HOME INSURANCE AND LIFE INSURANCE: CRITICAL SECRETS FOR SECURE ASSETS 2026

focusing on home insurance and life insurance is a critical step for any property owner looking to guarantee absolute financial protection.

have we ever stopped to recognize that taking out a mortgage is often the largest financial commitment most of us will ever manage? finalizing property deeds means taking on a multi-decade liability, which necessitates robust, immediate safeguarding. our review of the uk landscape shows a frustrating pattern across common financial literature. widely read sources usually repeat the exact same points: secure buildings protection to satisfy the lender, and get mortality coverage to keep your family afloat. focusing strictly on home insurance and life insurance is a critical step for any property owner looking to guarantee absolute financial protection. however, we consistently observe that these guides bypass several vital nuances. they rarely unpack the concealed expenses found inside aggressively marketed packages that bundle home insurance and life insurance. analyzing long-term outcomes reveals they also skip over the severe risks tied to picking a basic joint first death setup instead of individual coverage. furthermore, those sources entirely gloss over complex situations, such as leasehold confusion or income drops for solo purchasers. investigating these specific oversights drives our objective today.

REMEMBER:

we need to ensure our protection strategy adapts whenever our domestic situation shifts, like relocating or expanding our family while managing our home insurance and life insurance premiums.

examining numerous distressed property scenarios gives us a distinct viewpoint on why things go wrong. families seldom face repossession purely because they had zero coverage; instead, the underlying issue is typically an incorrectly designed safety net. approaching this complicated sector requires an organized, factual framework. evaluating the actual mechanics of home insurance and life insurance allows us to separate industry jargon from practical utility. transforming our perspective helps us view these tools not as frustrating paperwork, but rather as critical elements for preserving long-term assets. acting as informed managers of our financial resources is essential, rather than remaining detached participants in the marketplace. optimizing our approach to home insurance and life insurance fundamentally shifts our economic security matrix.

DO I NEED BOTH HOME AND LIFE INSURANCE?

taking out buildings cover is generally mandatory for securing a mortgage, while mortality coverage provides a vital safety layer to help beneficiaries retain the property following an unexpected passing, proving why home insurance and life insurance remain inherently linked in financial planning.

KEY TAKEAWAYS FOR HOME INSURANCE AND LIFE INSURANCE

- buildings cover is a strict condition of our mortgage, active from the moment contracts are exchanged.

- life cover is technically optional but acts as the primary defense against repossession if a breadwinner passes away.

- bundling our home insurance and life insurance often leads to restrictive medical underwriting and coverage gaps.

- two single life policies offer drastically better long-term security than a standard joint first-death policy.

- income protection is a critical, frequently ignored supplement for single property buyers lacking financial dependents.

- evaluating the distinct separation of home insurance and life insurance guarantees maximum market leverage.

TIPS:

organizing a secure digital folder for essential documents ensures that relatives can locate necessary paperwork regarding home insurance and life insurance swiftly during a crisis.

DECONSTRUCTING THE JARGON: THE CORE DIFFERENCES EXPLAINED

defining terms accurately is the required first step before structuring any wealth defense mechanism. processing billions in annual premiums, the uk market utilizes incredibly distinct frameworks for calculating risk. looking closely at home insurance and life insurance, we are actually dealing with two remarkably different methods of transferring liability. physical structures and their contents are shielded from environmental damage or accidents by one type. preserving the economic stability of the individuals earning the revenue to pay for those properties is the sole function of the other. mixing these two concepts up represents a frequent misstep among newly minted property owners, which is why clarifying home insurance and life insurance functionality is paramount.

NOTE:

the “FINANCIAL CONDUCT AUTHORITY” monitors domestic markets to verify that companies treat consumers equitably and distribute transparent product details.

speaking practically, safeguarding the physical building and the goods kept inside is the core function of property policies. mortality coverage, on the flip side, mitigates the financial devastation caused by the sudden loss of an earner’s future income. “THE FINANCIAL CONDUCT AUTHORITY” oversees both arenas, yet the evaluation methods remain radically distinct. geographic data, such as local flood plains and historical subsidence, dictate the pricing for bricks and mortar. assessing personal health metrics, familial medical backgrounds, and daily habits determines the cost of human coverage. treating these instruments as isolated components of our wealth management plan is absolutely necessary to maximize the true potential of our home insurance and life insurance portfolios.

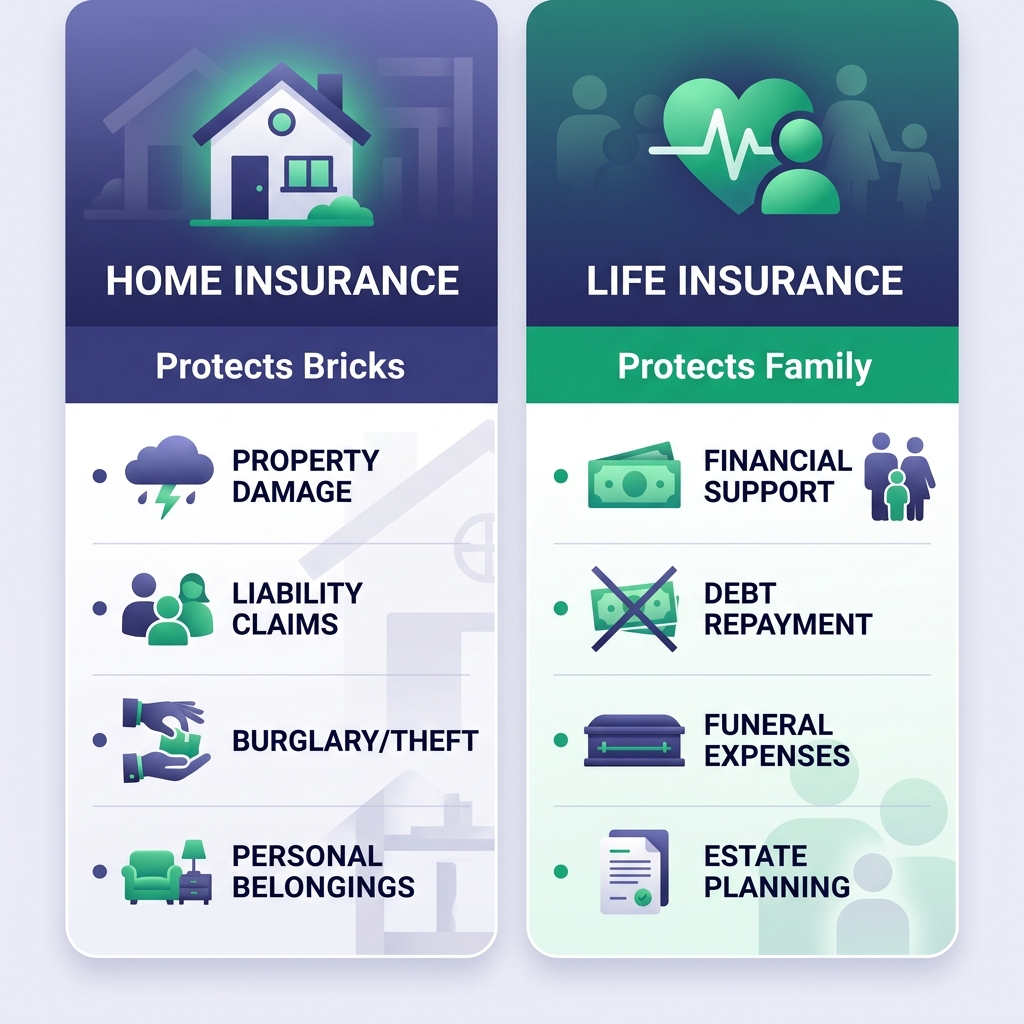

WHAT HOME INSURANCE ACTUALLY COVERS (BUILDINGS VS. CONTENTS)

structural coverage acts as an indemnity for the permanent, fixed elements of our residence. this category includes exterior walls, roofing materials, underground pipes, and permanently attached installations such as fitted cabinetry. should a devastating blaze or massive flood compromise the foundation, this specific contract funds the physical reconstruction process. calculating an accurate rebuild figure is vital, meaning we should focus on current labor and material expenses rather than the fluctuating market price of the real estate. integrating the cost of modern materials ensures our home insurance and life insurance evaluations remain grounded in reality.

WARNING:

failing to specify an adequate rebuild value frequently results in rejected claims or partial settlements that fall short of actual repair expenses.

movable goods transported into the residence fall under the umbrella of contents protection. visualizing the house being turned upside down helps clarify that anything falling out belongs in this category. everyday items, ranging from costly electronics and sofas to rugs and wardrobes, fit into this bucket. estimating the total replacement expense for these belongings is something we regularly undervalue during the initial quoting phase. integrating useful supplementary features, such as accidental damage or emergency breakdown assistance, bolsters our defense against sudden plumbing leaks or failing white goods. properly assessing these assets fortifies our overall home insurance and life insurance strategy.

WHAT IS ACCIDENTAL DAMAGE COVER?

purchasing this optional extra shields belongings from unintentional mishaps, including knocking over a television or accidentally hammering into hidden wiring.

THE FUNDAMENTAL PURPOSE OF LIFE INSURANCE FOR HOMEOWNERS

navigating the property market means utilizing mortality coverage for one highly targeted objective: eradicating the remaining mortgage balance if we pass away. generating a substantial, tax-free capital injection for our chosen beneficiaries is the primary function of this agreement. securing this exact outcome remains the goal for millions of domestic policyholders across the nation. forcing a grieving spouse or dependents to confront potential eviction due to a stopped salary is a scenario we actively seek to avoid. delivering that capital eliminates the debt, transitioning completely unencumbered ownership rights directly to our survivors.

treating this arrangement as a structured, contractual inheritance is much more productive than viewing it as a gloomy gamble on our lifespan. predicting the precise moment of our passing is impossible, yet the economic fallout of dying uninsured is a known fact. aligning the potential payout with our shrinking debt creates an impenetrable financial wall against creditors. retaining the physical residence we strove to buy becomes possible for our loved ones, completely unburdened by relentless monthly installments. coordinating our home insurance and life insurance ensures this inheritance mechanism remains mathematically viable.

LEGAL MANDATES AND MORTGAGE PREREQUISITES

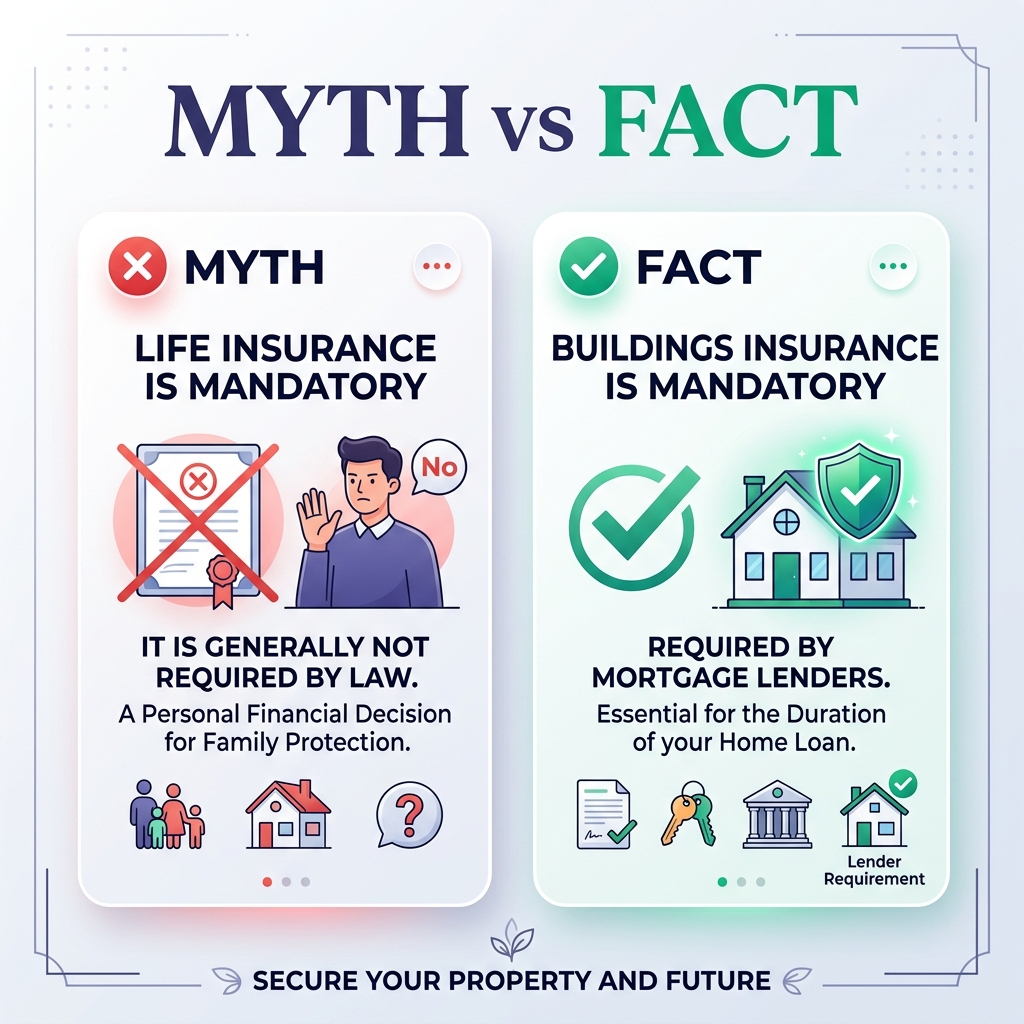

confusion surrounding legal duties regularly causes stress while we navigate the property acquisition timeline. separating rigid contractual demands from the strong suggestions offered by legal and financial professionals is a crucial step. delivering factual clarity helps us understand the landscape better. federal legislation in the uk does not compel any citizen to carry private personal coverage. retail banks, on the other hand, enforce their own strict risk management frameworks. borrowing massive sums means we have to operate within the specific guidelines established by these lending institutions.

NOTE:

securing the loan dictates that lenders demand buildings insurance, ensuring their financial collateral remains protected against total loss.

precision is essential when we attempt to satisfy these institutional constraints. assuming that coverage only needs to start on the day we pick up the keys is a widespread and dangerous misconception. leaving ourselves exposed financially is the direct result of this timing error. matching our activation dates perfectly against the legal timeline of conveyancing prevents these gaps. examining the exact stipulations of mortgage providers allows us to distinguish between their strict rules and our personal choices regarding home insurance and life insurance mandates.

WHY BUILDINGS INSURANCE IS A NON-NEGOTIABLE MORTGAGE CONDITION

obtaining clearance for funds from any legitimate uk lender absolutely requires demonstrated proof of structural protection. the physical structure functions as the primary collateral for their substantial financial outlay. watching a house burn down without a rebuilding safety net means the bank’s security evaporates in minutes. embedding rigid contractual clauses within the mortgage documentation forces us to sustain this coverage throughout the loan’s lifetime. lapsing on this specific requirement constitutes a direct breach of our lending agreement. it is the bedrock of the home insurance and life insurance foundation.

REMEMBER:

assuming legal liability happens the instant we exchange contracts, completely regardless of our actual physical move-in date.

grasping the exact chronology of our legal liability is non-negotiable. activating our structural plan must occur simultaneously with the exchange of contracts, rather than waiting for the final completion day. acquiring the risk for the building’s physical state happens immediately upon that legal exchange. fixing a roof smashed by a falling branch the following morning becomes our sole financial responsibility. bridging this perilous period requires perfectly synchronizing our coverage start date within the broader context of our home insurance and life insurance preparations.

THE TRUTH ABOUT LIFE INSURANCE: HIGHLY RECOMMENDED, BUT STRICTLY OPTIONAL

pushing back against high-pressure broker sales pitches reveals that no banking institution legally mandates mortality coverage for a residential loan. opting into this protection remains an entirely voluntary decision on our part. finalizing the transaction and occupying the residence with zero mortality safety nets is perfectly legal. highlighting the severe economic vulnerability we invite by taking this path is our duty as informational analysts. lacking a legal requirement certainly does not diminish the practical urgency of having the right protection. ignoring home insurance and life insurance synchronization is a massive financial gamble.

evaluating a typical two-income household illustrates the mechanics of this risk perfectly. combining two salaries is generally how we manage to comfortably pay the large monthly installments. losing a partner abruptly leaves the survivor attempting to service the entire debt load using half the historical cash flow. tracking these scenarios statistically shows a swift descent into arrears, often culminating in repossession. declining to secure our future is a massive wager placed against our family’s primary shelter.

CAN A LENDER DENY MY MORTGAGE WITHOUT LIFE INSURANCE?

avoiding mortality coverage will not legally stop a mortgage application, though banks heavily suggest it to bolster our baseline financial safety.

THE BUNDLING DILEMMA: SHOULD YOU COMBINE POLICIES?

consumer culture heavily conditions us to assume that packaging services together automatically yields superior pricing. applying this logic to broadband or media subscriptions is common, and we repeatedly try extending it to our fiscal defenses. deciding if linking our home insurance and life insurance through one giant corporation is a shrewd tactic or just an administrative convenience is a crucial debate. breaking down the actual mechanics behind multi-policy promotional rates requires objective scrutiny to determine if home insurance and life insurance truly belong together.

evaluating human mortality relies on actuarial parameters that differ wildly from those used to assess property risks. a firm offering incredible rates for localized flood hazards might penalize us unfairly when reviewing our personal medical records. determining whether the visual appeal of a unified login portal justifies the danger of acquiring inferior coverage is an essential calculation. balancing these logistical perks against the mathematical drawbacks demands careful consideration when optimizing home insurance and life insurance portfolios.

TIPS:

running a direct comparison of the total cost between standalone agreements and packaged deals reveals the true economic benefit.

THE ADMINISTRATIVE ADVANTAGES OF A SINGLE PROVIDER

keeping our various safety nets within a single corporate entity provides obvious logistical advantages. engaging a sprawling conglomerate that operates across numerous divisions radically streamlines our filing systems. accessing one central digital dashboard, dealing with a shareholder team, and leaning on brand familiarity offers undeniable comfort. lowering our overall administrative stress during a chaotic property relocation is incredibly appealing.

promotional discounts serve as the primary hook for these consolidated offerings. promising premium slashes of up to twenty-five percent is a standard tactic if we agree to merge our property and mortality defenses. trimming a visible chunk from our recurring monthly expenses is incredibly tempting when managing a tight household budget. synchronizing our renewal dates and centralizing our direct debits creates the very convincing illusion of maximum efficiency regarding home insurance and life insurance execution.

THE HIDDEN COSTS AND COVERAGE GAPS OF BUNDLED POLICIES

investigating these generic packages uncovers significant structural weaknesses in the combined approach. the underwriter proposing the lowest premium for our physical structure could simultaneously apply punitive health criteria to our personal coverage. possessing a minor historical medical issue, a higher bmi, or engaging in extreme sports can trigger harsh price hikes within the packaged deal. erasing the small savings gained on the property side is almost guaranteed when the mortality premium is artificially inflated.

WARNING:

accepting a package deal frequently results in weaker coverage on one front simply to secure minor savings elsewhere.

separating these financial products into distinct purchases is the strategy we generally champion. acquiring property safeguards from a general specialist, while securing mortality contracts from a dedicated health underwriter, usually produces stronger results. unbundling our home insurance and life insurance grants us the flexibility to maneuver through the market with surgical precision. sidestepping hidden exclusions, ensuring equitable medical evaluations, and ultimately lowering our combined monthly outlay are the frequent rewards of this targeted methodology.

NAVIGATING LIFE INSURANCE TYPOLOGY FOR PROPERTY OWNERS

exploring the landscape of personal protection often results in severe confusion due to the sheer density of product variations. navigating the sector’s complex vocabulary frequently masks the straightforward functional mechanics of the underlying contracts. dismantling these various options systematically is our current goal. matching the appropriate financial instrument directly to the specific amortization schedule of our loan is imperative. picking an incompatible structure means we risk overspending on redundant coverage or abandoning our family with a massive shortfall.

NOTE:

selecting a framework that perfectly mirrors how our mortgage debt shrinks over the decades is paramount.

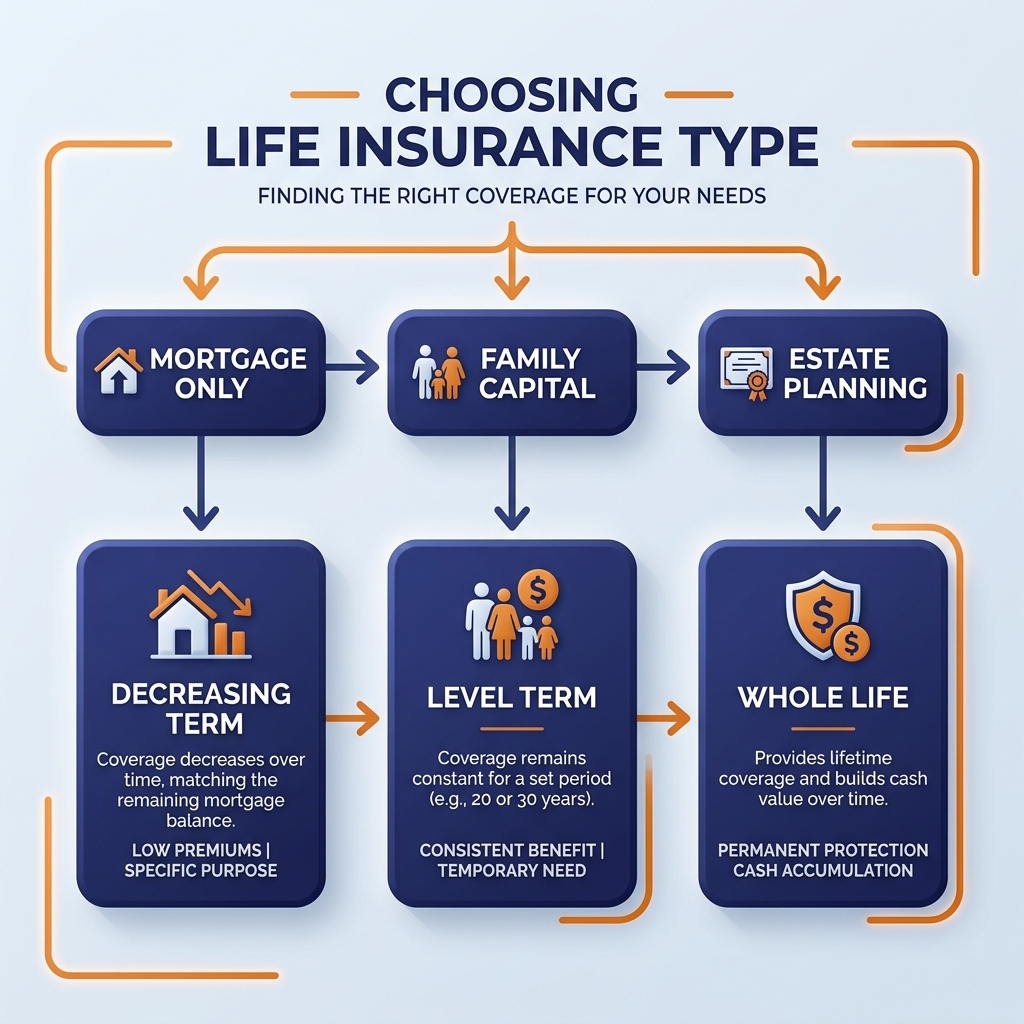

filtering the massive marketplace down to three core variations simplifies the decision for real estate buyers. tracking how the final death benefit behaves over the term length is the central factor differentiating these products. identifying whether the final capital injection diminishes, remains static, or guarantees a payout at any age is necessary. mapping the exact trajectory of the intended funds unlocks our ability to secure optimal coverage without overpaying. integrating these insights bolsters our home insurance and life insurance competence.

MORTGAGE LIFE INSURANCE (DECREASING TERM) EXPLAINED

targeting a standard capital repayment loan requires the precision of a decreasing term structure. operating this contract relies on incredibly straightforward mechanics. locking in a static monthly payment guarantees our costs, while the potential death benefit systematically reduces year after year. matching this downward slide with our shrinking principal balance creates a perfectly synchronized safety net. needing less capital to erase the debt as the years pass means the total coverage volume drops naturally in tandem.

WHY IS DECREASING TERM INSURANCE CHEAPER?

dropping the potential payout volume reduces the overall insurer’s risk, which directly results in a cheaper monthly rate for us.

minimizing the carrier’s future liability makes this format the most economical way to defend our primary residence. suffering a fatal event in the second year triggers a massive transfer of funds, wiping out the peak debt. dying in the twentieth year yields a much smaller sum, which still cleanly eliminates the final, minor arrears. paying exclusively for our precise current exposure level eliminates wasted premiums. highlighting this extreme efficiency explains why it remains our top suggestion for conventional buyers within their home insurance and life insurance architecture.

LEVEL TERM LIFE INSURANCE: PROTECTING MORE THAN JUST BRICKS

switching to a level term contract introduces a totally different mathematical path. fixing both the recurring premium and the ultimate capital payout for the chosen duration defines this mechanism perfectly. purchasing a five-hundred-thousand-pound safety net for three decades guarantees that exact figure pays out regardless of when the fatality occurs. maintaining a flat payout profile completely removes the reduction element, inherently driving the monthly price higher than a decreasing alternative.

REMEMBER:

securing a level term agreement guarantees a flat guaranteed lump sum capable of addressing both debt clearance and future household expenses.

deploying a level structure makes sense under highly specific financial conditions. carrying an interest-only loan mandates this approach, given that the base principal never shrinks during the lifespan of the debt. leaving a massive financial buffer for dependents is another excellent reason we point toward flat coverage. clearing the property debt is step one, and any surplus capital can subsequently handle school fees, grocery bills, and childcare, cementing robust economic continuity.

WHOLE OF LIFE COVER FOR ESTATE PLANNING

ensuring complete transparency demands a quick look at permanent coverage structures. contrasting sharply with fixed-duration contracts, these unique instruments never carry an expiration date. remitting our monthly dues faithfully ensures the carrier will dispatch funds upon our eventual demise. eliminating the guesswork around policy duration changes the fundamental nature of the product. transforming a statistical probability into an absolute certainty naturally pushes the monthly pricing into a much higher bracket.

utilizing permanent contracts to cover basic property loans is a tactic we almost never endorse. navigating complex inheritance logistics for high-net-worth estates is where these tools truly shine. generating immediate capital to offset severe tax burdens or covering substantial burial costs are the primary use cases. opting for standard term agreements remains a far more practical and affordable route for ordinary buyers attempting to protect a primary residence via home insurance and life insurance.

PROPERTY MORTGAGE PROTECTION VS. LIFE INSURANCE: CLEARING THE CONFUSION

tracking consumer search data exposes a hazardous habit of mixing up crucial terminology. tossing around phrases like payment defense, mortality coverage, and property mortgage protection interchangeably happens constantly. falling into this linguistic trap paves the way for disastrous misunderstandings regarding our actual safety nets. assuming we hold a massive death benefit while actually possessing a brief illness contract is a catastrophic error. defining the rigid borders between these unique financial tools is an absolute necessity.

fielding a vague pitch for “property mortgage protection” from a retail bank requires us to demand exact specifics on the underlying instrument. determining whether the contract drops a massive cash sum upon death or simply handles direct debits during a broken ankle is the priority. leaving massive vulnerabilities in our wealth defense is the direct result of conflating these two mechanisms. breaking down the exact mechanics of payment supplements shows exactly why they fail to replace true mortality contracts in the realm of home insurance and life insurance.

WARNING:

blindly assuming that basic mortgage protection provides a death benefit is dangerous; verifying the exact policy triggers is essential.

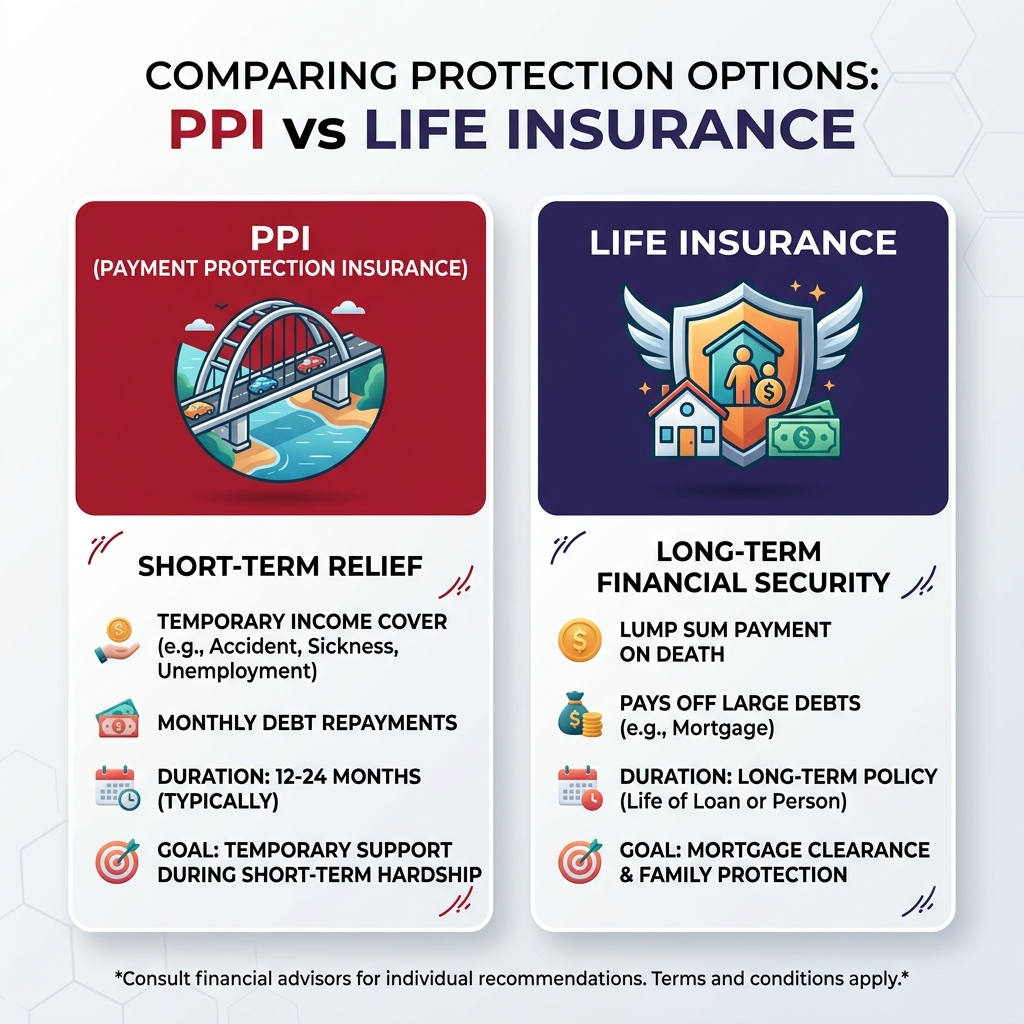

THE ROLE OF PAYMENT PROTECTION INSURANCE (PPI)

short-term payment defense serves as a temporary, localized financial bridge. stepping in to handle recurring housing obligations during sudden incapacity is its solitary purpose. sustaining a severe injury, receiving a long-term medical sick note, or facing involuntary termination are the standard activation triggers. sending cash directly to the banking institution prevents dangerous arrears from accumulating while we heal or hunt for a new job. this differs significantly from core home insurance and life insurance.

highlighting the severe constraints of this product is something we do aggressively. capping the payout window is standard practice, usually limiting assistance to a strict twelve or twenty-four-month period. cutting off the financial drip happens automatically once the clock runs out, totally irrespective of our recovery status or employment situation. functioning as a temporary raft, this tool is never meant to act as a permanent rescue vessel. purchasing a brief window of stability does absolutely nothing to shrink the massive principal balance.

HOW LONG DOES PPI PAY OUT?

utilizing payment protection limits your safety net to 12 to 24 months, an duration that often proves insufficient for severe medical conditions.

WHY LIFE INSURANCE SERVES A FUNDAMENTALLY DIFFERENT PURPOSE

contrasting a brief payment pause against the permanent nature of mortality protection clears up any lingering confusion. dismissing temporary layoffs or minor fractures is inherent to a standard death benefit contract. releasing a massive capital reserve happens solely upon verified mortality, or occasionally following a terminal prognosis carrying less than twelve months of life expectancy. addressing the ultimate, permanent loss requires a permanent, heavily capitalized solution that property mortgage protection cannot replicate.

cementing this distinct difference into our strategic planning is critical. acquiring a short-term income patch fails to produce a generational legacy or erase massive principal debts upon our passing. relying on a death benefit, conversely, provides zero assistance if we lose our job next week and cannot make the monthly installment. building a comprehensive defensive posture frequently involves layering both home insurance and life insurance derivatives, fully aware of exactly which crisis activates which policy.

ENHANCING YOUR FINANCIAL SHIELD: SUPPLEMENTARY PROTECTIONS

showcasing genuine mastery over asset protection means pushing past the bare minimum requirements. spending a few dozen pounds monthly on base-level coverage solely guards against the most catastrophic, terminal outcome. analyzing historical claims data proves that surviving a debilitating disease inflicts financial devastation far more frequently than abrupt mortality. widening our defensive perimeter is the logical next step for holistic wealth preservation in our home insurance and life insurance strategies.

NOTE:

enduring a massive health crisis generates immense financial strain, emphasizing that living payouts rival death benefits in overall importance.

weaving supplementary, yet critical, layers into our financial architecture is the solution. acquiring mechanisms that deliver capital while we are alive is a massive priority. advanced clinical treatments allow us to beat oncological diagnoses and cardiac events that were previously fatal. beating the disease, however, rarely translates into a rapid return to full-time employment and normal mortgage servicing. injecting targeted liquidity protects our physical assets while our bodies slowly recuperate.

CRITICAL ILLNESS COVER (CIC): SECURING LIVING BENEFITS

adding a severe illness rider stands out as one of the most powerful tactical upgrades available. distinguishing this product from standard mortality coverage hinges on its ability to release tax-free funds to a living policyholder. confirming a diagnosis for a specific condition outlined in the contract instantly activates the capital transfer. “THE LANCET” notes that managing recovery from advanced cancers, severe strokes, or aggressive multiple sclerosis demands massive external resources.

TIPS:

reviewing your existing documentation reveals whether terminal illness cover is already bundled, noting its distinct differences from broader critical illness protection.

embedding this feature as an accelerated rider or buying it completely separate are both viable structural choices. receiving this capital influx feels miraculous when a brutal medical verdict alters our reality. deploying the funds to eradicate the property debt, finance specialized clinical interventions, or modify the residence for mobility access prevents a rapid descent into bankruptcy. weaving this into our home insurance and life insurance grid is highly recommended.

INCOME PROTECTION: THE ULTIMATE SAFETY NET FOR SINGLE BUYERS

structuring a long-term income replacement plan ensures a steady cash flow, typically substituting half to two-thirds of our historical gross earnings during severe incapacity. outlasting the brief duration of standard payment defense, this mechanism operates for years on end. maintaining the monthly deposits until we either regain our health, hit retirement parameters, or pass away creates unparalleled stability. building this heavily reinforced safety net is a phenomenal way to protect future earnings.

emphasizing a highly specific structural truth regarding this tool is important for our single demographic. purchasing property alone, without children or a partner relying on the income, completely negates the mathematical requirement for standard mortality coverage. facing a health crisis as a solo buyer means zero secondary salary exists to float the household expenses. lacking a consistent revenue stream practically guarantees the lending institution will seize the collateral. deploying an income replacement strategy acts as the absolute strongest defense for an unattached buyer, complementing their home insurance and life insurance effectively.

REMEMBER:

securing income replacement forms a long-term commitment designed to keep you sheltered during extended periods of medical unemployment.

THE MORTGAGE BROKER BATTLEFIELD: NAVIGATING SALES PRESSURE

acknowledging the severe psychological weight of a real estate purchase is vital for providing realistic guidance. acting as objective analysts requires us to confront the widespread stress reported by thousands of buyers. reaching the final stages of lending approval often leaves us exhausted, making us vulnerable to aggressive advisers pushing in-house products. prioritizing the loan’s success occasionally pushes us into blindly endorsing whichever safety contracts are placed in front of us.

developing a strong resistance to these eleventh-hour sales tactics is a necessity. capturing massive commissions drives brokers to aggressively push supplementary safety nets alongside the main debt facility. mapping out their commercial incentives helps us recognize the underlying bias in their suggestions. acquiring our home insurance and life insurance from the individual finalizing our debt is never a legal requirement. detaching the mortgage arrangement from the asset protection consultation is frequently the most lucrative move we can manage.

DECODING BROKER COMMISSIONS AND TIED PANELS

dissecting the internal mechanics of the advisory ecosystem grants our audience significant leverage. securing difficult lending approvals is where brokers excel, yet their secondary product suggestions are heavily influenced by massive commercial kickbacks. securing a signed mortality contract triggers an immediate, substantial payment from the carrier to the advisory firm. operating within a “tied panel” presents a massive hazard to the consumer. restricting their search exclusively to a handful of partnered corporations prevents these individuals from ever finding truly competitive rates.

WARNING:

trusting a tied broker usually results in inflated premiums, given their inability to scan the wider market for better pricing.

limiting a search to an exclusive network practically guarantees we will miss out on the sharpest pricing. evaluating merely a handful of pre-selected firms severely undercuts our ability to optimize the monthly cost. locking into artificially inflated rates for decades happens easily when we trust a restricted view of the market. missing out on a dramatically cheaper, superior contract occurs simply because the advisor was contractually forbidden from acknowledging that specific carrier when quoting our home insurance and life insurance.

HOW TO EXECUTE AN INDEPENDENT WHOLE-OF-MARKET COMPARISON

arming ourselves with practical, defensive tactics neutralizes the advisory advantage. tapping into broad, independent comparison engines prior to the final banking meeting is a strategy we heavily endorse. dedicating a brief window of time to establishing a realistic baseline for both our home insurance and life insurance provides immediate clarity. assessing the advisor’s final proposal becomes effortless once we know the actual, unfiltered market rate.

hunting down direct-only carriers adds another layer of thoroughness to our search. specific colossal institutions purposely bypass comparison platforms to sidestep third-party fees. visiting these direct channels manually guarantees our market analysis remains comprehensively intact. merging independent aggregator results with direct-to-consumer estimates completely dismantles the broker’s informational monopoly, allowing us to dictate the terms of our protection seamlessly alongside property mortgage protection discussions.

HOME INSURANCE AND LIFE INSURANCE: 7 CRITICAL STEPS FOR PROVEN PROTECTION

synthesizing all the complex actuarial data and market realities into an actionable sequence empowers us to take definitive control of our financial destiny. achieving optimal security requires moving beyond theoretical knowledge and executing a rigid set of protocols. following these seven distinct steps ensures that our home insurance and life insurance deployment operates flawlessly, stripping away vulnerability and cementing generational wealth retention.

step one involves auditing our exact liability numbers. calculating the precise rebuild cost of the physical structure, completely separate from the real estate market value, sets the baseline for the property defense. simultaneously, we must calculate the exact down-to-the-penny sum of our outstanding mortgage principal to set the mortality coverage baseline. obtaining these two hard figures prevents the most common error of systemic underinsurance.

step two demands separating our purchases. ignoring the aggressive cross-selling tactics deployed by banking institutions and centralized brokers guarantees we maintain market leverage. isolating the property quote from the mortality quote forces underwriters to compete purely on the merits of their specific product category. this step routinely saves thousands over the lifespan of a thirty-year home insurance and life insurance setup.

step three focuses entirely on matching the timeline. aligning the duration of our mortality contract explicitly to the final scheduled payment of our property loan ensures zero coverage gaps exist. stretching a twenty-five-year loan necessitates a twenty-five-year safety net. allowing our protection to expire in year twenty while five years of debt remain is a catastrophic oversight.

step four forces us to reject joint first-death structures if we are part of a buying couple. insisting on twin, individualized contracts guarantees that a tragedy affecting one partner does not instantly dissolve the safety net for the survivor. establishing this dual-layered defense is the absolute pinnacle of strategic property mortgage protection.

step five requires integrating living benefits into the architecture. recognizing that extreme medical survival rates are surging means we must prepare for prolonged unemployment rather than immediate demise. attaching critical illness riders or standalone income replacement tools ensures our mortgage installments continue seamlessly while we undergo specialized clinical rehabilitation.

step six dictates writing our mortality contracts into a formal trust. executing this legal maneuver ensures the massive capital payout bypasses the sluggish probate process entirely. funnelling the tax-free funds directly to our chosen beneficiaries within weeks, rather than months, empowers them to clear the debt immediately before banking arrears can legally accumulate.

step seven mandates a biennial review cycle. setting a strict calendar alert to re-evaluate our comprehensive home insurance and life insurance posture every twenty-four months ensures our safety nets evolve alongside our lives. introducing a new child, extending the property through a renovation, or securing a massive salary increase inherently demands recalibrating our financial defenses.

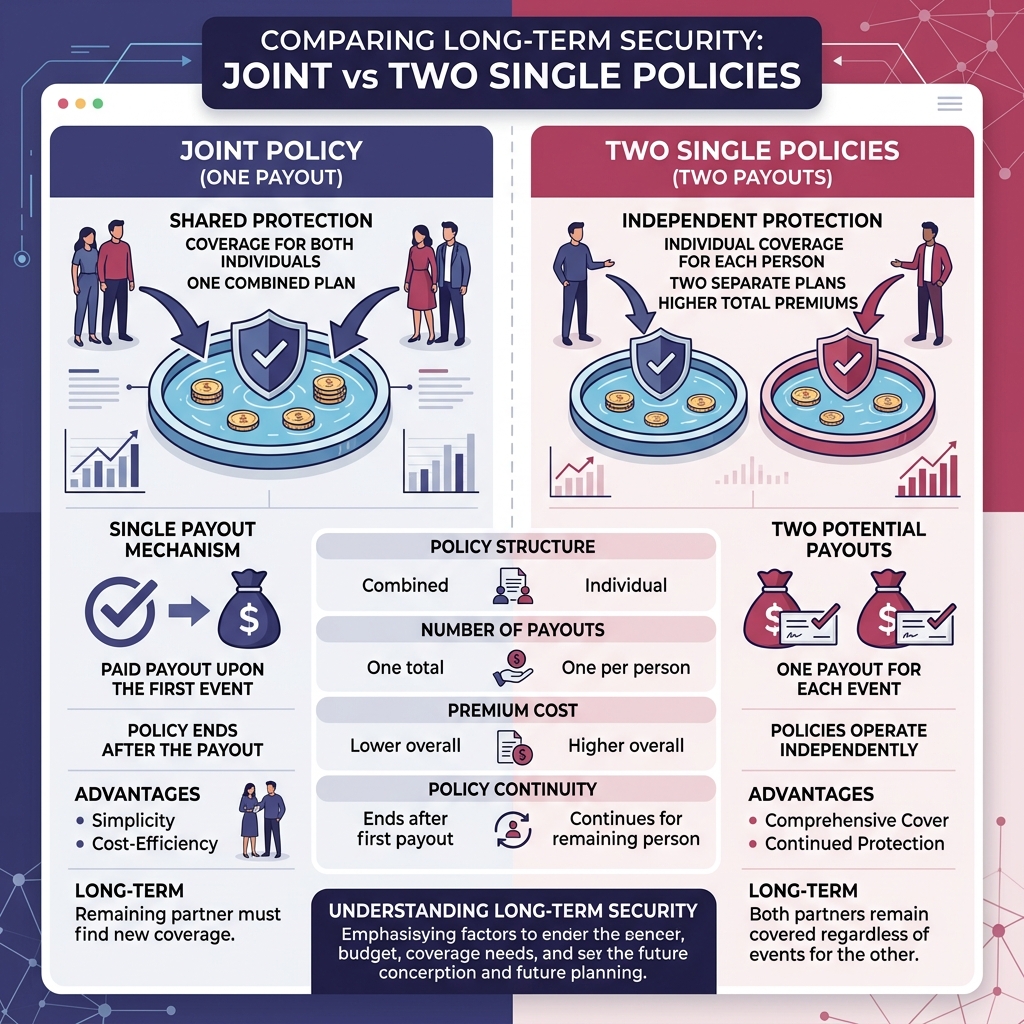

STRATEGIC STRUCTURING: JOINT VS. SINGLE LIFE POLICIES

acquiring a residence as a dual-income partnership introduces a complex, highly significant structural variable. defaulting to a singular, shared safety net is the path of least resistance pushed by most digital tools and uninspired agents. merging the risk feels intuitively correct from an administrative standpoint. running the long-term mathematical models, however, indicates that utilizing a shared framework is generally a severe mistake that drastically undercuts the surviving individual’s security regarding home insurance and life insurance.

NOTE:

engineering your contracts correctly dictates whether your household enjoys basic coverage or robust, single and double protection against multiple tragedies.

projecting our economic durability thirty years down the timeline matters far more than saving pennies on the immediate monthly draft. tracking the exact trigger mechanisms determines what happens to the underlying framework after an initial fatality. exposing the dangerous clauses hiding inside shared contracts is fundamental to our strategy. spending slightly more capital upfront on isolated agreements produces a remarkably stronger fortress for our dependents as they age.

THE LIMITATIONS OF “FIRST DEATH” JOINT POLICIES

defining the unyielding rules governing shared mortality contracts is our next objective. linking two human lives under one specific agreement means the payout functions on a strict “first death” parameter. suffering the loss of the initial partner forces the carrier to deploy the capital and wipe the ledger clean. triggering that transfer, unfortunately, instantly dissolves the contract in its entirety, leaving nothing behind in the realm of property mortgage protection.

abandoning the surviving individual without any subsequent safety net highlights the catastrophic weakness of this setup. owning a house outright is fantastic, yet lacking any mechanism to leave capital to their offspring creates a new hazard. attempting to source fresh coverage as a fifty-year-old widow or widower introduces massive hurdles. fighting against age-based price hikes and newly acquired health defects ensures that procuring a new safety net remains prohibitively expensive.

THE LONG-TERM ADVANTAGES OF TWO SINGLE POLICIES

championing the implementation of dual, isolated contracts is a core pillar of our philosophy. absorbing a slightly heavier recurring premium initially unlocks profound, compounding strategic benefits over the long run. watching partner a’s unique agreement activate, erase the principal, and close out proves the efficiency of this method. preserving partner b’s isolated safety net without interruption is the ultimate goal, ensuring their coverage remains active.

CAN TWO SINGLE POLICIES PAY OUT TWICE?

utilizing twin contracts guarantees that two separate lump sums deploy to the offspring if both individuals pass away during the timeline.

holding onto a cheap, medically verified contract locked in during a younger, healthier phase grants the survivor massive leverage. controlling a paid-off asset while possessing a secondary capital reservoir intended for the next generation is a phenomenal position. deploying this dual-layered defense elevates a standard loan-clearing tactic into a robust framework for preserving wealth across multiple generations. demanding isolated estimates from brokers is a rule we expect all partnerships to follow when negotiating home insurance and life insurance.

SPECIALIZED PROPERTY SCENARIOS AND UNIQUE LIABILITIES

expanding our analytical lens beyond basic detached properties guarantees our framework remains universally applicable. navigating a heavily segmented housing market means addressing the distinct legal exposures generated by varied ownership structures. pasting standard templates onto niche scenarios, such as apartment blocks or rental portfolios, guarantees voided contracts and severe capital losses. customizing the specific type of home insurance and life insurance to match the exact legal tenure is an absolute requirement.

operating within the strict boundaries of insurable interest dictates how underwriters evaluate risk. suffering a direct economic hit from an asset’s destruction is the only way we legally qualify to protect it. misidentifying the true legal owner of the exterior bricks easily leads to purchasing redundant coverage that carriers will aggressively deny during a massive claim. analyzing title deeds with absolute precision prevents these disastrous technicalities.

REMEMBER:

confirming the exact tenure type immediately clarifies which party holds the legal burden for protecting the physical bricks.

FREEHOLD VS. LEASEHOLD: WHO IS RESPONSIBLE FOR BUILDINGS COVER?

clarifying the severe duties tied to physical ownership structures eliminates ambiguity. taking possession of a standard detached or semi-detached plot generally grants us absolute freehold status over the earth and the dwelling. holding total ownership instantly transfers one hundred percent of the structural protection burden directly onto our ledger. absorbing the financial consequences of an uninsured structural collapse is a risk we manage independently via our property mortgage protection.

flipping the script completely, apartment blocks usually operate under a leasehold dynamic. maintaining ultimate legal possession of the exterior shell remains the exclusive duty of the overarching block management firm or the central freeholder. organizing macro-level protection against structural disasters falls to them, and they seamlessly embed those premiums into our yearly maintenance fees. purchasing exterior coverage as a flat owner is a massive error; our focus should narrow exclusively to securing our interior movable goods.

PROTECTING RENTAL INVESTMENTS: THE ROLE OF LANDLORD INSURANCE

evaluating the commercial rental sector requires acknowledging a massive shift in baseline liability. introducing external, paying occupants into the dwelling instantaneously warps the actuarial risk profile of the property. moving a tenant in absolutely voids standard residential agreements without exception. transitioning to a dedicated landlord contract secures specialized additions, encompassing public liability defense and safeguards against malicious rent defaulting, which standard frameworks purposely exclude.

TIPS:

investigating specialized rent guarantee insurance allows commercial property owners to shield their cash flow from defaulting occupants.

advising property investors on mortality strategies is an equally critical component of our analysis. accumulating numerous rental units inherently requires accumulating a dangerous stack of heavily leveraged commercial debt. passing away abruptly forces an unprepared family to wrestle with immense banking liabilities. deploying targeted capital clears these specific commercial loans immediately, converting a terrifyingly leveraged portfolio into a streamlined, high-yield revenue engine for our heirs through meticulous home insurance and life insurance execution.

NON-HOMEOWNERS: DO RENTERS NEED PROTECTION?

crushing the widespread fallacy that mortality safety nets belong exclusively to the property-owning class is a major priority. tying the idea of asset protection exclusively to holding a mortgage deed misleads millions of lifelong tenants into ignoring severe personal vulnerabilities. misinterpreting the fundamental purpose of these financial tools creates massive societal risk. guarding the title deed is irrelevant; we are actually shielding the basic survival capabilities of the humans relying on our income.

lacking a massive bank loan certainly does not eliminate the relentless pressure of recurring household expenses. managing landlord payments, covering energy tariffs, and supplying groceries requires continuous capital. extracting the primary earner from a tenant situation frequently triggers a faster, sharper economic freefall than in a mortgaged scenario, simply due to the absence of stored equity. shifting the narrative away from real estate and focusing tightly on human frailty represents a necessary evolution in our financial planning surrounding home insurance and life insurance concepts.

NOTE:

facing a crisis without any equity in a home to liquidate leaves renting families acutely exposed to rapid financial collapse.

WHY LIFE INSURANCE REMAINS VITAL FOR TENANTS WITH DEPENDENTS

speaking directly to those locked into the private rental market highlights an urgent structural need. possessing zero legal duty to fix the exterior walls and lacking a principal loan balance are obvious truths for tenants. harboring dependents or a spouse who survive on our wages, however, changes the calculus entirely. stopping that cash flow permanently guarantees an inability to service the tenancy agreement, accelerating the timeline toward inevitable eviction.

establishing our final position confirms that supporting financial dependents is the sole trigger for requiring mortality protection, completely divorced from holding property deeds. utilizing an inexpensive, flat-rate contract delivers a massive capital reserve, enabling a devastated renting family to securely meet lease obligations for extended periods. granting this psychological and economic breathing room allows dependents to systematically adjust to their altered circumstances. recognizing that basic defensive planning applies to everyone is vital for mastering home insurance and life insurance theories.

CONCLUSION

finalizing this analysis provides us with an unyielding, comprehensive architecture for economic defense. managing real estate acquisitions requires an aggressive, multi-layered approach to neutralizing long-term threats. verifying through extensive data modeling, we see that property coverage handles the strict physical collateral needs of the bank, while mortality coverage shields the vulnerable human capital driving the operation. ignoring either side of this equation dangerously exposes our dependents to severe setbacks capable of destroying decades of accumulated wealth.

delivering our final mandate requires us to warn against taking the lazy, convenient path. rejecting the forceful, combined packages peddled by heavily commissioned advisors is something we strongly advocate. splitting our investigations apart and running fierce, unbiased market comparisons ensures we capture the sharpest available terms for our home insurance and life insurance. selecting isolated tools, and heavily prioritizing twin personal contracts over shared setups, successfully erects a flawless barrier around our wealth and solidifies our descendants’ economic trajectory permanently.