows down, you can update your application to adjust your monthly premium credit immediately. this responsiveness protects you from overpaying or owing huge sums at tax time. we see this flexibility as crucial for the modern gig economy.

TAX PENALTIES AND MANDATES

historically, the “individual mandate” penalized people for not having insurance, but the federal financial penalty was reduced to zero in 2019. this means you will not owe a federal tax fee for being uninsured, although some states have enacted their own mandates. “California, Massachusetts, and New Jersey”, for example, still impose state-level penalties. we advise checking your local laws to ensure compliance and avoid unexpected fines.

coverage under an aca plan ensures you meet any state-level requirements for minimum essential coverage to avoid these state penalties. beyond avoiding fines, maintaining continuous coverage protects you from waiting periods or coverage gaps in the future. we believe the primary motivation should always remain health protection rather than tax avoidance.

DENTAL AND VISION OPTIONS

while pediatric dental and vision are essential health benefits, adult coverage is not mandated. some marketplace plans bundle these services, while others require purchasing standalone dental or vision policies. usually, standalone plans on the exchange act similarly to medical plans regarding enrollment windows. we suggest evaluating if a separate plan or a bundled option offers better value for your specific needs.

costs for adult dental and vision are not typically subsidized by premium tax credits in the same way medical premiums are. however, having coverage can significantly reduce the costs of exams, cleanings, and glasses. ignoring oral and eye health can lead to broader systemic health issues down the line. we encourage budget-conscious consumers to at least consider preventive dental plans.

CONCLUSION

navigating the landscape of aca health plans can initially seem overwhelming, but the protections and financial assistance they offer are undeniable. we have explored how these plans guarantee essential benefits, safeguard those with pre-existing conditions, and provide a tiered system to match different budgets. from understanding the metal levels to maximizing subsidies, you now have the tools to make a confident choice. securing the right coverage is a pivotal step in protecting your health and financial future.

remember that the marketplace is dynamic, with plans and prices changing annually, so active re-evaluation each open enrollment is key. whether you choose a bronze plan for catastrophic safety or a gold plan for ongoing care, the act ensures a standard of quality you can rely on. we encourage you to log in, compare your options, and enroll before the deadline passes. take charge of your healthcare journey today.

medical disclaimer: the information provided in this article is for educational and informational purposes only and does not constitute professional financial, legal, or medical advice. health insurance policies, laws, and regulations such as the affordable care act are subject to change. individual eligibility for coverage and subsidies depends on specific personal circumstances. always consult with a licensed insurance agent, tax professional, or healthcare provider before making decisions regarding your health coverage or medical care. we do not guarantee the accuracy or completeness of the information regarding specific plan benefits or costs.