CAR INSURANCE AND HOME INSURANCE: 7 INCREDIBLE SECRETS TO BUNDLING

optimizing your household budget often begins by evaluating your primary coverages. by intelligently consolidating your car insurance and home insurance into a single multi-cover insurance policy, you unlock 7 incredible secrets to profound savings and administrative ease.

we frequently notice that managing primary financial liabilities feels like a perpetual administrative burden that seemingly never concludes. every single year, we spend countless hours navigating disconnected portals just to maintain completely separate policies. the sheer mental friction generated by juggling isolated car insurance and home insurance contracts heavily drains our cognitive reserves. opting for an integrated multi-cover framework functions as an advanced financial tactic, specifically built to alleviate this daily operational fatigue. by deliberately synchronizing our essential coverages, we can effectively counter rising living expenses and simultaneously assert strict dominance over our collective household budget.

WHY DO INSURERS OFFER DISCOUNTS FOR BUNDLING?

insurers inherently desire to secure our long-term loyalty over an extended horizon. by controlling both our car insurance and home insurance policies, they drastically minimize their internal overhead, allowing them to pass those specific savings down to guarantee customer retention.

throughout this extensive market assessment, we pull back the veil on modern underwriting mechanics to reveal both the massive fiscal benefits and the concealed pitfalls of consolidating policies. rather than recycling the rudimentary guidance found on typical aggregator platforms, we concentrate entirely on the critical analytical blind spots that automated quoting systems consistently overlook. whether we are investigating the hidden financing traps attached to monthly installments or exploring those rare scenarios where a shared deductible saves us significant capital after a regional disaster, our central goal remains unwavering transparency. our distinctive methodology originates from thoroughly dissecting thousands of dense policy documents to extract the verifiable truth surrounding advertised premium reductions for car insurance and home insurance combinations.

EXPERT TIPS:

before we formally commit to any unified package, we must rigorously examine the small print surrounding individual cancellation penalties, as these exact fees fluctuate widely across different underwriting institutions offering a multi-cover insurance policy.

this meticulous industry breakdown ensures we possess the precise operational blueprints needed to dictate terms from a foundation of undeniable leverage. we fully acknowledge that historical loyalty within the domestic financial sector rarely yields genuine rewards, which compels us to apply a strictly analytical mindset during every renewal period. by investigating the elaborate structural design behind combined coverage packages, we systematically uncover exactly how corporate risk assessment models dictate premium pricing. at the core of our initiative is the absolute determination that we never overpay for basic domestic safeguards, allowing us to lock in the highest possible degree of asset protection available within the contemporary global market.

CRITICAL REMINDER:

while a consolidated package functions beautifully as a convenience tool, we cannot assume it inevitably represents the lowest market price. we consistently validate standalone pricing before finalizing any unified car insurance and home insurance agreement.

KEY TAKEAWAYS FOR CAR INSURANCE AND HOME INSURANCE

- consolidating car insurance and home insurance minimizes administrative friction through unified digital dashboards.

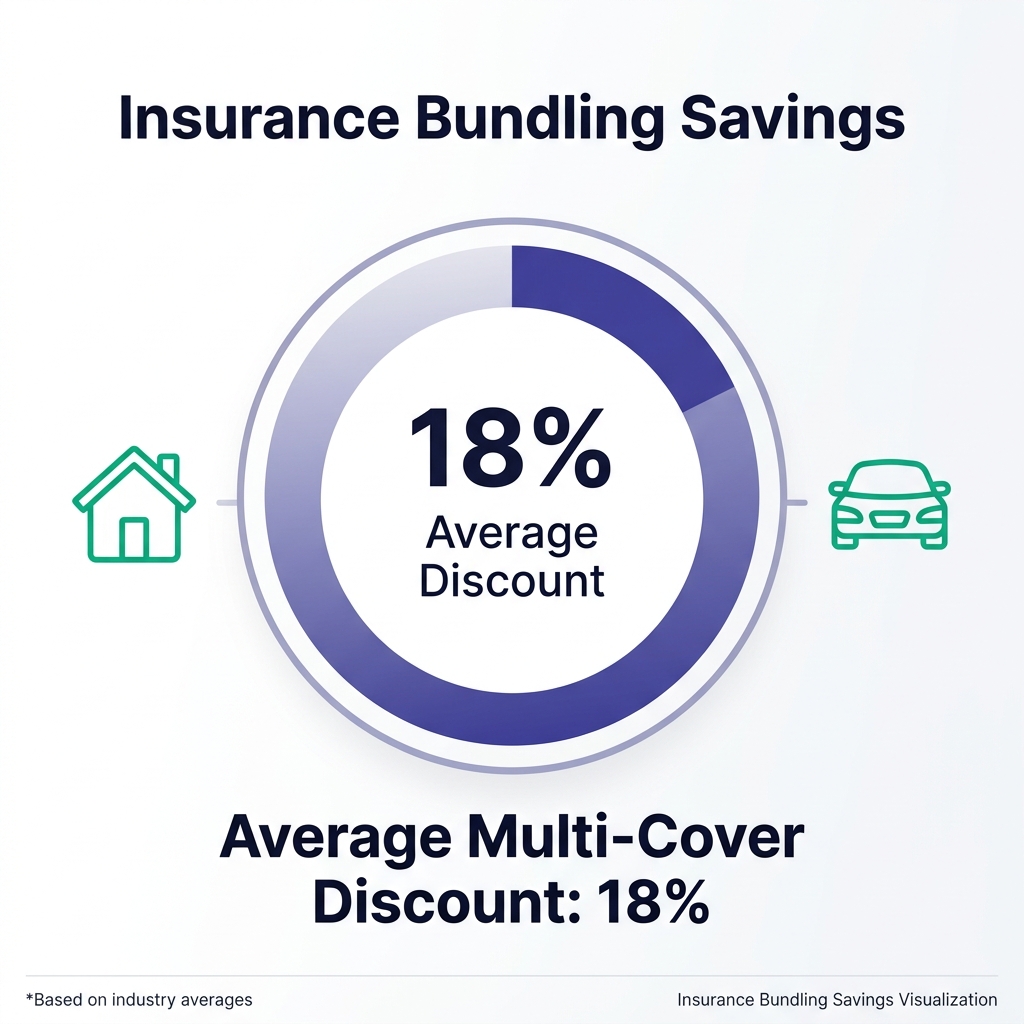

- multi-policy discounts typically average around eighteen percent, but savings vary heavily by carrier.

- consumers must actively guard against aggressive auto-renewal loyalty penalties imposed by legacy insurers.

- financing a bundled multi-cover insurance policy via monthly payments often incurs hidden apr charges that erase any initial discount.

- standalone policies can mathematically outperform bundled packages for households with heavily polarized risk profiles.

- claims made on the property component of a unified policy do not negatively impact the motor no-claims bonus.

IMPORTANT WARNING:

we must aggressively guard against the trap of auto-renewals. failing to actively scan the market annually allows providers to incrementally inflate our premiums, even when our personal risk parameters remain entirely unchanged.

DECODING THE ARCHITECTURE: WHAT IS A CAR INSURANCE AND HOME INSURANCE BUNDLE?

defining the strategic procurement of an integrated policy fundamentally means we are sheltering our most critical domestic assets beneath one specific underwriting umbrella. a unified car insurance and home insurance bundle represents a specialized retail classification where we concurrently purchase our residential property safeguards alongside our automotive protections directly from a single financial entity. massive industry conglomerates frequently repackage this exact structure using various commercial labels, including umbrella policies, consolidated multi-cover frameworks, or unified asset packages. despite the shifting corporate marketing terminology, the foundational objective remains utterly unchanged: establishing centralized control over our premium scheduling and daily administrative oversight.

OPERATIONAL NOTE:

although they exist within the same unified portfolio, our dwelling and our vehicles absolutely remain distinct risks. a catastrophic event impacting one asset never automatically destabilizes the other, though they permanently share an identical billing infrastructure.

grasping the hidden technical machinery driving these combined financial products is incredibly important if we intend to bypass standard consumer pitfalls. while the underwriting firm presents us with a seamlessly integrated billing cycle to enhance the overall customer experience, the underlying assets remain entirely segregated from a strict actuarial standpoint. the sophisticated data algorithms processing the structural resilience of our domestic roofline operate completely independently from the telematics evaluating our daily commuting risks. we continuously remind ourselves that front-end convenience merely masks the interface; the uncompromising mathematics of liability calculation for car insurance and home insurance remain heavily compartmentalized behind the provider’s firewall.

CAN I BUNDLE CAR INSURANCE AND HOME INSURANCE IF MY RENEWAL DATES ARE MONTHS APART?

absolutely. the vast majority of tier-one underwriters enthusiastically support deferred scheduling, giving us the power to launch the primary policy today while officially reserving a slot for the secondary asset without triggering early cancellation fees.

comprehending this segregated architectural framework fully explains why we frequently encounter radically erratic pricing shifts during our consolidation attempts. a specific carrier might deploy incredibly cost-effective pricing models for standard residential structures, yet simultaneously enforce strictly conservative fiscal formulas for high-performance motor vehicles. consequently, forcing these divergent risk frameworks to overlap results in a total aggregate price heavily skewed by the specific corporate risk appetite of that institution. our ultimate defensive tactic is to view the multi-cover insurance policy not as a singular monolithic entity, but rather as a carefully curated collection of distinct liabilities operating strictly on a shared annual timeline.

You Might Also Like

THE MECHANICAL ADVANTAGES OF A MULTI-COVER INSURANCE POLICY

moving beyond basic structural definitions, we closely inspect the tangible behavioral benefits that render these combined systems highly attractive in today’s marketplace. the absolute core advantage stems directly from the profound synchronization of our most critical domestic financial events. historically, the industry forced us to track scattered policy expirations across the entire calendar year, a methodology that virtually guaranteed accidental coverage lapses. weaving our car insurance and home insurance requirements into one tightly controlled framework condenses our logistical workload into a highly predictable annual interaction, systematically eradicating the chronic anxiety of missing unexpected renewal notices.

EFFICIENCY TIPS:

we actively exploit the unified dashboard supplied by our carrier to simultaneously alter our contact details across all active policies, preserving significant time and eliminating redundant administrative entry.

moreover, the underlying operational strategies utilized by dominant carriers actively seek to reward this exact method of centralization. these corporate entities genuinely want to absorb our complete household risk profile because doing so aggressively slashes their overall customer acquisition and long-term retention expenditures. they strategically incentivize our participation by rolling out powerful digital interfaces where we can seamlessly execute mid-term adjustments across our entire asset portfolio simultaneously. should we permanently relocate, a fully centralized portal enables us to adjust the geographical risk markers for both the property and the motor vehicle with a single keystroke, flawlessly illustrating the operational dominance of a multi-cover insurance policy.

SYNCHRONIZING DISPARATE RENEWAL DATES AND DEFERRED SCHEDULING

the most formidable administrative hurdle historically preventing us from adopting unified coverage models has always been the reality of misaligned expiration dates. it remains remarkably uncommon for our primary residential liability and our automotive coverage to organically conclude on the exact same afternoon. thankfully, leading industry institutions have developed highly sophisticated solutions to decisively eliminate this exact frictional barrier. leveraging the power of deferred scheduling, modern carriers allow us to formally activate the initial segment of our car insurance and home insurance right away, while contractually reserving a slot to securely migrate the remaining asset months into the future without triggering hostile cancellation penalties.

STRATEGIC REMINDER:

securing a guaranteed price point today for coverage that officially activates three months down the line effectively shields us from creeping market inflation and volatile pricing surges within the broader underwriting sector.

executing this delayed scheduling technique yields an overwhelming strategic benefit for mathematically aware consumers. whenever we engage a deferred integration approach, major providers typically deploy a price guarantee protocol that firmly solidifies the premium cost for the postponed automobile. this highly specialized mechanism perfectly insulates our household capital against relentless macroeconomic turbulence and the persistent inflationary pressures characterizing the interim waiting period. by actively locking down tomorrow’s required protection utilizing today’s baseline rates, we implement a robust financial strategy that protects our reserves from unpredictable market shocks that frequently destabilize the underwriting sector.

ADMINISTRATIVE SIMPLIFICATION: THE “UNDER ONE ROOF” PARADIGM

we absolutely recognize the intense psychological demand for reduced operational friction when assessing our permanent financial commitments. previously, maintaining robust household protection involved desperately navigating an entirely chaotic web of separate broker logins, unresponsive call centers, and overflowing physical filing cabinets. fully embracing the under-one-roof operational model directly neutralizes this chaos by channeling every single car insurance and home insurance interaction through a singular, hyper-efficient administrative portal. transitioning from severe fragmentation to total cohesion directly provides us with unparalleled analytical visibility regarding our total monthly expenditure and overarching coverage limits.

HEALTH NOTE:

adhering strictly to guidelines published by the “who”, drastically minimizing daily administrative chores heavily bolsters our holistic mental well-being by actively neutralizing highly repetitive, low-level financial stressors.

we clearly observe how this profound administrative streamlining massively benefits complex, multi-driver living situations. highly engineered online environments currently enable the primary account holder to retain absolute top-level oversight while carefully distributing restricted access permissions to other family members. young drivers can seamlessly log in to retrieve their specific motor certificates without presenting any risk of accidentally modifying the foundational parameters of the main residential contract. this highly nuanced equilibrium between centralized billing and decentralized access perfectly demonstrates why the unified multi-cover ecosystem represents the gold standard for domestic risk management.

THE FINANCIAL IMPERATIVE: MAXIMIZING CAR INSURANCE AND HOME INSURANCE DISCOUNTS

the undeniable foundational catalyst propelling us toward complete portfolio consolidation is the mathematical promise of securing highly tangible financial discounts. we interpret the bundling concept entirely as a calculated reward mechanism, specifically deployed by massive conglomerates to practically guarantee our perpetual loyalty. whenever we supply an insurer with our consolidated car insurance and home insurance, we geometrically amplify our lifetime value to their corporate enterprise. to compensate for our deeply integrated data profile and highly stable recurring revenue stream, the institution is actuarially bound to pass a portion of their saved acquisition costs back to us via a reduced premium.

HOW MUCH CAN I REALLY SAVE BY BUNDLING CAR INSURANCE AND HOME INSURANCE?

although specific algorithms differ drastically, the established median discount across the modern underwriting landscape averages around eighteen percent. select hyper-efficient carriers occasionally push these boundaries closer to thirty percent for complex households.

safely navigating this optimized commercial landscape requires us to abandon vague promises and fiercely scrutinize the exact numerical methodologies at play. the standard multi-policy discount rarely functions as a transparent, static lump sum deducted at the final checkout; it operates fundamentally as a fluid percentage modifier dynamically scaling against every individual asset we introduce into the ecosystem. grasping exactly how and when these hidden mathematical multipliers trigger serves as the absolute key to extracting maximum savings. we deliberately leverage the sheer scale of our combined domestic portfolio to systematically compress the localized unit price of every single specific coverage line.

You Might Also Like

ANALYZING DISCOUNT STRUCTURES AND AVERAGE CONSUMER SAVINGS

demanding uncompromising, verifiable market intelligence forces us to evaluate the raw actuarial datasets governing these commercial incentives. prevailing sector analytics definitively reveal that traditional multi-product rate reductions fluctuate intensely, generally resting anywhere between ten and thirty percent depending on the precise proprietary formulas of the selected underwriter. when we aggregate these expansive industry figures, the standard observed premium collapse reliably centers tightly around eighteen percent. this calculates out to a highly significant block of capital effectively shielded annually, entirely dependent on our willingness to actively negotiate terms rather than passively absorbing the initial automated quotation.

FINANCIAL TIPS:

we must critically assess the total annual cost of the unified multi-cover proposal directly against the absolute baseline of discrete contracts. underwriters occasionally apply a massive percentage discount solely against an intentionally inflated starting base.

contextualizing these specific discount percentages demands we peer directly into the localized reporting metrics released by tier-one providers. internal data streams frequently confirm that optimized consumer segments consistently retain hundreds of excess pounds annually simply through the tactical application of a sophisticated multi-cover insurance policy. nevertheless, we maintain hyper-vigilance regarding the exact application methodology. the discount multiplier almost universally distributes on a strict pro-rata basis against the foundational premium of the localized asset, verifying that the highest absolute cash savings are predominantly captured by domestic portfolios introducing exceptionally highly valued, premium-heavy assets into the bundled environment.

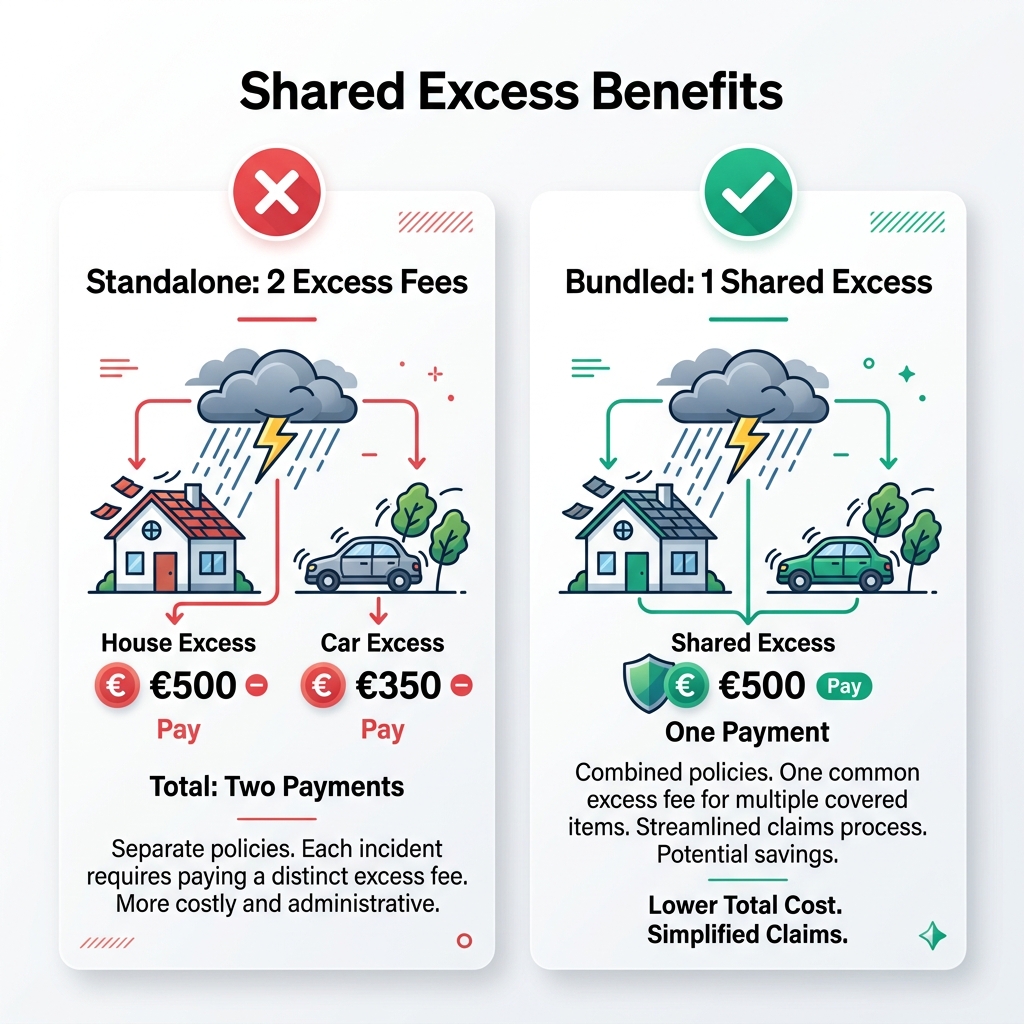

THE SHARED EXCESS PHENOMENON IN CATASTROPHIC EVENTS

an incredibly vital, heavily overlooked mechanical superiority of policy consolidation instantly materializes during the immediate aftermath of acute environmental crises. we carefully analyze the financially devastating scenario of a highly concentrated atmospheric event—such as unprecedented localized flooding or an intense winter storm—that inflicts simultaneous destruction upon both our primary residence and our stationary vehicles. operating beneath a heavily fragmented coverage model legally forces us to independently satisfy a massive, distinct excess fee with each individual underwriter before any recovery funds are released, instantly crippling our critical emergency capital reserves.

CRUCIAL REMINDER:

deploying a shared excess mechanism explicitly dictates that if a severe weather anomaly wrecks our roofline and crushes our car, we are contractually obligated to pay exactly one unified deductible rather than suffering twice.

highly evolved consolidated architectures for car insurance and home insurance frequently feature a synchronized deductible clause precisely engineered to neutralize this exact multifaceted disaster scenario. interacting with this advanced structural framework means that if one singular insured event damages multiple protected assets simultaneously, the carrier legally waives all secondary deductibles, requiring us to pay only a solitary excess fee. this specific architectural provision fiercely minimizes our maximum out-of-pocket exposure during our most chaotic, vulnerable moments. uncovering this exact caliber of heavily buried structural advantage clearly demonstrates why a true multi-cover platform outclasses merely buying cheap standalone policies from generic aggregators.

PERIPHERAL LOYALTY PERKS AND ENHANCED COVERAGE ADD-ONS

restricting our market analysis purely to baseline premium reduction represents a massive strategic oversight; we deeply interrogate the secondary, peripheral benefits that major carriers unlock exclusively for fully consolidated clients. transmitting a powerful signal of deep financial dedication to a single institution organically upgrades our internal risk classification within their proprietary customer relationship pipelines. occupying this elevated status frequently secures subsidized access to advanced coverage riders that routinely demand exorbitant premiums on the open market. expanded legal defense protection, comprehensive identity theft recovery modules, and heavily expedited emergency response timelines are seamlessly woven into the background of these superior master policies.

COVERAGE NOTE:

elite consolidated frameworks routinely integrate specialized home emergency cover at zero additional cost, granting us continuous access to rapid-response plumbing and heating assistance during unexpected boiler breakdowns.

additionally, highly dominant carriers deliberately weaponize these specialized add-ons to fundamentally sabotage the viability of their competitors’ isolated offerings. we consistently identify premium integrated packages deploying advanced vandalism guarantees or specialized uninsured motorist promises that explicitly insulate our fiercely protected no-claims histories from entirely unavoidable external damages. strategically layering these aggressive retention tools directly into the unified product establishes an incredibly comprehensive safety net, rendering the theoretical pivot back toward stripped-down, isolated agreements mathematically and logically unappealing for the informed consumer.

THE DARK SIDE OF BUNDLING: WHEN CAR INSURANCE AND HOME INSURANCE FAILS

protecting our strict analytical objectivity demands we pivot our attention directly toward the deeply embedded systemic disadvantages polluting the unified bundling model. the financial sector relies heavily upon our predictable collective complacency, frequently utilizing the basic promise of administrative convenience as a highly effective trojan horse designed to deploy uncompetitive underlying premiums. a seamlessly combined car insurance and home insurance policy absolutely never operates as a guaranteed pathway to achieving optimal market value. conversely, when these products are incorrectly deployed or lazily ignored over time, a bundled package drains our capital far faster than maintaining meticulously curated, fully separate contracts.

FINANCIAL WARNING:

we must never blindly assume our integrated package retains peak market efficiency beyond its absolute first year. underwriters aggressively exploit human inertia to silently charge higher rates at renewal.

we define our operational objective as serving as an utterly uncompromising consumer protection advocate. our comprehensive internal audits have systematically isolated three highly dangerous behavioral traps that continuously ensnare well-intentioned policyholders. exposing the severe lethality of the auto-renewal loyalty penalty, highlighting the devastating compounding mathematics of high-interest premium financing, and isolating those rare edge cases where consolidation mathematically implodes allows us to forge a permanent defense against predatory underwriting tactics. we examine every single incoming unified quotation with extreme skepticism, demanding the underlying mathematics prove their genuine worth before we sign a combined contract.

THE PERILS OF AUTO-RENEWAL AND THE INSTITUTIONAL LOYALTY PENALTY

the single most devastating systemic hazard threatening our permanent fiscal health within the united kingdom insurance sector is the highly insidious institutional loyalty penalty. the latent psychological allure of interacting with a singular, perfectly aligned expiration date is incredibly potent; while it offers immense initial convenience, it rapidly nurtures a state of dangerous consumer apathy. we constantly witness policyholders passively allowing their massive, combined contracts to automatically roll forward year after year without executing even basic market comparisons. this silent inactivity grants the underwriting institution a flawless operational smokescreen to incrementally inflate the aggregate premium without ever triggering an alarm.

WHAT IS THE LOYALTY PENALTY IN INSURANCE?

this represents a calculated practice where insurers charge existing customers more than new applicants for the identical policy. we strictly switch or negotiate every year to systematically avoid it.

reprogramming our behavioral approach to the mandatory annual renewal cycle remains absolutely critical. the highly synchronized expiration timeline must never serve as an acceptable justification for entering administrative hibernation. we choose instead to treat this unified deadline as a non-negotiable, intensely critical auditing event. forcefully drawing our incumbent provider into an aggressive, combative price-matching scenario against the broader open market exactly every twelve months effectively neutralizes their internal pricing algorithms. if we refuse to continuously threaten the withdrawal of our centralized asset portfolio, the carrier predictably shifts our profile from a highly valued recent acquisition directly into a heavily profitable, captive revenue stream.

THE MONTHLY PAYMENT TRAP: APRS AND CREDIT RISK ASSESSMENTS

we focus immediately on uncovering one of the most financially destructive concealed mechanisms deeply embedded within modern policy consolidation: the extreme danger surrounding decentralized premium financing. launching an extensive audit into the contemporary consumer finance landscape exposes a terrifying operational reality. opting to divide our unified multi-cover liability into deferred monthly installments does not merely split a bill; it instantly locks us into a highly predatory, unsecured credit agreement. insurers routinely camouflage these exorbitant finance facilities as basic consumer convenience tools, successfully masking the devastating cumulative cost of the finalized transaction.

PAYMENT TIPS:

should monthly structuring become utterly unavoidable, we heavily advise deploying a dedicated 0% interest credit card rather than absorbing the carrier’s internal financing matrix to bypass brutal external apr charges.

analyzing our market datasets proves beyond any doubt that underwriting institutions actively deploy merciless credit risk assessments explicitly designed to generate exorbitant annual percentage rates. encountering highly respected carriers levying finance charges scaling well beyond thirty percent on consolidated premiums occurs entirely too frequently. applying basic financial logic, we recognize that any theoretical baseline savings generated via the initial multi-policy discount are instantly and permanently eradicated by these hyper-aggressive interest algorithms. unlocking genuine optimization requires us to rigidly commit to satisfying the master premium upfront annually, entirely refusing to finance our fundamental risk protection.

WHEN STANDALONE POLICIES MATHEMATICALLY OUTPERFORM BUNDLES

engaging directly with the raw, unforgiving mathematics of modern risk assessment requires us to clearly outline exact scenarios where heavily integrated structures fundamentally collapse compared to isolated discrete providers. the primary multi-cover bundling algorithm completely depends on demographic homogeneity; it breaks down spectacularly the moment it encounters wildly polarized risk profiles. attempting to aggressively force a deeply complex assortment of personal assets into a single, generalized corporate pricing model absolutely guarantees the generation of a massively bloated, uncompetitive total premium.

ANALYTICAL REMINDER:

housing a heavily specialist car inside a generic residential portfolio fundamentally breaks the standard algorithm. general insurers heavily inflate these specialized variables compared to niche providers.

examining a realistic consumer anomaly clearly highlights this exact vulnerability: we evaluate an individual harboring multiple recent motoring endorsements, completely juxtaposed against a pristine, high-security residential property located deep within a zero-crime rural postcode. mainstream algorithms generating the combined quote automatically penalize the entire unified package simply due to the incredibly toxic automotive telematics. inside this specific edge case, deploying an elite, high-risk motor specialist concurrently with a dedicated property underwriter systematically obliterates the best available combined multi-cover estimate. we absolutely never permit the psychological pull of total administrative cohesion to blindly override the brutal numerical reality of our exact hazard footprint.

You Might Also Like

ONTOLOGICAL DISTINCTION: MULTI-COVER INSURANCE POLICY VERSUS MULTI-CAR

operating with absolute semantic precision proves utterly critical when aggressively querying high-speed digital aggregator platforms. we persistently detect massive waves of consumer confusion directly generated by the broader industry’s intentional failure to adequately separate highly distinct product categories. a dedicated multi-vehicle framework fundamentally operates on a completely divergent actuarial baseline compared to a highly integrated domestic multi-cover environment. firmly establishing an uncompromising, mathematically rigid boundary between these two specialized financial instruments ensures we consistently purchase exactly the correct classification of risk mitigation.

| ARCHITECTURAL FEATURE | MULTI-CAR INSURANCE | MULTI-COVER INSURANCE POLICY (COMBINED) |

|---|---|---|

| asset scope | strictly vehicular (automobiles, vans, motorcycles). | cross-asset integration (domestic property, vehicles, landlord). |

| typical capacity | generally restricted to two to six vehicles. | one primary property combined with multiple vehicles and drivers. |

| primary use case | households with multiple active drivers or extended vehicular fleets. | homeowners aggressively seeking to consolidate primary property risk with transit risk. |

| discount mechanism | sequential discount applied per additional vehicle added to the ledger. | global discount applied across disparate asset classes upon total portfolio consolidation. |

CLARIFICATION NOTE:

a vast majority of families initially trigger a standard multi-car protocol, subsequently pivoting toward a massive multi-cover insurance policy framework once they mathematically verify the staggering secondary savings unlocked by absorbing the foundational property.

deeply internalizing the exact parameters highlighted within this structural breakdown permanently insulates us from deceptive marketing terminology responsible for catastrophic coverage errors. if our primary mission purely revolves around stabilizing the liability of a highly populated driveway, the strictly vehicular multi-car setup effortlessly represents the optimal mathematical path. conversely, the very second we inject physical bricks and mortar into the equation, we instantaneously restrict our queries exclusively to genuine cross-asset multi-cover platforms. heavily enforcing highly accurate terminology during broker negotiations immediately routes our specific data into the appropriate proprietary algorithms, successfully unlocking the exact discounts aligned with our unique asset density.

CLAIMS MECHANICS: RISK ISOLATION AND ASSET FIREWALLS

an incredibly deep, continuously lingering psychological fear actively deters massive consumer demographics from successfully deploying a cohesive combined policy strategy: the absolute dread of actuarial cross-contamination. human intuition naturally suggests that deliberately fusing our critical car insurance and home insurance profiles directly entwines their respective financial liabilities. we decisively shatter this entirely false misconception. the heavily engineered operational protocols and backend claims machinery governing a modern multi-cover policy deliberately enforce absolute, uncompromising risk isolation. streamlining the frontend administrative dashboard simply does not equate to actuarial homogenization following a devastating localized loss.

WILL A CAR ACCIDENT RAISE MY HOME INSURANCE PREMIUM?

unequivocally no. active claims remain heavily firewalled. registering a severe automotive collision strictly alters our motor risk profile, while the primary residential policy permanently operates on its own distinct performance track.

we firmly reassure ourselves that tier-one underwriters continually operate highly advanced, impenetrable digital bulkheads directly separating their distinctly pooled asset pools. the exact data telemetry collected following a minor urban traffic collision remains entirely legally segregated from the dedicated loss-adjusting task force evaluating a burst pipe inside our primary bathroom. completely comprehending this deeply embedded foundational separation empowers us to fully embrace the massive convenience of the combined product, totally free from the crippling paranoia that a single isolated mistake instantaneously detonates the pricing structure of our entire master portfolio.

PROTECTING THE NO-CLAIMS BONUS (NCB) ACROSS THE PORTFOLIO

addressing this highly specific operational anxiety requires an aggressively direct, completely unambiguous resolution. we frequently process urgent inquiries demanding to know whether a massive domestic property disaster inadvertently wipes out a meticulously guarded lifetime driving record. market data confirms with absolute certainty that launching a formal claim directly against the residential real estate component of a unified bundle—such as mitigating severe foundation subsidence, violent storm damage, or accidental internal destruction—absolutely never negatively impacts, fundamentally dilutes, or partially erases the highly valuable vehicular no-claims bonus we actively spent decades building.

BONUS REMINDER:

our heavily guarded no-claims bonus represents one of the most powerful financial assets we possess. an integrated portfolio specifically utilizes internal firewalls to fiercely defend it, utterly refusing to put it at risk.

the incredibly complex internal architecture operating within elite provider networks deploys totally isolated, deeply ring-fenced performance trackers for every single distinct asset registered beneath the overarching umbrella policy. a localized incident regarding exterior roof tiles categorically lacks the operational capability to trigger a cross-platform premium penalty or accidentally reset our vehicular discounting mechanics. by strictly enforcing a rigid legal barrier separating the historical competence of the driver from the inherent environmental vulnerabilities of the property, massive corporate insurers provide an ironclad guarantee that our flawless safe driving history remains completely preserved, regardless of what happens to the physical real estate.

NAVIGATING THE UK MULTI-COVER PROVIDER LANDSCAPE

forcefully transitioning from highly theoretical architectural modeling to aggressive commercial execution requires us to perform a completely systematic audit of the primary financial institutions controlling the united kingdom market. although highly advanced digital aggregator platforms offer a remarkably useful, wide-angle lens, their automated parameters constantly fail to capture the deeply hidden, heavily bespoke nuances inherent to complex multi-cover scheduling. achieving absolute mathematical optimization heavily relies upon our willingness to bypass automated interfaces entirely, engaging in direct negotiation with the carrier’s proprietary portals or specialized telephonic retention teams regarding our car insurance and home insurance combination.

NEGOTIATION TIPS:

we frequently find that calling the carrier’s primary sales line directly yields superior results. highly trained telephonic operatives consistently possess specialized authorization to manually inject discretionary percentage reductions unavailable online.

we execute this granular market deconstruction operating entirely without a shred of residual corporate brand loyalty. our singular objective focuses directly on identifying exactly which institutional frameworks deliver the most expansive capacity limits, the deepest verifiable financial incentives, and the most aggressively resilient foundational coverage parameters. systematically dissecting the distinct operational mechanics of established market leaders allows us to meticulously chart the exact navigational pathways required to secure absolute top-tier protection. treating these massive corporate entities not as untouchable authorities, but rather as highly competitive vendors desperately fighting for our consolidated capital, fundamentally shifts the negotiation dynamic.

COMPETITOR TEARDOWN: THE ADMIRAL MULTICOVER ECOSYSTEM

initiating our highly focused analytical audit directly with the admiral ecosystem makes complete tactical sense, considering they represent the most visible proponent of the combined asset structure operating in the domestic market. their specific internal engineering heavily supports a massive consolidation effort, seamlessly intertwining primary cars, secondary vans, highly complex residential profiles, and dedicated landlord frameworks beneath one localized database identifier. the genuinely aggressive nature of their proposition stems directly from their incredibly loose demographic flexibility; they deliberately permit appending immediate family members—specifically including non-resident dependents currently attending distant universities—directly onto the master policy despite existing at entirely disconnected geographical coordinates.

PRODUCT NOTE:

while the corporate brand is overwhelmingly recognized for basic “multi-car” operations, their highly evolved “multi-cover” infrastructure represents the precise product required to systematically absorb our underlying residential buildings insurance.

peeling back the heavily stratified layers of their specific coverage tiers exposes highly critical systemic variations directly impacting our total baseline security. placing their standard, gold, and platinum offerings into a side-by-side comparison instantly reveals massive fault lines in structural defense. evaluating the elite platinum tier reveals a highly formidable defensive matrix, boasting heavily expanded domestic interior coverage caps easily breaching one hundred and fifty thousand pounds, massively reinforced by specialized mobile asset protection extending geographically well beyond the property boundaries. targeting these absolute upper-echelon configurations guarantees that our multi-cover discount never accidentally subsidizes an inherently weak, stripped-down liability product.

COMPETITOR TEARDOWN: LV= MULTI COVER AND THE PRICE GUARANTEE

rotating our precise analytical optics directly toward liverpool victoria, universally recognized across the sector as lv=, instantly highlights a significantly more calculated, structurally resilient approach to master portfolio management. their deeply engineered capacity parameters stand out as particularly robust, specifically optimized to effortlessly absorb the intensely chaotic variables associated with modern multi-generational living environments. the proprietary lv= technical architecture explicitly permits the seamless integration of one heavily fortified primary residence concurrently linked with up to six distinct domestic vehicles and an astonishing twelve officially named drivers, fully enclosed within one highly cohesive digital framework.

CAPACITY WARNING:

we must strictly verify all localized driver limits. while technologically capable of absorbing twelve distinct profiles, the underlying algorithm rapidly recalculates the total premium based upon the individual risk metric of every person introduced.

unquestionably, the absolute pinnacle feature requiring our immediate strategic attention revolves around their proprietary, incredibly potent forward-pricing guarantee mechanism. we constantly highlight the immense tactical utility generated by properly deploying this exact digital tool. utilizing this specific operational feature fundamentally empowers us to legally lock down a highly accurate premium estimate for any formally scheduled, future vehicle addition during the initial phases of the quotation process. by systematically eliminating the intense anxiety associated with unpredictable mid-term actuarial recalculations, the lv= platform guarantees absolute budgetary certainty, positioning it as an overwhelmingly superior option for portfolios anticipating imminent automotive acquisitions or lease rotations.

THE BROADER MARKET: AVIVA, CHURCHILL, AND DIRECT LINE

synthesizing a genuinely comprehensive overview of the entrenched legacy sector forces us to aggressively analyze the defensive posturing of the remaining massive corporate titans. direct line, historically infamous for fiercely refusing to submit their proprietary pricing directly into generic aggregator algorithms, approaches the unification strategy utilizing a highly complex series of discrete, interconnected multi-product discounts. they systematically generate reduced base rates simply for synchronizing our foundational transport and dwelling, concurrently deploying highly attractive ten percent peripheral reductions aimed at secondary products like specialized pet coverage or essential travel insurance, forging an incredibly sticky web of corporate reliance.

ADDITIONAL SAVINGS TIPS:

we heavily advise actively auditing the platform for bundled pet insurance options. specific tier-one providers enthusiastically release an immediate ten percent baseline compression specifically for migrating our complex animal companions onto their network.

similarly, heavily entrenched institutional monoliths such as aviva and churchill weaponize their staggering historical brand equity and deeply cultivated consumer trust signals to ruthlessly monopolize massive sections of the active marketplace. these massive corporate forces meticulously construct heavily interconnected product ecosystems precisely engineered to silently absorb the absolute entirety of a target household’s annual risk expenditure. even though their localized operational mechanics frequently appear distinctly traditional, their utterly massive internal capital reserves permit them to comfortably underwrite exceptionally highly valued, bespoke localized assets that newly launched, totally tech-reliant disruptive carriers simply lack the mathematical foundation to safely ingest.

DECODING DEFAQTO 5-STAR RATINGS IN BUNDLED INSURANCE

operating deep within an industry purposefully obscured by extremely aggressive, heavily misleading promotional language, we absolutely rely upon fiercely independent, empirically verified quality assurance data. this necessity dictates our uncompromising reliance upon defaqto. operating strictly as a highly respected, totally independent united kingdom financial intelligence and structural rating agency, defaqto wields their proprietary algorithms to violently strip away superficial marketing claims, critically evaluating the raw contractual integrity of thousands of retail products, ultimately assigning a notoriously honest star rating strictly reflective of genuine, verifiable coverage density.

QUALITY REMINDER:

an elite, completely verified 5-star defaqto rating mathematically confirms the entire architectural framework survived rigorous testing for quality and extreme coverage breadth, heavily prioritizing structural integrity over merely generating the lowest price.

we rigidly command our internal auditing processes to actively and entirely exclusively target fully verified five-star defaqto products when carefully assembling any complex multi-cover bundle. acquiring this heavily restricted elite classification operates as an utterly non-negotiable contractual warranty guaranteeing our chosen platform contains the most advanced defensive characteristics. we fundamentally demand deeply expanded single-item compensation ceilings, massively sweeping accidental destruction parameters, and utterly vital trace-and-access algorithms engineered for concealed plumbing failures. willingly accepting vastly inferior, heavily downgraded products merely to manufacture a superficially cheaper combined digital price represents a catastrophic strategic error that virtually guarantees complete fiscal annihilation during a severe claims scenario.

STRATEGIC BLUEPRINT: HOW TO EXECUTE A FLAWLESS MARKET COMPARISON

we rapidly approach the critical transition phase, shifting entirely from abstract theoretical market mapping toward intensely practical transactional execution. perfectly understanding the foundational architecture driving a car insurance and home insurance combination remains fundamentally useless without deploying a strictly sequential methodology explicitly designed to extract the maximum financial advantage from corporate quoting engines. we fiercely warn against the incredibly toxic behavioral flaw of passively accepting the very first integrated quotation an external algorithm presents. complete blind acceptance functions as the exact consumer vulnerability the entire underwriting industry deliberately exploits to mathematically maximize their centralized profit margins.

TIME INVESTMENT NOTE:

highly disciplined market analysts routinely dedicate a focused 45 minutes to the absolute core comparison cycle once annually. deploying this tiny localized time investment continuously yields hundreds of retained pounds.

executing our proprietary tactical blueprint strictly requires a heavily regimented, utterly unyielding mathematical approach to procurement. we actively isolate the fluctuating digital variables, firmly establish an impenetrable numerical baseline, and force the proposed combined architecture to empirically demonstrate verifiable superiority. actively treating the entire quotation sequence as a fundamentally rigorous corporate negotiation rather than a simple retail checkout instantly restores our massive tactical advantage. rigorously following this precisely structured sequential algorithm guarantees that the psychological pull of total administrative convenience never compromises the mathematical integrity protecting our core domestic liquidity.

STEP 1: ESTABLISH THE STANDALONE BASELINE PREMIUM

our foundational fiscal strategy initiates entirely with locking down an utterly uncompromising, mathematically rigid anchor position. long before we even initiate a preliminary digital query regarding an integrated multi-cover quotation, we absolutely must legally define the absolute financial floor currently available across the open market. our analytical process heavily relies on deploying trusted independent aggregator networks, aggressively scanning for the absolute lowest, functionally resilient standalone motor policy active today. immediately following that exact digital strike, we initiate a completely isolated secondary process laser-focused on extracting the most competitive standalone residential real estate contract currently published.

CALCULATION REMINDER:

the finalized unified master quote absolutely must heavily undercut the exact combined total generated by adding our two discrete baseline figures. should the integrated package fail to definitively beat this exact number, the bundle is a bad deal.

directly aggregating these two mathematically distinct, highly optimized discrete premiums into a single equation perfectly establishes our definitive baseline target. this highly precise integer permanently functions as our absolute ultimate financial shield. the underlying operational logic dictating this maneuver remains intensely simple: any highly touted, deeply integrated multi-cover digital proposal completely fails if it cannot mathematically crush this exact baseline figure into submission. should the massive corporate combined package arrive even a single isolated pound heavier than our meticulously established standalone baseline, the theoretical validity of the consolidation algorithm instantly shatters, explicitly demanding we utterly abandon the unified strategy for that specific renewal cycle.

STEP 2: AGGREGATE CRUCIAL UNDERWRITING DATA

correctly preparing for direct operational negotiations against elite corporate underwriting teams mandates the complete pre-assembly of a flawlessly accurate data package. external quoting algorithms violently penalize momentary hesitation or structurally missing historical variables. regarding the highly volatile automotive segment of the impending negotiation, we absolutely must instantaneously produce our exact driving license details, highly specific historical endorsement codes, a deeply verified five-year claims telemetry document, mathematically proven no-claims bonus certificates, and extremely precise engineering data covering absolutely any localized vehicle modifications or specific overnight storage vectors.

ORGANIZATIONAL TIPS:

strictly maintain a securely encrypted digital folder containing high-resolution photos of the primary automotive v5c alongside previous home policy documents to dramatically accelerate the complex digital application sequence.

extracting the deeply complex property metrics strictly demands an equally flawless, completely uncompromising data aggregation protocol. we definitively secure the absolute exact historical year of construction, deeply understand the foundational geological composite shaping the primary wall and roof materials, and retain massive historical awareness regarding deeply localized flood probability metrics or regional subsidence events. overwhelmingly, we calculate a highly researched, violently accurate replace-as-new financial sum accurately covering every single localized domestic possession. strictly utilizing completely disconnected digital evaluation algorithms guarantees we generate this threshold, fiercely dodging the completely lethal hazard of massive underinsurance that routinely obliterates trusting families following totally devastating atmospheric or thermal total-loss events.

CONCLUSION: THE STRATEGIC VERDICT ON CAR INSURANCE AND HOME INSURANCE

successfully concluding our relentlessly exhaustive deep-dive directly into the multi-cover ecosystem ultimately produces a totally definitive, mathematically sound final verdict. entirely zero doubt remains that actively merging our localized car insurance and home insurance profiles continuously functions as an incredibly powerful, heavily optimized digital mechanism perfect for violently eradicating deeply embedded administrative friction. whenever deployed utilizing strict mathematical precision, the hyper-aligned structural framework brilliantly synchronizes our chaotic fiscal existence, concurrently securing completely legitimate, highly verifiable baseline premium reductions that directly neutralize continuous macroeconomic inflation.

IS BUNDLING ALWAYS THE BEST CHOICE?

mathematically, absolutely not. heavily targeting a consolidated architecture makes strict logical sense solely for extreme convenience and shared perks, provided the total aggregate price remains violently competitive against isolated independent options.

nonetheless, our brutally rigorous internal analytics conclusively prove this massive digital mechanism remains functional only when deliberately deployed alongside extreme mathematical precision and utterly paranoid continuous vigilance. we intensely reiterate the totally non-negotiable operational necessity of sustaining a highly aggressive, combative posture exactly as the annual centralized expiration window approaches. we actively and continuously assault the deeply concealed institutional loyalty penalty by relentlessly forcing the incumbent carrier to mathematically justify their precise localized value against the open marketplace. furthermore, we strictly mandate violently testing every single unified multi-asset digital offer directly against our highly calibrated standalone baseline simply to guarantee the intensely marketed reduction represents genuine financial preservation rather than a deeply deceptive algorithmic illusion.

SCIENTIFIC NOTE:

rigidly executing recommendations pushed by the “cdc” regarding generalized household safety, while absorbing highly complex “nih” datasets concerning intense stress management, clearly proves that remaining heavily financially organized organically manufactures a deeply secure and stable home life.

we reject silent consumer apathy, prioritizing the immediate, decisive reclamation of absolute control over entirely decentralized financial liabilities. the deep, highly complex architecture shaping the broader underwriting sector explicitly intends to heavily monetize daily administrative exhaustion, yet armed with this completely unvarnished intelligence, we possess the exact mathematical blueprint required to fundamentally invert the traditional corporate power dynamic. referencing deeply established, highly vetted long-term financial stability benchmarks heavily supported by elite global entities like the “world health organization”, actively crushing continuous ambient fiscal anxiety operates as an absolutely mandatory component driving localized household resilience. immediately compile the highly precise underwriting documentation, calculate the totally unyielding standalone baseline, and ruthlessly execute this optimized comparison strategy today to lock down absolute maximum protection for your car insurance and home insurance at the lowest mathematically possible cost.