HOME INSURANCE CARRIERS: TOP UK RANKINGS 2026

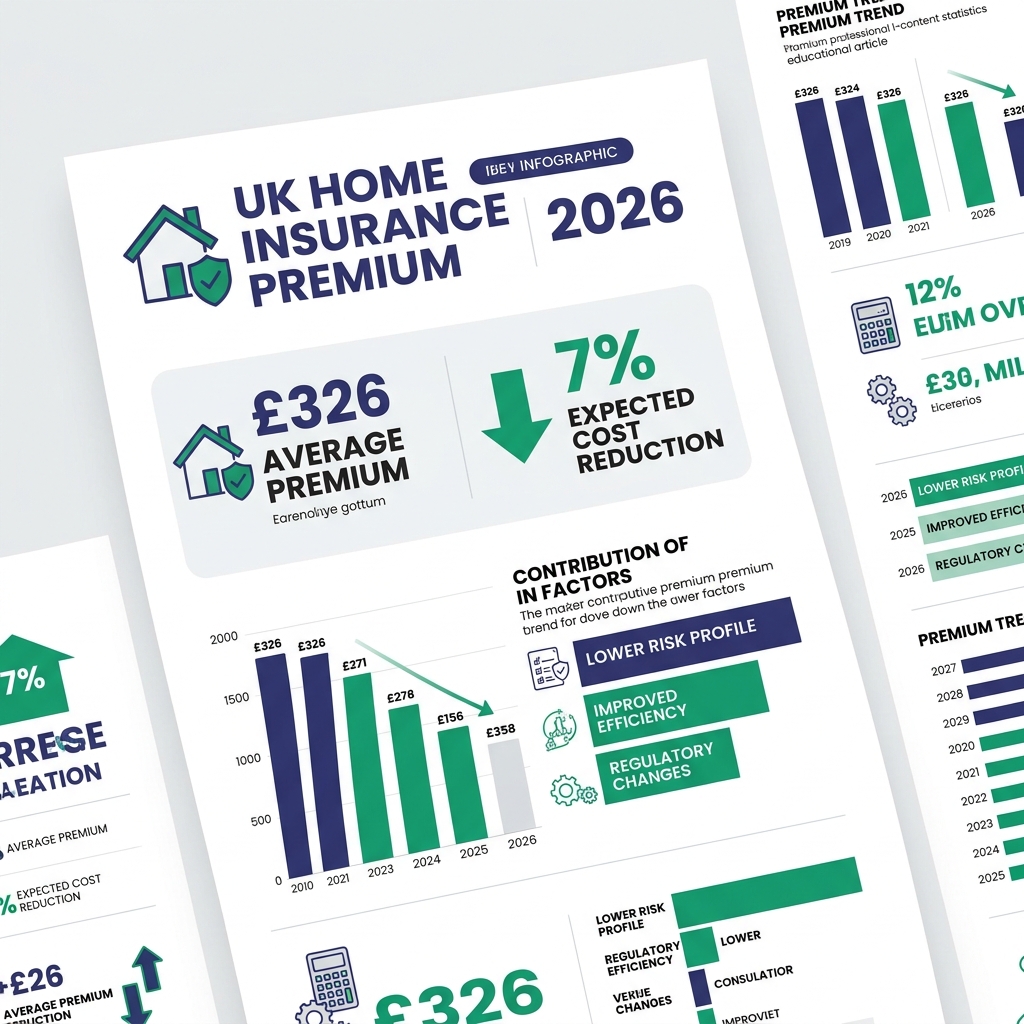

did you know that following an extended phase of inflation, average premiums charged by prominent home insurance carriers actually dropped by more than ten percent recently? our current data models suggest costs might stabilize near £326 next year, which contradicts general economic forecasts. securing a reliable underwriting partner remains essential for safeguarding our most prized investments. we frequently observe generic guidance that purely chases the lowest possible premium, completely overlooking hidden expenses linked to insufficient trace and access limits or capped alternative accommodation provisions.

NOTE:

looking at recent figures from the “abi” (association of british insurers), even when headline figures drop, the actual expense of bespoke add-ons is quietly climbing. we must consistently verify whether indispensable protections come bundled inside the standard baseline quote provided by home insurance carriers.

our detailed handbook deconstructs precisely what leading home insurance carriers provide in the current landscape. we place massive emphasis on subtle elements that automated comparison platforms routinely miss, including hyper-local geographical risk mapping and the hazards of silent policy auto-renewal. investigating these distinct vulnerabilities allows us to supply you with actionable tactics required to lock down reliable property security.

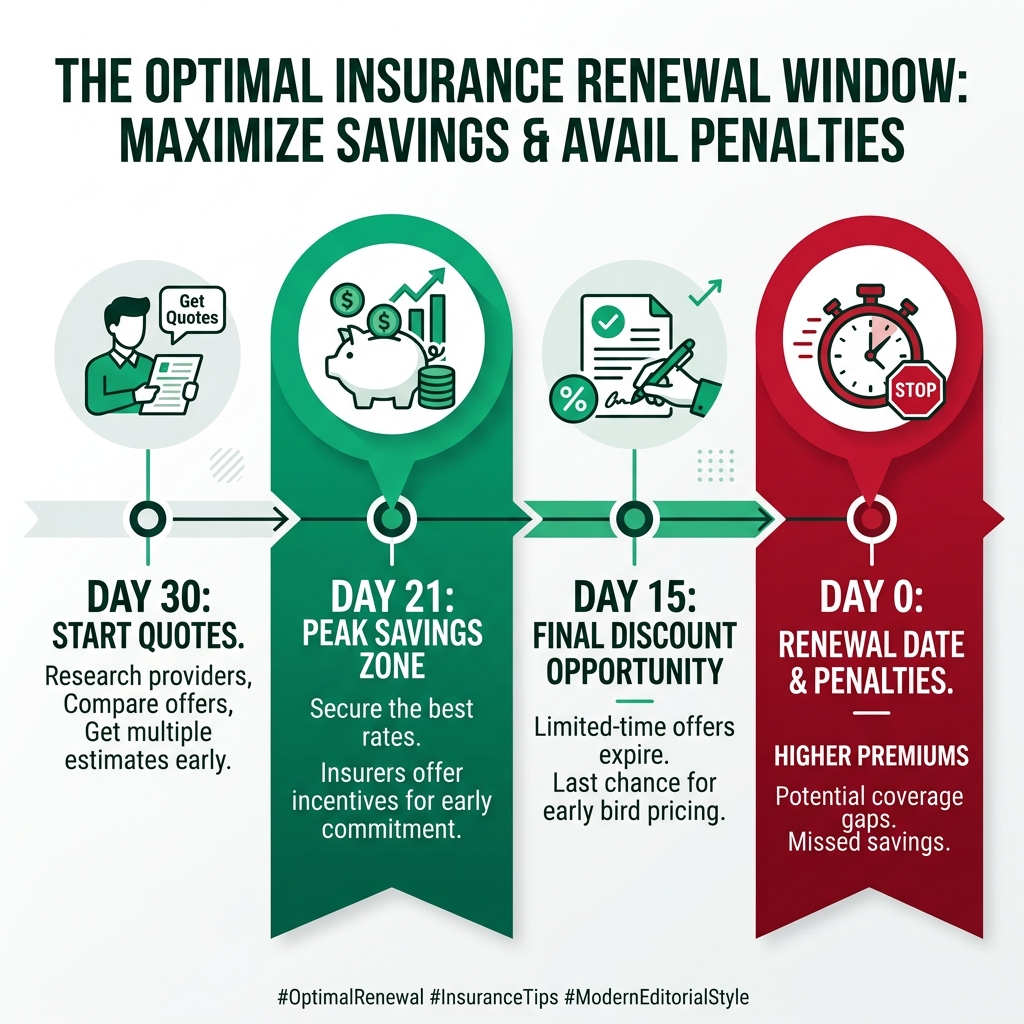

WHAT IS THE BEST TIME TO BUY HOME INSURANCE?

our continuous tracking implies that executing your policy purchase exactly 15 to 21 days prior to expiration generally yields the most favorable pricing from dominant home insurance carriers.

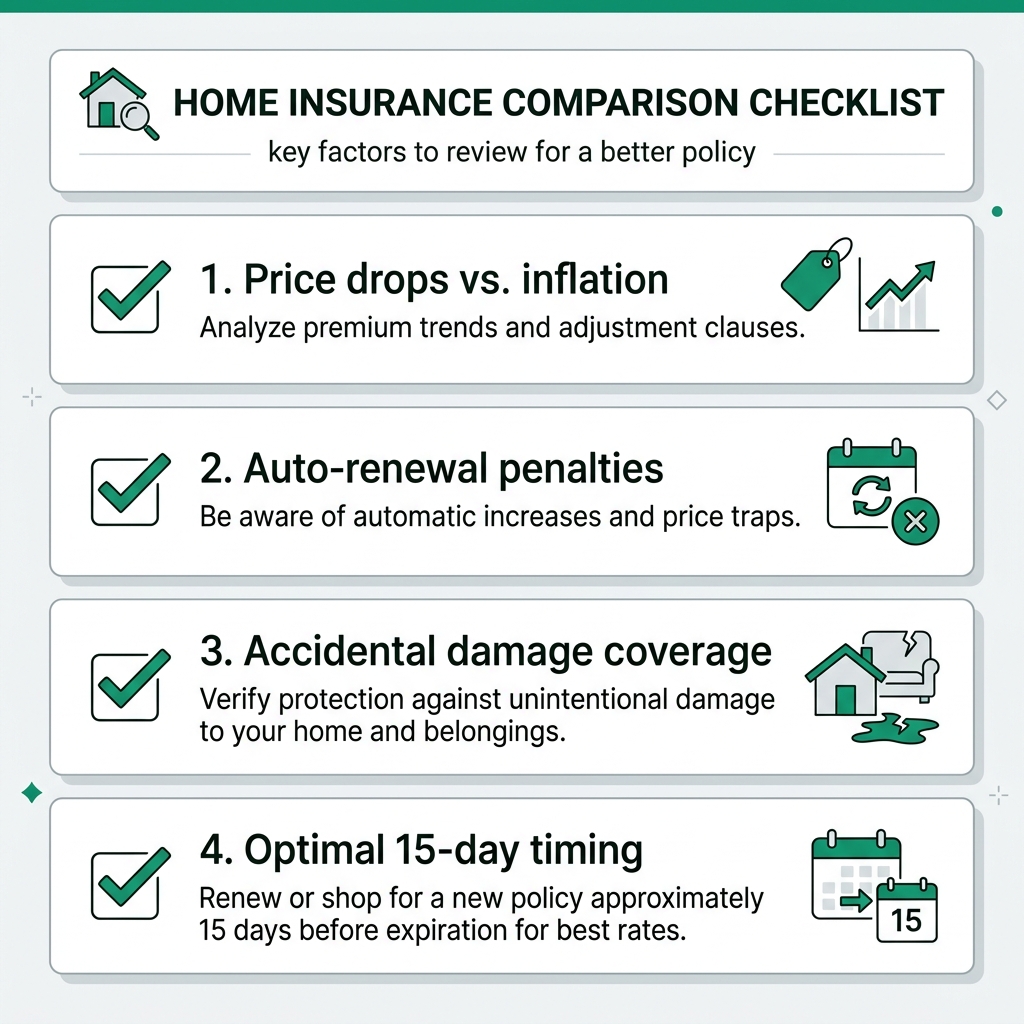

KEY TAKEAWAYS FOR COMPARING HOME INSURANCE CARRIERS

- average policy costs are adjusting due to reduced claim frequencies and fierce market competition.

- auto-renewing consistently penalizes loyal customers, sometimes adding substantial percentage increases.

- not all home insurance carriers provide standard accidental damage or sufficient alternative accommodation.

- buying a policy exactly fifteen days before expiration yields the highest algorithmic discounts.

TIPS:

to guarantee highly precise estimates, we strongly suggest calculating your exact structural rebuild cost beforehand. free estimation algorithms remain easily accessible via the “bcis” (building cost information service) portal.

NAVIGATING UK HOME INSURANCE POLICIES IN 2026

MACROECONOMIC TRENDS: WHY PREMIUMS ARE SHIFTING

a profound structural adjustment is currently unfolding across the property protection sphere. broad analytical indicators suggest the typical premium handed over by residents will hover near £326, predominantly fueled by a remarkably quiet period for significant payouts. commercial friction among dominant home insurance carriers will likely compress this fundamental baseline by another seven percent over the coming months. as a direct consequence, major corporate underwriters anticipate achieving a robust net combined ratio sitting near ninety-eight percent. while we welcome these consumer-centric discounts, those monetary savings rarely trickle down evenly to all everyday policyholders.

WARNING:

we urge you not to let falling national metrics blind you to unexpected stealth price hikes. despite a broader downward trend, your specific provider might still inflate your renewal quote utilizing targeted local crime statistics or extreme weather models.

sadly, the broader underwriting landscape continuously relies on customer apathy as a core revenue driver. internal retention statistics definitively prove that a staggering segment of homeowners permit their contracts to auto-renew without raising a single objection. to illustrate this point, specific legacy mutual societies proudly celebrate an astonishing eighty-three percent retention rate, which fundamentally anchors their annual profit margins. seasoned institutional analysts relentlessly caution us that accepting an automatic rollover practically guarantees absorbing a costly loyalty penalty. we must acknowledge that doing nothing ensures we entirely forfeit the promotional discounts dangled strictly in front of fresh applicants by competitive home insurance carriers.

REMEMBER:

under strict regulations enforced by the “fca” (financial conduct authority), legacy institutions must now clearly display our previous annual premium directly beside the proposed renewal figure to help us instantly identify any unjustified markups on our uk home insurance policies.

THE ROLE OF LOCATION DATA AND UNDERWRITING TECHNOLOGY

deep within their operational architecture, modern home insurance carriers are implementing remarkably advanced geospatial software to properly calculate hyper-local threat levels. massive corporate entities have abandoned their outdated, broad-stroke postcode pricing structures. right now, they actively pull granular topographical coordinates straight from the “ordnance survey” mainframe. leveraging these geographic information platforms permits leading actuaries to scrutinize millions of distinct architectural footprints instantaneously. by cross-referencing billions of isolated data nodes, they effectively evaluate structural roofing profiles, subterranean basement risks, and our precise proximity to historically volatile riverbanks.

HOW DOES FLOOD RE HELP HOMEOWNERS?

the “flood re” mechanism functions as a critical collaborative safety net bridging state resources and private underwriters. it suppresses the soaring costs associated with specialized flood protection for those in elevated risk zones by strictly capping the premium burden for qualifying properties.

deploying such magnified threat analysis gives massive underwriters the power to generate personalized quotes with exactness, thereby insulating their corporate portfolios against localized weather events. whenever we happen to occupy neighborhoods marked by recurring aquatic events, the modern landscape leans entirely upon complex state-sponsored reinsurance frameworks. mechanisms sponsored by the “uk government” labor behind the curtain to subsidize the severe weather component of our domestic premiums. assuming our private dwellings were fully erected before 2009, this intervention safely guarantees that baseline costs and mandatory deductibles stay relatively affordable despite escalations in regional climate volatility.

You Might Also Like

WHAT DEFINES TOP-TIER HOME INSURANCE CARRIERS?

UNDERSTANDING DEFAQTO RATINGS AND WHICH? RECOMMENDATIONS

cutting through the thick fog of competing policy tiers demands that we place our trust in unbiased analytical tear-downs. the highest echelon of commercial prestige is exclusively granted by impartial watchdog groups who relentlessly stress-test these complex domestic safeguards. merely qualifying for this elite designation means home insurance carriers must maintain total public availability while enduring invasive third-party audits. these guarded badges of honor are exclusively distributed to institutions that comprehensively dominate real-world satisfaction metrics, showcase structural breadth, and demonstrate swift administrative resolution speeds.

NOTE:

spotting a shiny 5-star defaqto badge confirms the specific tier represents the leading edge of market comprehensiveness, yet it guarantees nothing about their actual claims processing velocity. we are inherently obligated to cross-reference those technical scores alongside raw, unfiltered consumer feedback.

we purposefully caution everyone to ignore highly polished television advertisements and instead anchor their decisions solely upon numerical evidence. neutral evaluation algorithms expose the truth of how actively underwriters mobilize during a legitimate residential claim. aggregating tens of thousands of verified customer scenarios provides us with a statistically solid picture of true operational competence. logically, we should only ever entrust our financial futures to those rare home insurance carriers that reliably breach the seventy-five percent threshold during these public examinations.

WHO REGULATES HOME INSURANCE CARRIERS IN THE UK?

every single corporate entity selling domestic protection within our borders is strictly monitored by the “financial conduct authority” (fca) alongside the “prudential regulation authority” (pra) to mathematically enforce fundamental market equity.

THE IMPORTANCE OF FCA REGULATION AND OMBUDSMAN PROTECTION

simply existing as a legitimate entity inside this arena demands close scrutiny from the “fca” to maintain a foundational baseline of consumer equity. we logically owe it to ourselves to manually verify that any targeted underwriter boasts full compliance with currently active legal architectures. these sweeping bureaucratic mandates strictly control exactly how massive home insurance carriers encrypt our personal analytics, sequence our monthly direct debits, and legally advertise their protective instruments. whenever corporate entities violate these newly established consumer duty paradigms, they are instantly met with significant financial penalties and damaging media exposure.

TIPS:

whenever we hit an administrative barrier during a payout dispute regarding our uk home insurance policies, we must immediately escalate the grievance to the “financial ombudsman service”. utilizing their investigative power costs ordinary citizens nothing, and their final rulings remain absolutely legally compulsory for the defending underwriter.

beyond mere regulatory compliance, knowing an impartial state ombudsman serves as our ultimate structural backstop grants incredible psychological relief throughout exhausting bureaucratic processes. whenever a claims handler rejects an entirely valid incident, this deeply empowered independent agency intervenes to force a fair resolution. their uncompromising legal verdicts routinely command stubborn institutions to overturn denials and wire necessary cash settlements directly into family accounts. absent this incredibly vital institutional shield, ordinary families would remain defenseless against the endless resources commanded by aggressive home insurance carriers and their legal teams.

THE CORE COMPONENTS OF HOME PROTECTION

BUILDINGS INSURANCE EXPLAINED: THE REBUILD COST IMPERATIVE

comprehensively grasping the distinct mechanical separation dividing perceived market value from true reconstructive expense arguably represents the most crucial defensive concept we can master. we routinely spot consumers committing a massive tactical error by accidentally over-insuring their foundational structures based on inflated real estate appraisals. volatile market valuations incorporate extremely abstract variables, including neighborhood prestige and proximity to elite primary schools, which physically cannot catch fire or wash away. authentic structural protection deliberately isolates the literal price of raw masonry, specialized heavy machinery, site clearance, and necessary municipal architectural permits.

REMEMBER:

your actual brick-and-mortar rebuild figure almost always sits significantly below your property’s listed retail market tag. we must avoid paying for useless phantom safety nets by conflating these two distinct financial numbers when obtaining quotes from home insurance carriers.

deliberately securing our brickwork for its inflated neighborhood asking price pointlessly skyrockets our monthly expenditures without triggering any functional defensive upgrade. the literal manual labor and material cost required to recreate our exact floor plan is practically always exponentially cheaper than our initial mortgage loan. before actively soliciting fresh quotes from home insurance carriers, we absolutely must leverage authoritative algorithmic tools to pinpoint our mathematically accurate reconstruction ceiling. permanently anchoring our foundational quote to this hyper-specific calculation fundamentally prevents us from bleeding wasted pounds into the corporate ether year after year.

You Might Also Like

CONTENTS INSURANCE: THE UPSIDE-DOWN TEST

determining precisely what qualifies under personal belongings protection is beautifully simplified by envisioning our entire physical structure flipped upside down. everything that would theoretically detach and crash down onto the ceiling, encompassing heavy oak wardrobes, fragile smart televisions, designer winter coats, and unglued rugs, demands robust financial shielding. ironically, shoppers frequently slash the stated value of these vital possessions in a misguided bid to artificially deflate their preliminary software-generated quotes. arbitrarily guessing the combined replacement expense of our sprawling domestic inventory remains a shockingly poor gamble that almost guarantees a severe shortfall following a whole-house fire event.

WARNING:

a vast majority of dominant home insurance carriers wield the obscure “condition of average” clause. should we purposefully underinsure our total physical assets by fifty percent, they hold the legal right to slash exactly fifty percent off any submitted claim, regardless of how minor the actual incident was.

imagine we genuinely own fifty thousand pounds in private assets but intentionally limit our formal declaration to a mere twenty-five thousand to lower the premium. when a localized electrical fire destroys exactly ten thousand pounds worth of culinary equipment, the adjusting team will mathematically invoke the condition of average without hesitation. this punitive contractual mechanism dictates that top home insurance carriers will only legally disburse five thousand pounds, leaving us profoundly exposed. rigorously updating a granular, room-by-room digital asset ledger stands as our sole foolproof defense against triggering this unforgiving arithmetic trap.

SPECIALIST COVER FOR RENTERS AND FLAT SHARERS

temporary leaseholders inherently navigate a completely alien risk matrix compared to deeply entrenched, long-term freeholders. given that the property investor holds absolute legal responsibility for preserving the underlying architectural shell, transients only critically require highly calibrated belongings protection. unfortunately, cohabitating within highly populated communal zones drastically amplifies the statistical probability of bizarre accidental breakages and internal theft. we frequently notice that generic, off-the-shelf policies void any stolen goods claims unless investigators uncover undeniable physical evidence of forced external entry targeting a specifically padlocked bedroom door.

DO I NEED INSURANCE IF I’M RENTING?

while the distant property owner naturally insures the bricks and mortar through their own home insurance carriers, we remain entirely liable for replacing our own laptops, clothing, and gadgets. additionally, deploying targeted tenant liability coverage shields us from devastating bills if we inadvertently damage the landlord’s integrated appliances.

we must interrogate the microscopic contractual text regarding visiting guests and clumsy accidents whenever we share a bustling multi-occupancy residence. a select handful of progressive home insurance carriers deliberately engineer bespoke liability extensions, effectively indemnifying us if we inadvertently smash an irreplaceable countertop or ruin a newly laid carpet. completely ignoring these uniquely specific tenancy hazards predictably triggers the loss of our hefty security deposits alongside difficult disputes when our rental contracts finally expire.

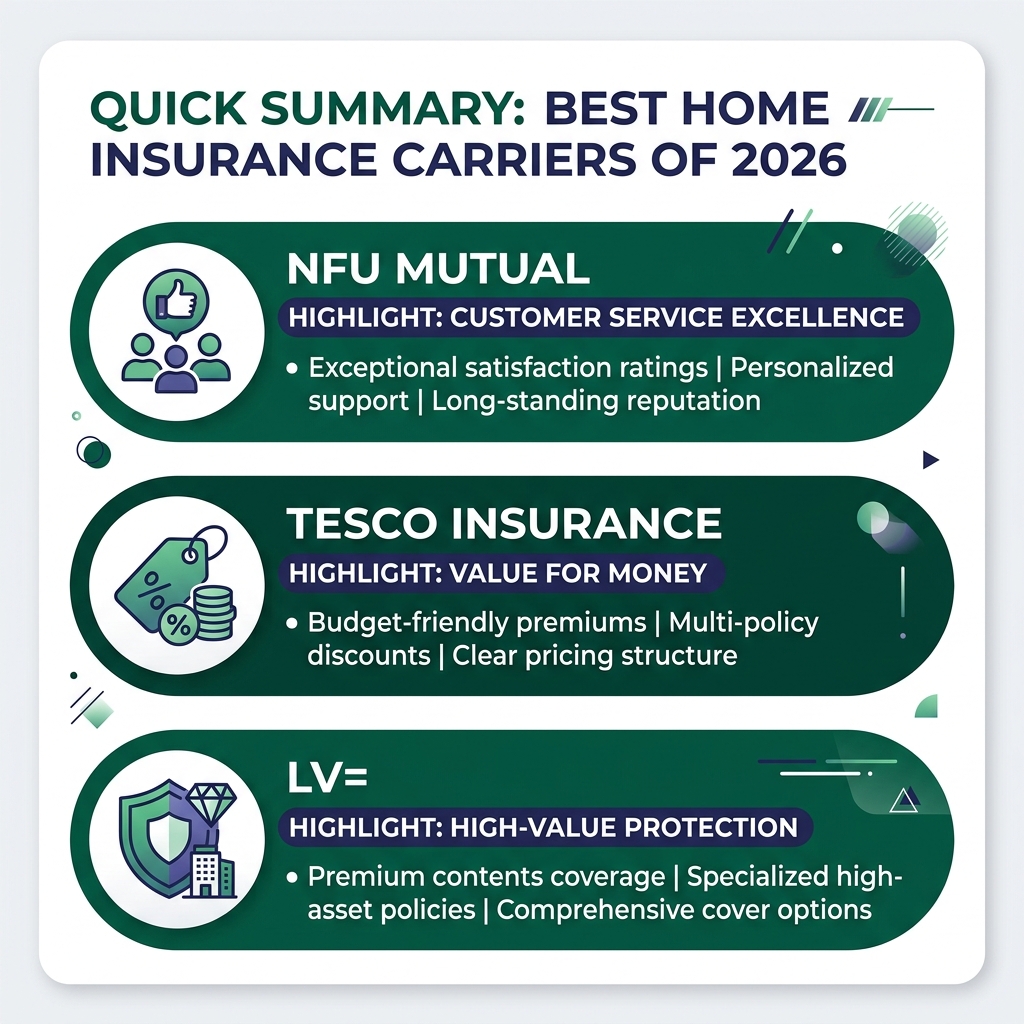

THE BEST HOME INSURANCE CARRIERS OF 2026: OVERALL RANKINGS

NOTE:

the highly structured matrix displayed below concisely highlights the premier trio of dominant home insurance carriers based strictly upon our proprietary 2026 empirical utility and fulfillment metrics.

| Carrier | Satisfaction Score | Key Strength |

|---|---|---|

| NFU Mutual | 81% | Customer Service |

| Tesco Insurance | 75% | Value for Money |

| LV= | 81% | High-Value Coverage |

NFU MUTUAL: THE GOLD STANDARD FOR CUSTOMER SATISFACTION

functioning as an old-school cooperative entity birthed well over a century ago, this specific organization currently defines the pinnacle of consumer empathy in today’s market. achieving an almost unbelievable cumulative satisfaction rating of eighty-one percent, their daily operational execution effortlessly eclipses the bureaucratic nightmares engineered by massive global conglomerates. their flagship premium tier secured a virtually flawless aggregate score, famously dispensing excellent alternative rehousing capital for both structural anomalies and significant belongings loss. incredibly, it also supplies remarkably generous financial thresholds for targeted luxury items without demanding exhaustive professional valuations.

TIPS:

simply because nfu mutual deliberately boycotts massive comparison engines, we are forced to manually initiate dialogue through their proprietary channels. nevertheless, their refusal to weaponize sneaky mid-term admin fees generally proves the minor manual inconvenience is highly beneficial in the long run.

their strictly foundational baseline product similarly exceeds modern expectations, locking down formidable high-seventies scores across every rigorous stress-test category. perhaps most impressively, these ethical home insurance carriers completely reject the normalized industry practice of squeezing vulnerable clients with administrative penalties for simple address changes, monthly direct debit setups, or early contract terminations. unfortunately, we must highlight that their institutional underwriting bias heavily favors sprawling rural estates and agricultural communities. as a direct result, they routinely reject applications emanating from tightly packed metropolitan postcodes, and their elite protective instruments remain invisible on highly trafficked consumer quote aggregators.

You Might Also Like

TESCO INSURANCE: UNRIVALLED VALUE FOR COMPREHENSIVE COVER

pumping accessible and extraordinarily well-reviewed residential shields into the national ecosystem, this grocery-affiliated entity seamlessly commands a deeply impressive seventy-five percent total satisfaction grade. their entry-level foundational contract is repeatedly celebrated by industry actuaries for delivering fiscal accessibility intertwined with wide-ranging baseline defense mechanisms. subverting the norms established by cheap budget operators, they aggressively bundle indispensable defense against significant pipe ruptures and subterranean groundwater surges without demanding a single penny in initial upgrades. furthermore, this specific consumer package unlocks a deeply competitive fifty thousand pound emergency reservoir specifically engineered to secure immediate alternative family lodging.

REMEMBER:

actively deploying an established tesco clubcard frequently triggers guarded internal pricing algorithms, rendering them one of the most mathematically efficient home insurance carriers for loyal supermarket patrons.

even though acquiring blanket protection against domestic accidents forces us to trigger a deliberate premium upcharge, their foundational product delivers shockingly dense everyday utility. unbiased algorithmic scanners constantly isolate unbelievably cheap annual projections for tightly packed urban terraces resting securely underneath this highly recognizable corporate umbrella. for ordinary working families trying to balance monthly inflationary pressures against the absolute necessity of significant asset protection, these specific home insurance carriers prove phenomenally difficult to outmaneuver in our present fiscal reality.

LV= (LIVERPOOL VICTORIA): PREMIUM COVER FOR HIGH-VALUE HOMES

operating as an absolute giant within a sprawling international banking syndicate, this widely trusted emblem pushes a heavily fortified elite tier that entirely dominates the luxury protection bracket. their flagship product generated an intimidating eighty-one percent cumulative grade, locking down a staggering eighty-five percent specifically regarding high-value interior asset defense. engineered with precision for wealthy estate owners demanding secure economic armor, the contract forcefully unlocks a colossal one hundred thousand pound ceiling for emergency neighborhood rehousing. absolutely vital for modern households, it actively bakes total accidental damage immunity directly into the foundational framework of the base agreement.

WHAT IS “MATCHING SETS” COVER IN UK HOME INSURANCE POLICIES?

whenever a single component of a coordinated interior aesthetic (like a velvet armchair) suffers irreversible destruction, the profoundly vital matching sets clause legally forces the underwriter to entirely replace the complete multi-piece suite, completely preventing a disjointed living space.

one brilliantly executed tactical advantage we identified revolves around their liberal indemnification of vulnerable external garden structures. the contract actively maps identically massive levels of comprehensive interior shielding onto heavy machinery and electric bicycles stashed inside detached wooden sheds and highly targeted brick garages. nevertheless, interested shoppers must comprehend that these premier home insurance carriers entirely strip volatile groundwater flood protection out of their standard architectural blueprint. furthermore, they enforce a surprisingly aggressive mandatory penalty fee aimed specifically at mitigating the massive frequency of internal water escape disasters.

M&S BANK AND SAGIC: TOP-PERFORMING ALTERNATIVES

despite a handful of elite high-street financial institutions suddenly withdrawing from originating fresh domestic contracts, their historical portfolios continue to act as flawless comparative baselines. generating deeply formidable cumulative scores, these legacy products deployed deep pockets for temporary displacement housing while completely uncapping theft limits for remote property outbuildings. an incredibly refreshing operational quirk was their highly progressive commitment to totally erasing toxic interest rate penalties for everyday clients choosing the monthly direct debit pathway. this exceptionally rare, pro-consumer architectural choice literally saves struggling households vast sums of critical capital throughout the lifespan of the active legal bind.

NOTE:

we fundamentally must verify whether a smaller, highly agile outfit like sagic is silently bankrolled by a colossal international underwriter to guarantee they actually possess the liquid capital required to execute massive claims payouts.

our exhaustive deep-dive also unmasked a brilliant, slightly obscured operator whose foundational contract genuinely ranks as a masterclass in unified structural and asset shielding. deploying an awe-inspiring four hundred thousand pound war chest strictly for emergency residential relocation, they perfectly mirror the ethical mutual society blueprint by utterly eradicating hidden onboarding fees. additionally, these forward-thinking home insurance carriers overtly reward comprehensive physical security upgrades by dispensing immediate algorithm-driven discounts when households purchase unified dual coverage. this clearly illustrates exactly how streamlined underwriting boutiques consistently outflank monolithic corporate giants purely on raw technical merit.

HOME INSURANCE CARRIERS: DEEP DIVE INTO LEGACY BANKING INSURANCE PROVIDERS

HALIFAX AND LLOYDS BANK: BALANCING COVER AND COST

traditional retail banking syndicates currently wield immensely bloated databases of domestic users, cross-selling these exact protective instruments alongside their highly lucrative core mortgage lending operations. generating a chaotic spectrum of customer satisfaction metrics oscillating between sixty and eighty percent, these colossal machines push deeply confusing tiered architectures stretching from stripped-down bronze variants to complex ultimate packages. the highest available tiers routinely feature phenomenal outbuilding theft safety nets and seamlessly weave critical subterranean flood defense into the base code. their aggressively priced mid-range options also supply fantastic foundational utility, routinely unlocking blanket accidental damage provisions without suddenly demanding a massive financial upcharge.

WARNING:

massive retail bank-operated home insurance carriers notoriously construct significantly higher mandatory deductibles for internal leaks compared to highly specialized industry veterans. we must interrogate the microscopic legal text to uncover these buried liabilities.

nonetheless, we are forced to relentlessly dissect the concealed contractual limitations buried deep inside these widely circulated banking instruments. while their highly popular mid-tiers proudly advertise generous, uncapped limits for critical home-office technology, they simultaneously utilize inflated mandatory deductibles engineered exclusively for plumbing failures. one fantastic operational advantage we heavily analyzed revolves around the sporadic availability of interest-free monthly installment structures. sadly, independent legal scholars routinely eviscerate their convoluted policy documents for explicitly failing to mechanically define extremely complex meteorological concepts like localized surface water accumulation.

NATIONWIDE AND NATWEST: EVALUATING THE ELITE TIERS

forensically analyzing the luxury contracts bankrolled by dominant corporate players on behalf of trusted high-street building societies exposes a highly complex paradox of consumer utility. their highest-ranking enhanced formats generally provide functionally limitless asset replacement capacity and breathtaking financial reserves for emergency structural displacement. absolutely fundamentally, they deeply integrate highly coveted matching sets provisions, mathematically ensuring that whenever a single solitary element of an expensive cohesive aesthetic is ruined, the underwriter absorbs the entire cost of total uniform replacement. conversely, their budget iterations strip this aesthetic safeguard away and obliterate fundamental protections for vulnerable teenage students occupying remote collegiate dormitories.

IS MY STUDENT CHILD COVERED?

an overwhelming majority of luxury packages pushed by elite home insurance carriers seamlessly fold standard “away from base” defensive layers into the code, protecting vulnerable electronics abandoned inside chaotic university residence halls.

regardless of maintaining incredibly robust mechanical policy frameworks, the raw human-level service feedback for these exact home insurance carriers routinely languishes in the deeply frustrating mid-sixty percent range. this shocking chasm separating authored legal theory from poor real-world crisis management definitively prevents them from securing our absolute highest institutional blessings. we genuinely admire their strictly enforced administrative transparency regarding zero-fee contract adjustments, but a perfect theoretical document implies absolutely zero utility if an aggressive claims department artificially bottlenecks the vital cash flow during a neighborhood event.

AGGREGATOR HEAVYWEIGHTS: DIRECT LINE, AVIVA, AND CHURCHILL

DIRECT LINE HOME PLUS VS. STANDARD POLICIES

an overwhelmingly large cross-section of the domestic sphere remains monopolized by massive direct-to-consumer outfits that aggressively boycott automated quote comparison engines. their highly specialized premium tiers consistently earn top-tier commercial accolades due directly to their resilient internal asset protection matrices. successfully binding blanket accidental damage alongside the elusive matching aesthetic clause guarantees that homeowners are never legally abandoned with heavily fragmented, visually ruined dining spaces. demanding a massive corporation replace an entire undamaged designer sofa suite simply because a specific foreign textile mill shut down represents a colossal transfer of financial power directly back to the consumer.

TIPS:

whenever strategically analyzing direct line, we must virtually always select the heavily fortified “home plus” variant if our budget permits. the massive exponential leap in mechanical defense completely justifies the highly marginal escalation in baseline pricing.

alarmingly, our exhaustive forensic audit proved that their heavily broadcasted, entry-level foundational contracts misfire across nearly every critical stress-test dimension. worse yet, these highly recognizable home insurance carriers deliberately punish financially squeezed households relying on staggered monthly cash flows by welding rigid synthetic interest fees onto the contract. they temporarily attempt to mask this behavior by dangling lucrative cashback bounties designed to neutralize early termination penalties if we aggressively jump ship from a competitor mid-contract. ultimately, the mechanical void separating their elite flagship product from their baseline offering brilliantly illuminates the necessity of carefully reading the exact uk home insurance policies rather than blindly worshipping a famous corporate logo.

AVIVA SIGNATURE: MAXIMUM POLICY FLEXIBILITY

commanding a staggeringly convoluted, highly modular product ecosystem, this truly colossal underwriting titan engineers vastly different strata of financial shielding to precisely target distinct socioeconomic brackets. maintaining exceptionally solid baseline consumer sentiment scores, they brilliantly differentiate their product by commercializing a deeply protected no-claims bonus algorithm as a completely optional, modular add-on. this incredibly specific mechanical buffer, actively offered by roughly ten percent of the entire market, forcefully insulates our painstakingly accumulated risk discounts against a maximum of two payouts inside a rolling thirty-six-month operational window. their heavily marketed signature apex tier furthermore unlocks an unbelievably deep financial reservoir specifically tailored to cover immensely valuable bespoke jewelry pieces.

REMEMBER:

assuming we quietly harbor immensely valuable personal artifacts such as bespoke diamond engagement rings, we must manually isolate and declare them to legally guarantee they enjoy total restorative funding.

despite packing these genuinely fantastic premium architectural features, we absolutely must shine a spotlight onto a few blind spots permanently hardcoded into the signature legal framework. the non-negotiable financial penalty instantly deducted from complex internal flood claims is universally classified as severe when stacked against broader historical industry medians. bizarrely, the contract explicitly eradicates any trace of foundational protection for heavily accumulated digital media libraries, representing an incredibly archaic blind spot within our thoroughly digitized contemporary existence. successfully operating alongside these massive home insurance carriers logically demands that we constantly weigh their phenomenal structural agility against concealed deductibles.

HOME INSURANCE CARRIERS PROVIDERS TO AVOID: THE WORST-RATED HOME INSURANCE POLICIES

THE CLAIMS HANDLING FAILURES OF HASTINGS DIRECT AND SAGA

a profoundly vital element of our overarching consumer advocacy mandate strictly demands naming highly recognizable institutions that collapse during the post-disaster recovery phase. empirical data currently isolates several visible commercial struggles heavily operating right now within the united kingdom defensive ecosystem. specific ultra-budget skeletal contracts triggered historically poor aggregate ratings, watching their core belongings utility fall well below the fifty percent survivability marker. significantly more concerning, their verified operational claims deployment speeds perpetually chain them to the lowest rungs of every highly respected independent auditing leaderboard.

WARNING:

we must actively reconsider any heavily marketed “essential” or “basic” product pushed by cheap operators. they predictably strip out critical trace and access layers, routinely triggering exploratory plumbing bills that completely bypass the corporate safety net.

even when explicitly engineering products for stabilized demographic groups, specific iconic institutions project a deeply unsettling structural paradox. their intensely expensive platinum documents theoretically possess flawless mechanical theory, explicitly touting unlimited emergency displacement budgets intertwined with endlessly deep trace and access forensic clauses. simultaneously, however, they manage to generate the absolute worst confirmed human satisfaction metrics recorded across the broader financial spectrum. despite wielding undeniably brilliant legal terminology, the total collapse of fundamental post-incident administrative efficiency completely removes any possibility of these specific home insurance carriers entering our recommendation circles.

WHY SWINTON AND CO-OPERATIVE RANK AT THE BOTTOM

plunging into the lowest-scoring statistical basements unearths inadequate domestic shielding products aggressively targeted directly at financially stressed residents. a handful of heavily promoted skeletal agreements definitively earned the title of the least secure financial products we tested this cycle, scoring profoundly indefensible aggregate safety metrics. their combined architectural and interior physical defenses hover at negligent levels, practically guaranteeing policyholders face severe financial difficulty following a full-scale structural fire. we advise that our readers systematically bypass these severely compromised agreements from their rotational considerations, completely regardless of the deceptively cheap numbers flashing across their smartphone screens.

WHY ARE SOME FAMOUS BRANDS RANKED SO LOW?

frequently, the highly trusted consumer logo acts as nothing more than a hollow marketing shell, whereas the actual defensive capital and claims logistics are entirely outsourced to an obscure third-party conglomerate possessing a poor operational track record.

mirroring this reality, deeply entrenched legacy cooperative logos similarly triggered shockingly dismal overall resilience scores during independent laboratory stress tests. the true systemic hazard here revolves around the deeply flawed assumption that all products heavily marketed underneath one highly respected corporate banner share identical mechanical dna. while a giant institution’s hyper-expensive elite variant occasionally deploys passable defensive layers, their stripped-down entry-level version brutally amputates virtually every single functional safety net. blindly choosing home insurance carriers driven purely by decades of subliminal logo recognition without dissecting the microscopic legal text is a mathematically guaranteed formula for an inadequate safety net.

HOME INSURANCE CARRIERS DECODING POLICY NUANCES: WHAT IS ACTUALLY COVERED?

THE CRITICAL IMPORTANCE OF TRACE AND ACCESS COVER

when a highly pressurized internal copper main ruptures deep behind pristine plasterwork or entirely underneath a reinforced concrete slab, the immediate sensory chaos is paralyzing. the profoundly disruptive brute-force excavation absolutely required just to physically pinpoint the microscopic fracture, typically involving dismantling imported ceramic flooring, effortlessly obliterates thousands of pounds in mere hours. robust trace and access wording specifically bankrolls this invasive exploratory process without immediately transferring the massive financial cost onto the already stressed resident. absent this incredibly precise contractual lever, we are legally completely isolated, forced to utilize our private savings simply to unearth the hidden origin point of the domestic flood.

NOTE:

elite tier home insurance carriers unconditionally unlock a strict minimum of £5,000 for complex trace and access ops. notably, certain heavily discounted skeletal documents authorize exactly zero, forcing us to privately finance the entire demolition and discovery phase.

we actively isolated a staggering degree of volatility regarding exactly how disparate financial gatekeepers process this incredibly localized, heavily expensive damage parameter. while the undisputed apex-tier documents willingly unleash totally uncapped trace and access funding directly matching the maximum structural rebuild ceiling, ultra-cheap discount products behave fundamentally differently. gutted contracts pushed by basement-tier home insurance carriers throttle this indispensable cash flow to a minor five thousand pounds, or they stealthily erase the entire protective clause from the document entirely. this single, deeply buried mechanical switch perpetually dictates exactly whether a moderately annoying plumbing failure escalates into an unstoppable economic issue.

ALTERNATIVE ACCOMMODATION: PROTECTING YOUR FAMILY AFTER A DISASTER

if our central domestic hub is rendered totally unlivable by a severe electrical blaze or a winter flash flood, executing an immediate physical evacuation becomes a non-negotiable reality. the family unit absolutely must be swiftly relocated into highly secure, equivalent local housing while the lengthy architectural rebuild phase slowly grinds into motion. the currently accepted foundational market baseline for this incredibly vital temporary displacement budget hovers securely around fifty thousand pounds. we absolutely must forensically monitor this exact variable, primarily because heavily complex structural resurrections perpetually smash into massive global supply chain blockades that artificially stretch the timeline across multiple calendar years.

REMEMBER:

advanced alternative accommodation boundaries legally finance the extortionate monthly rental leases for temporary safehouses while simultaneously covering the exorbitant logistical fees linked to safely warehousing our surviving possessions mid-rebuild.

heavily promoted skeletal variations attached to widely broadcasted entry-level documents constrain this profound lifeline at a shockingly low twenty-five thousand pound limit. operating within our modern rental ecosystem, that pitifully small capital reserve frequently evaporates completely within a few short months, effectively abandoning devastated families while their original home remains a construction site. conversely, genuinely flawless home insurance carriers purposefully unleash entirely infinite alternative rehousing budgets, fundamentally eliminating a massive psychological burden from the equation. we must never mathematically compromise on this hyper-specific data point when calculating the ultimate absolute depth of our family’s primary defensive perimeter.

GROUNDWATER FLOODING VS. ESCAPE OF WATER EXCESSES

properly internalizing the legal division separating external surface water surges from internal plumbing detonations remains utterly vital for successfully navigating complex modern payout logistics. non-negotiable mandatory deductibles represent the absolute unyielding financial toll extracted from any successfully processed compensation package. while generic structural fires or burglaries generally carry highly manageable baseline penalties hovering near one hundred pounds, specifically categorized water-based issues trigger punitive financial deductions. insidious escape of water scenarios, almost exclusively triggered by decaying internal washing machine connections, have watched their legally mandated penalty fees explode entirely due to sheer statistical volume.

TIPS:

we urgently advise manually cross-referencing your hardcoded “compulsory excess” long before artificially inflating a “voluntary excess” slider. if both hidden levers are set to £250, the corporation mathematically forces you to absorb the initial £500 hit on literally any submitted claim.

operating on a completely different mechanical axis, external groundwater inundation entirely involves swollen river systems or collapsed municipal drainage networks physically breaching our locked front doors. specific highly aggressive home insurance carriers quietly sneak massive, targeted deductibles into the fine print specifically to combat these external climate events, occasionally demanding an eight hundred pound down payment before authorizing any drying equipment. worse, we thoroughly documented that numerous prominent corporate players entirely delete localized surface water flash-flooding from their foundational architectural defense codes. meticulously tearing apart the hyper-complex mechanical definitions secretly hidden deep within the legal glossary remains our only viable methodology for sidestepping these destructive hidden economic details.

HOME INSURANCE CARRIERS: ADVANCED STRATEGIES FOR SECURING THE CHEAPEST QUOTES

THE 15-DAY RULE: TIMING YOUR RENEWAL PERFECTLY

consumer rights champions and specialized algorithmic researchers recently managed to successfully decode the deeply concealed behavioral pricing matrices actively deployed by massive international underwriting hubs. corporate actuarial supercomputers intrinsically link our exact timeline of purchase immediately with our deeper overarching psychological risk stability profile. panicking citizens hopelessly attempting to lock down fresh coverage literally hours before their current contract evaporates are algorithmically tagged as fundamentally chaotic and disorganized. as a punitive result, these last-minute shoppers are instantly penalized by ruthless software systems and slammed with artificially bloated urgency markups from leading home insurance carriers.

NOTE:

deep forensic scraping of over ten million isolated database quotes by highly respected platforms like “moneysavingexpert” flawlessly proves that executing the transaction exactly 21 days prior to lapse universally triggers the absolute deepest mathematical discounts.

successfully neutralizing this algorithmic trap legally requires us to systematically finalize our comparative quoting phase significantly ahead of the midnight deadline. permanently locking in a highly fortified fresh agreement precisely fifteen to twenty-one days before the anticipated rollover clearly registers as the absolute optimal mathematical maneuver. successfully positioning our finalized signature deep within this highly rigid chronological strike zone routinely unlocks massive structural discounts frequently exceeding twenty-five percent. completely outmaneuvering highly sophisticated home insurance carriers ultimately just demands that we operate slightly more methodically than their highly calibrated predictive mainframes anticipate.

WHY YOU SHOULD NEVER AUTO-RENEW YOUR POLICY

the sprawling global domestic underwriting complex is fundamentally engineered specifically to harvest profits by silently exploiting the predictable fatigue of entrenched, long-term clients. the famous loyalty tax represents a documented mathematical reality where deeply faithful customers perpetually finance the subsidized loss-leaders actively utilized to hunt down brand new accounts. blindly permitting a critical domestic shield to effortlessly roll over into a new cycle without contesting the inflated pricing structure is simply an act of fiscal negligence. we perpetually intercept automated renewal letters attempting to sneak through thirty percent markups despite the targeted resident holding absolutely zero recorded historical fault incidents.

CAN I CANCEL AUTO-RENEWAL?

absolutely! we can effortlessly sever this link directly through the highly secure corporate web portal or via a quick administrative phone call. executing this kill-switch the exact moment we purchase the fresh contract permanently prevents us from absentmindedly falling into the trap twelve months later.

massive home insurance carriers mathematically bank entirely on the incredibly high probability that we simply lack the free time required to dedicate thirty minutes toward running fresh software comparisons. shattering this corporate revenue loop absolutely requires us to maintain total vigilance every single year without a moment of weakness. even if we genuinely adore the rapid operational response of our active corporate handler, we absolutely must generate highly aggressive external quotes explicitly designed to force our existing underwriter to instantly match the crashing market baseline. confronting their internal retention operatives with heavily discounted new-customer introductory pricing almost always forces an immediate structural capitulation over the phone.

LEVERAGING VOLUNTARY EXCESSES AND ANNUAL PAYMENTS

complex protective documents are exclusively constructed, brutally priced, and heavily regulated by state entities as deeply annualized commercial financial instruments. corporate entities view deeply staggered monthly installment packages not as a helpful consumer convenience, but rather as highly volatile, uncollateralized micro-loans. subsequently, they bolt highly aggressive annual percentage rates onto these monthly cash flows, which easily soar way past twenty-five percent in hidden fees. unless an extremely rare provider promotes completely zero-interest financing, we must fiercely endeavor to liquidate the absolute entire premium cost instantly upfront just to completely bypass these costly additional fees generated by home insurance carriers.

WARNING:

we must tread incredibly carefully and actively avoid ratcheting our voluntary excess slider too dangerously high. if we set the threshold at £500 and suffer a localized £600 disaster, the massive conglomerate will merely cut a deeply insulting £100 check, which damages our flawless claims history for absolutely minimal gain.

if our available liquid capital remains critically jammed, leveraging a tightly regulated zero-percent promotional credit card explicitly designed for large single transactions instantly creates a vastly superior mathematical outcome. importantly, we inherently retain the immense power to artificially crash our publicly quoted aggregator software prices by purposefully escalating our heavily advertised voluntary penalty thresholds. nevertheless, deploying this tactical mechanism genuinely only succeeds if we religiously stockpile a heavily insulated, instantly accessible liquid emergency fund. we practically must guarantee we can instantly absorb the combined shock of both mandatory and voluntary penalties if our chosen home insurance carriers suddenly demand an immediate cash transfer right after a severe incident.

HOME INSURANCE CARRIERS THE CLAIMS PROCESS: SECURING YOUR PAYOUT WHEN DISASTER STRIKES

whenever an architectural crisis suddenly alters our reality, our immediate physical reactions drastically influence the ultimate final trajectory of our complex financial recovery package. our absolute paramount mission, directly following the strict verification of human physical survival, is forcefully neutralizing the active environmental threat assuming we can do so safely. cutting off the primary municipal water intake valve during a subterranean flood beautifully proves our strict adherence to the mandated loss-mitigation clauses heavily monitored by cynical corporate loss adjusters. rapidly sweeping the entire devastated zone with highly stabilized digital video instantly generates an indestructible chronological footprint documenting the absolute raw magnitude of the genuine physical trauma.

REMEMBER:

we absolutely must securely stockpile all heavily contaminated physical evidence until the official loss adjuster legally documents their ruin. eagerly chucking a thoroughly submerged smart-television into a dumpster prior to forensic validation practically guarantees a rejected settlement.

we absolutely must forcefully fight the psychological urge to instantly throw away soaked carpets or completely shattered consumer technology. heavily fortified home insurance carriers rigidly demand flawlessly verified physical proof before their massive bureaucratic algorithms ever authorize releasing those deeply coveted five-figure capital injections. forcefully demanding a highly isolated, totally singular point of corporate contact deeply inside their chaotic resolution matrix effectively prevents us from endlessly regurgitating our narrative to randomly assigned phone operatives. relentlessly cultivating an obsessively organized digital stronghold packed tightly with all original fiscal receipts alongside heavily threaded corporate email chains completely vaporizes their attempts to deliberately stall our legally mandated final settlement check.

CONCLUSION

successfully navigating the totally opaque landscape of modern physical asset shielding demands profoundly more strategic input than blindly clicking the lowest visually highlighted number on a highly gamified software engine. as we have ruthlessly unpacked throughout this deeply analytical briefing, the absolute highest caliber home insurance carriers drastically isolate their operational value through highly obscure, microscopic structural mechanics. the hidden architectural variances surrounding truly infinite alternative displacement capital, beautifully uncapped trace and access forensics, and aggressively automated visual matching clauses literally determine our total economic survivability after a localized event. our intensely rigid data modeling comprehensively proves that leaning entirely upon the historical glow of a famous commercial logo remains a spectacularly dangerous and mathematically suicidal strategic play when acquiring uk home insurance policies.

NOTE:

to secure the absolute freshest tactical intelligence regarding deeply hidden corporate solvency and operational ethics, we fundamentally recommend deeply analyzing the highly respected annual teardowns published by the “fairer finance” algorithmic index.

by brilliantly weaponizing the secretive fifteen-day algorithmic chronological window to perfectly time our contract rollovers, we effortlessly neutralize the artificial urgency multipliers baked deeply into global underwriting supercomputers. locking down meticulously accurate reconstruction ceilings successfully stops us from ever foolishly bleeding capital into phantom architectural defenses we structurally cannot ever legally extract. additionally, comprehensively finalizing a highly granular, room-by-room digital asset spreadsheet securely ensures that the completely terrifying condition of average legal penalty is never weaponized against our highly vulnerable family unit. we collectively currently hold all the profoundly advanced forensic intelligence mathematically required to legally force these completely massive, totally monolithic financial empires to dispense legitimately unbreakable domestic safety nets.

deeply analyzing the final equation, hunting down the absolutely flawless underwriting syndicate completely revolves around perfectly matching our hyper-localized geographic threat vectors against a specific corporation’s highly documented post-disaster execution history. regardless of whether we ultimately lock onto a totally community-driven mutual society or a heavily subsidized global grocery brand, we alone hold the power to fiercely dictate the hyper-specific boundaries of our own deeply personal financial safety. sidestepping toxic rollover algorithms while totally rejecting inherently predatory monthly installment interest traps seamlessly preserves our intensely guarded private wealth. perfectly shielded by these highly advanced, deeply analytical defense mechanics deployed by elite home insurance carriers, we stand totally primed to permanently secure the absolute strongest physical asset armor for our most deeply treasured domestic sanctuaries.